You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

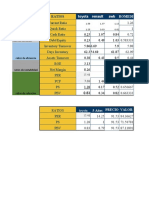

- Bilant Lb. Engleza ModelDocument5 pagesBilant Lb. Engleza ModelklarckkentNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Chapter 3 MCQ Afar 2 CompressDocument73 pagesChapter 3 MCQ Afar 2 Compresstaehyung kimNo ratings yet

- MCQ-Financial AccountingDocument13 pagesMCQ-Financial AccountingArchana100% (1)

- CASE 1: Petty Cash Fund Bank ReconciliationDocument50 pagesCASE 1: Petty Cash Fund Bank ReconciliationJohn Lloyd Yasto100% (1)

- Analisis Fundamentalde EmpresasDocument6 pagesAnalisis Fundamentalde EmpresasJHON JANER RODRIGUEZ MONTERONo ratings yet

- Week 5 Chapter 11Document6 pagesWeek 5 Chapter 11CIA190116 STUDENTNo ratings yet

- ACCT 501-Midterm FlashcardsDocument17 pagesACCT 501-Midterm FlashcardscarterkddNo ratings yet

- What Is An Intangible AssetDocument2 pagesWhat Is An Intangible AssetShin Darren BasabeNo ratings yet

- IAS 7 - Statement of Cash FlowsDocument21 pagesIAS 7 - Statement of Cash FlowsTD2 from Henry HarvinNo ratings yet

- FarDocument7 pagesFarVince MiramonNo ratings yet

- DocumentDocument5 pagesDocumentJannelle SalacNo ratings yet

- MBA AssignmentDocument2 pagesMBA Assignmentg_d_dubeyciaNo ratings yet

- Income StatementDocument13 pagesIncome StatementShakir IsmailNo ratings yet

- Business Plan OutlineDocument5 pagesBusiness Plan OutlineZulqarnain Bin Mohd NoorNo ratings yet

- Geme CostDocument6 pagesGeme CostBiruk Chuchu NigusuNo ratings yet

- Ambit Strategy Thematic Tomorrows Ten Baggers 19jan2012Document15 pagesAmbit Strategy Thematic Tomorrows Ten Baggers 19jan2012jainvivekNo ratings yet

- Sample Multiple Choice Questions Tybbi - Sem V Auditing IDocument25 pagesSample Multiple Choice Questions Tybbi - Sem V Auditing IShristi PathakNo ratings yet

- Financial Statement Analysis and Valuation 4th Edition Easton Test BankDocument30 pagesFinancial Statement Analysis and Valuation 4th Edition Easton Test BankTroyKnappdpci100% (15)

- Gale NikaDocument18 pagesGale NikaMister xNo ratings yet

- Partnership Exercise 2Document5 pagesPartnership Exercise 2nikNo ratings yet

- Handout On Chapter 12 Corporations PDFDocument9 pagesHandout On Chapter 12 Corporations PDFJeric TorionNo ratings yet

- Smokey ValleyDocument3 pagesSmokey ValleyaviNo ratings yet

- Solución Capitulo 3Document75 pagesSolución Capitulo 3ArnoldoGonzalezNo ratings yet

- Accounting For Special Transactions:: Corporate LiquidationDocument28 pagesAccounting For Special Transactions:: Corporate LiquidationKim EllaNo ratings yet

- MBA104 - Almario - Parco - Case Study LGAOP02Document25 pagesMBA104 - Almario - Parco - Case Study LGAOP02Jesse Rielle CarasNo ratings yet

- ACCT504 Case Study 1 The Complete Accounting CycleDocument19 pagesACCT504 Case Study 1 The Complete Accounting Cyclechana9800% (1)

- Audit Prob - ReceivablesDocument27 pagesAudit Prob - ReceivablesCharis Marie Urgel100% (3)

- Buscom Quiz: Book Value Fair ValueDocument2 pagesBuscom Quiz: Book Value Fair ValueNairah M. TambieNo ratings yet

- 18CSU13 PSG College of Arts & Science Bcom (CS) Degree Examination May 2021Document5 pages18CSU13 PSG College of Arts & Science Bcom (CS) Degree Examination May 202119BCS531 Nisma FathimaNo ratings yet