You might also like

- Factory Overhead - RFDDocument32 pagesFactory Overhead - RFDSamantha DionisioNo ratings yet

- CHAPTER 2 Cost Terms and PurposeDocument31 pagesCHAPTER 2 Cost Terms and PurposeRose McMahonNo ratings yet

- Cma Adnan Rashid Complete NotesDocument541 pagesCma Adnan Rashid Complete NotesHAREEM25% (4)

- Chapter 2 - Cost Concepts and Design EconomicsDocument54 pagesChapter 2 - Cost Concepts and Design EconomicsShayne Aira Anggong75% (4)

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Overhead Cost ManagementDocument47 pagesOverhead Cost ManagementTarakeshsapNo ratings yet

- Cost of Production ReportDocument14 pagesCost of Production ReportMuiz Hassan89% (9)

- Guidance For Candidates - The Iam Certificate: Edition 2 - January 2013Document14 pagesGuidance For Candidates - The Iam Certificate: Edition 2 - January 2013gosalhs9395No ratings yet

- Lecture 01 - Cost AccountingDocument56 pagesLecture 01 - Cost Accountingdia_890No ratings yet

- Volume 2 India Ver 141005 PDFDocument222 pagesVolume 2 India Ver 141005 PDFLittin Thankachan82% (17)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

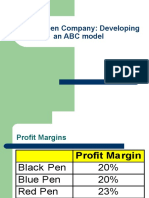

- Classic Pen Company: Developing An ABC ModelDocument22 pagesClassic Pen Company: Developing An ABC Modeljk kumarNo ratings yet

- Job Order Costing Systems DesignDocument24 pagesJob Order Costing Systems DesignSonali Jagath100% (1)

- I Am Sharing 'Cost Accounting and Classification7280895122984483619' With YouDocument10 pagesI Am Sharing 'Cost Accounting and Classification7280895122984483619' With Yousuraj banNo ratings yet

- Introduction Cost Concepts Terms and BehaviorDocument43 pagesIntroduction Cost Concepts Terms and BehaviorZACARIAS, Marc Nickson DG.No ratings yet

- Chapter 1: Cost Sheet (Unit Costing)Document102 pagesChapter 1: Cost Sheet (Unit Costing)Rimsha HanifNo ratings yet

- Cost Accounting: Introduction To Cost Accounting Lecture-1 Jameel A Khan HakroDocument35 pagesCost Accounting: Introduction To Cost Accounting Lecture-1 Jameel A Khan Hakrokashif aliNo ratings yet

- Basic Cost Management ConceptsDocument7 pagesBasic Cost Management ConceptsImadNo ratings yet

- UEU Akuntansi Biaya Pertemuan 8910Document84 pagesUEU Akuntansi Biaya Pertemuan 8910hardyputra46No ratings yet

- Cost Accounting DetailsDocument3 pagesCost Accounting DetailsAneela TabassumNo ratings yet

- Chapter04 000 PDFDocument27 pagesChapter04 000 PDFgracel angela tolejanoNo ratings yet

- Cost HandoutDocument31 pagesCost HandoutTilahun GirmaNo ratings yet

- Cost Accounting and Control: Cagayan State UniversityDocument74 pagesCost Accounting and Control: Cagayan State UniversityAntonNo ratings yet

- Costs - 3Document29 pagesCosts - 3Itachi UchihaNo ratings yet

- Purpose of costing: value inventory, record costs, price products, make decisionsDocument13 pagesPurpose of costing: value inventory, record costs, price products, make decisionsSiddiqua KashifNo ratings yet

- Accounting For Other ExpensesDocument8 pagesAccounting For Other ExpensesLinyVatNo ratings yet

- CostDocument36 pagesCostbt21108016 Kehkasha AroraNo ratings yet

- Costing Methods: Actual, Normal and StandardDocument71 pagesCosting Methods: Actual, Normal and StandardKathleya Weena EmbradoNo ratings yet

- Term Associated With CostDocument6 pagesTerm Associated With Costaashir chNo ratings yet

- On Target Vol2 No4 2012 SEP Overhead Rates and Absorption Versus Variable CostingDocument6 pagesOn Target Vol2 No4 2012 SEP Overhead Rates and Absorption Versus Variable CostingnajmulNo ratings yet

- Manufacturing OverheadDocument5 pagesManufacturing OverheadSheila Mae AramanNo ratings yet

- C1 - Introduction To MGMT AccDocument28 pagesC1 - Introduction To MGMT AccLee Li HengNo ratings yet

- Understanding Cost Concepts for Managerial DecisionsDocument75 pagesUnderstanding Cost Concepts for Managerial DecisionsVivek AnbuNo ratings yet

- Ac102 ch2Document21 pagesAc102 ch2Fisseha GebruNo ratings yet

- Cost & Management Accounting - MGT402 Power Point Slides Lecture 01Document27 pagesCost & Management Accounting - MGT402 Power Point Slides Lecture 01iris2326No ratings yet

- Managerial Accounting Cost ConceptsDocument19 pagesManagerial Accounting Cost ConceptsSohaib ArifNo ratings yet

- Lecture-1 Introduction of Cost AccountingDocument28 pagesLecture-1 Introduction of Cost Accountingarslanjaved690No ratings yet

- Introduction to Cost and Management AccountingDocument19 pagesIntroduction to Cost and Management AccountingTilahun GirmaNo ratings yet

- Chapter 3 Cost IDocument64 pagesChapter 3 Cost IBikila MalasaNo ratings yet

- Cost ConceptsDocument8 pagesCost ConceptssreekanthNo ratings yet

- Chapter 2 - Managerial Cost Concepts and Cost Behaviour AnalysisDocument53 pagesChapter 2 - Managerial Cost Concepts and Cost Behaviour AnalysisPRAkriT POUdeLNo ratings yet

- Principles of Cost AccountingDocument28 pagesPrinciples of Cost AccountingNin WaramNo ratings yet

- Variable, Fixed, Direct and Indirect CostsDocument7 pagesVariable, Fixed, Direct and Indirect Costsraul_mahadikNo ratings yet

- Dwnload Full Cost Accounting A Managerial Emphasis 14th Edition Horngren Solutions Manual PDFDocument35 pagesDwnload Full Cost Accounting A Managerial Emphasis 14th Edition Horngren Solutions Manual PDFcurguulusul100% (13)

- Managerial Economics NotesDocument17 pagesManagerial Economics NotesBell BottleNo ratings yet

- Cost Accounting Cost Accounting: Unit-IDocument65 pagesCost Accounting Cost Accounting: Unit-IPriyanshu JhaNo ratings yet

- Production and Operations Management Cost ConceptsDocument37 pagesProduction and Operations Management Cost ConceptsYash PathakNo ratings yet

- Cost_Classifications__167083589515669092976396eeb75c11aDocument16 pagesCost_Classifications__167083589515669092976396eeb75c11a22je0766No ratings yet

- Pre-Study Session 4Document10 pagesPre-Study Session 4Narendralaxman ReddyNo ratings yet

- Study Note Ma1Document16 pagesStudy Note Ma1Kwasi AppiahNo ratings yet

- Actual, Opportunity, Sunk, Incremental Cost DefinitionsDocument2 pagesActual, Opportunity, Sunk, Incremental Cost DefinitionsdragjoNo ratings yet

- Group 8 - Chap 2 an Introduction to Cost Terms and PurposeseDocument39 pagesGroup 8 - Chap 2 an Introduction to Cost Terms and Purposeseqgminh7114No ratings yet

- Key Differences Between Cost Accounting and Financial AccountingDocument32 pagesKey Differences Between Cost Accounting and Financial AccountingsajedulNo ratings yet

- Cost BBIT Lec-1Document11 pagesCost BBIT Lec-1Amna Seok-JinNo ratings yet

- Fundamentals of Costing ExplainedDocument32 pagesFundamentals of Costing ExplainedAfzal AhmedNo ratings yet

- MaxwelDocument4 pagesMaxwelJayesh ChopadeNo ratings yet

- Cost Accounting: Swiss Business SchoolDocument149 pagesCost Accounting: Swiss Business SchoolMyriam Elaoun100% (1)

- 701211-บทที่ 1 แนวคิดเกี่ยวกับต้นทุนและการจำแนกประเภทต้นทุนDocument24 pages701211-บทที่ 1 แนวคิดเกี่ยวกับต้นทุนและการจำแนกประเภทต้นทุนWich PanuwichNo ratings yet

- Unit 2: Final Accounts of Manufacturing Entities: Learning OutcomesDocument17 pagesUnit 2: Final Accounts of Manufacturing Entities: Learning OutcomessajedulNo ratings yet

- BMT1009 Production and Operations Management: Unit-IIDocument37 pagesBMT1009 Production and Operations Management: Unit-IIKartik ChaturvediNo ratings yet

- Chapter 2Document17 pagesChapter 2Ngọc Minh Đỗ ChâuNo ratings yet

- CH-4 Chapter ManufDocument14 pagesCH-4 Chapter Manufጌታ እኮ ነውNo ratings yet

- Discussion 3 FinanceDocument7 pagesDiscussion 3 Financepeter njovuNo ratings yet

- BCT593 ASSIGNMENT ESTIMATING March August 2023Document7 pagesBCT593 ASSIGNMENT ESTIMATING March August 2023MAXSWELL MANGGIE ZAMRYNo ratings yet

- Accounting TermsDocument13 pagesAccounting TermsNadeem KhanNo ratings yet

- Managerial Accounting Final ProjectDocument5 pagesManagerial Accounting Final Projectapi-382641983No ratings yet

- Cost Allocation Joint Products and ByproductsDocument8 pagesCost Allocation Joint Products and ByproductsHendriMaulanaNo ratings yet

- Dabur Winter Internship Report SagarDocument30 pagesDabur Winter Internship Report SagarSagar RaghuwanshiNo ratings yet

- Modul Lab - Akuntansi Manajemen 1 P22.23-1Document31 pagesModul Lab - Akuntansi Manajemen 1 P22.23-1Bena BustikaNo ratings yet

- Cost Accounting: Introduction and Key ConceptsDocument60 pagesCost Accounting: Introduction and Key ConceptspujaskawaleNo ratings yet

- Consignment NotesDocument6 pagesConsignment NotesZAKA ULLAHNo ratings yet

- Clapton Company inventory and overhead analysisDocument6 pagesClapton Company inventory and overhead analysisDiệu Linh Phan ThịNo ratings yet

- F5 PM Quantitative AnalysisDocument14 pagesF5 PM Quantitative AnalysisMazni HanisahNo ratings yet

- Absorption Costing ScriptDocument2 pagesAbsorption Costing ScriptRegine NanitNo ratings yet

- 1-Managerial AccountingDocument2 pages1-Managerial AccountingHaleem KhanNo ratings yet

- Wave Money Success Story: Key Learnings from Myanmar's Leading Mobile Financial Services ProviderDocument34 pagesWave Money Success Story: Key Learnings from Myanmar's Leading Mobile Financial Services ProviderBưu điện Việt Nam VNPostNo ratings yet

- Executive Guide - Negosim 2020 PDFDocument16 pagesExecutive Guide - Negosim 2020 PDFishan66666No ratings yet

- As 10 - Fixed Assets - As Made EasyDocument23 pagesAs 10 - Fixed Assets - As Made EasyraviNo ratings yet

- BLR CestatDocument9 pagesBLR CestatS kameshNo ratings yet

- Lesson 2Document15 pagesLesson 2Pamela MorcillaNo ratings yet

- 4 Borrowing CostDocument16 pages4 Borrowing CostHafizur RahmanNo ratings yet

- Accounting Skills in Recording Business Transactions-1 - 074113Document60 pagesAccounting Skills in Recording Business Transactions-1 - 074113shabanzuhura706No ratings yet

- Accounting Policies: 29th Annual ReportDocument4 pagesAccounting Policies: 29th Annual ReportTindo MoyoNo ratings yet

- Acctg 112 Reviewer Pas 1 8Document26 pagesAcctg 112 Reviewer Pas 1 8surbanshanrilNo ratings yet

- Ebook Cost Accounting Foundations and Evolutions 8Th Edition Kinney Test Bank Full Chapter PDFDocument61 pagesEbook Cost Accounting Foundations and Evolutions 8Th Edition Kinney Test Bank Full Chapter PDFCherylHorngjmf100% (10)

- Budgetary As A Planning ToolDocument60 pagesBudgetary As A Planning ToolVaisal AmirNo ratings yet

- Cost and Management Accounting GuideDocument79 pagesCost and Management Accounting GuideEalshady HoneyBee Work ForceNo ratings yet

- EP 1110-1-8 Vo2 PDFDocument501 pagesEP 1110-1-8 Vo2 PDFyodiumhchltNo ratings yet