You might also like

- Orca Share Media1670298872061 7005741240281517773Document14 pagesOrca Share Media1670298872061 7005741240281517773Hannah Marie NunagNo ratings yet

- Accounting 101: Facilitator: P. S. RajeshDocument33 pagesAccounting 101: Facilitator: P. S. RajeshBalaVivekNo ratings yet

- Step 3 4Document7 pagesStep 3 4Carls AligwayNo ratings yet

- Solution Cash Receipts Journal (A)Document9 pagesSolution Cash Receipts Journal (A)Qasim Khan100% (1)

- Accounting Record SystemDocument36 pagesAccounting Record Systemmanishpareta5No ratings yet

- Sample worksheet K204050266 P3.5Document16 pagesSample worksheet K204050266 P3.5Trâm Mai Thị ThùyNo ratings yet

- Chapter 1 - Recording Business TransactionDocument14 pagesChapter 1 - Recording Business TransactionThủy NguyễnNo ratings yet

- Part 3 - AccountingDocument13 pagesPart 3 - AccountingAmr YoussefNo ratings yet

- Kuliah 4 - Pelarasan AkaunDocument46 pagesKuliah 4 - Pelarasan AkaunDHARANIYA A/P SUBRAMANIAMNo ratings yet

- Kuliah 4 - Pelarasan AkaunDocument46 pagesKuliah 4 - Pelarasan AkaunDHARANIYA A/P SUBRAMANIAM100% (1)

- Soft Byte Company Journal Book EntriesDocument1 pageSoft Byte Company Journal Book EntriesSiam FarhanNo ratings yet

- BUSN7008 Week 3 Adjustments - Updated 2023Document33 pagesBUSN7008 Week 3 Adjustments - Updated 2023berfamenNo ratings yet

- Accounting Assignment Bilal 18798Document4 pagesAccounting Assignment Bilal 18798Muhammad Shahid KhanNo ratings yet

- Week3-Lecture 6 NotesDocument28 pagesWeek3-Lecture 6 Noteskk23212No ratings yet

- Presentation ON General Ledger & Trail BalanceDocument14 pagesPresentation ON General Ledger & Trail BalanceNumanNo ratings yet

- Tugas Akuntansi DasarDocument7 pagesTugas Akuntansi DasarJabbar aqwanNo ratings yet

- Accounting transactions journal entriesDocument8 pagesAccounting transactions journal entriesGedie Rocamora100% (1)

- Journal Entries for Accounting AdjustmentsDocument18 pagesJournal Entries for Accounting AdjustmentsJavid BalakishiyevNo ratings yet

- Financial Accounting Assignments ExplainedDocument8 pagesFinancial Accounting Assignments Explainedibrar ghaniNo ratings yet

- Analyzing TransactionsDocument8 pagesAnalyzing TransactionsUgaas yare21No ratings yet

- Account... : An Individual Accounting Record of Increases and Decreases in A Specific or ItemDocument25 pagesAccount... : An Individual Accounting Record of Increases and Decreases in A Specific or ItemPRIYA KUMARINo ratings yet

- Posting To Ledger Trial BalanceDocument18 pagesPosting To Ledger Trial BalanceVincent Neil NarvasNo ratings yet

- Trialbalance 1Document3 pagesTrialbalance 1Thư TrầnNo ratings yet

- Manual - BRS - Screen & LogicDocument19 pagesManual - BRS - Screen & LogicmayoorNo ratings yet

- Excel Chapter 6Document49 pagesExcel Chapter 6Rafia TasnimNo ratings yet

- Week2-Lecture 5 NotesDocument18 pagesWeek2-Lecture 5 Noteskk23212No ratings yet

- Recording of Business TransactionsDocument30 pagesRecording of Business TransactionsAnthony John BrionesNo ratings yet

- A. P100 Par Value Date Account Title DR CRDocument5 pagesA. P100 Par Value Date Account Title DR CRCalyx ImperialNo ratings yet

- Latihan 9 Sept 2021-Kelompok 3Document8 pagesLatihan 9 Sept 2021-Kelompok 3Marsya SigarlakiNo ratings yet

- Naura Alya Khalista - EA E - PG1 PG2 PG3Document8 pagesNaura Alya Khalista - EA E - PG1 PG2 PG3Naura AlyaNo ratings yet

- Bookkeeping Guide for EntrepreneursDocument29 pagesBookkeeping Guide for EntrepreneursVignette San AgustinNo ratings yet

- M.Com Financial Accounting Course OverviewDocument23 pagesM.Com Financial Accounting Course OverviewAwais ur RehmanNo ratings yet

- Adjusting The AccountsDocument17 pagesAdjusting The AccountsDira SabillaNo ratings yet

- Abdulla YounisDocument4 pagesAbdulla Younisashwani singhaniaNo ratings yet

- ACC407 - Chapter 4b - Trial BalanceDocument18 pagesACC407 - Chapter 4b - Trial BalanceA24 Izzah100% (1)

- ACCT 2211 Assignment 2Document17 pagesACCT 2211 Assignment 2Tannaz SNo ratings yet

- Tugas P3.1 Jurnal PenyesuaianDocument5 pagesTugas P3.1 Jurnal Penyesuaianyasser.amarullah.2304136No ratings yet

- Tugas 3 (Revisi) - Proses Posting-Ricky Andrian K. RumereDocument23 pagesTugas 3 (Revisi) - Proses Posting-Ricky Andrian K. RumererickyNo ratings yet

- Buana & Karya Baru: No Date Account Title and Explanation Reff Debit 1 8-Jan Inventory 235 Cash 2Document6 pagesBuana & Karya Baru: No Date Account Title and Explanation Reff Debit 1 8-Jan Inventory 235 Cash 2Jasmine AfifahNo ratings yet

- BT C1 - kttcqt1Document13 pagesBT C1 - kttcqt1Thảo NguyễnNo ratings yet

- Assignment 2Document11 pagesAssignment 2Ms.Muriel MorongNo ratings yet

- JS1 3RD TERM BUSINESS STUDIESDocument28 pagesJS1 3RD TERM BUSINESS STUDIESpalmer okiemuteNo ratings yet

- Chapters 4 and 5 The LedgerDocument14 pagesChapters 4 and 5 The LedgerSneha DasNo ratings yet

- 2020 AnswerDocument15 pages2020 Answertanjimalomturjo1No ratings yet

- Ch2 The Recording Process ACC101Document15 pagesCh2 The Recording Process ACC101Muhammad KridliNo ratings yet

- Chapter 5 - MerchandisingDocument39 pagesChapter 5 - Merchandisingk58 Cao Pham Ha MyNo ratings yet

- Jawaban Soal Akuntansi Piutang DagangDocument4 pagesJawaban Soal Akuntansi Piutang Dagangsilvia indahsariNo ratings yet

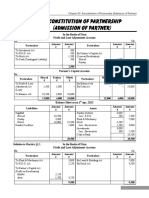

- 03 Reconstitution of Partnership Admission of Partner PDFDocument24 pages03 Reconstitution of Partnership Admission of Partner PDFBrawler Stars100% (3)

- This Study Resource Was: Date TransactionDocument5 pagesThis Study Resource Was: Date TransactionJames CastañedaNo ratings yet

- Chapter 2Document9 pagesChapter 2AmiliaNo ratings yet

- As Level Accounting Topic 1 OddDocument45 pagesAs Level Accounting Topic 1 OddShoaib AslamNo ratings yet

- AmirDocument7 pagesAmirMian UmarNo ratings yet

- Assignment No 1 FinalDocument13 pagesAssignment No 1 FinalMuhammad AwaisNo ratings yet

- Class Illustration: PG 56 Question 12: Ledger Accounts Cash AccountDocument2 pagesClass Illustration: PG 56 Question 12: Ledger Accounts Cash AccountBOON KEE KEKNo ratings yet

- Preparation of Ledger Trial Balance and Bank Reconciliation Statement 02 PDFDocument30 pagesPreparation of Ledger Trial Balance and Bank Reconciliation Statement 02 PDFzaya sarwarNo ratings yet

- Acc Formula PNS CycleDocument19 pagesAcc Formula PNS CycleJING RONG GOHNo ratings yet

- Account Name Account Number: Bengkel Servis Motor Sejat Trial Balance Pe 31 December 2004Document30 pagesAccount Name Account Number: Bengkel Servis Motor Sejat Trial Balance Pe 31 December 2004Rynda Nur AenyNo ratings yet

- Prinsip Dasar AkuntansiDocument20 pagesPrinsip Dasar Akuntansiabdul muslimNo ratings yet

- BT kế toán quốc tếDocument58 pagesBT kế toán quốc tếUyên Nguyễn Hoàng ThanhNo ratings yet

- How Finishing Tasks Fast Can Save TimeDocument1 pageHow Finishing Tasks Fast Can Save TimeHidden UniverseNo ratings yet

- How To Help Aging Parents Deal With LonelinessDocument1 pageHow To Help Aging Parents Deal With LonelinessHidden UniverseNo ratings yet

- Final SummaryDocument1 pageFinal SummaryHidden UniverseNo ratings yet

- How To Help A Friend Get Over A BreakupDocument1 pageHow To Help A Friend Get Over A BreakupHidden UniverseNo ratings yet

- MGT 212 - Chapter 3 - Managing The External Environment and Organization's CultureDocument45 pagesMGT 212 - Chapter 3 - Managing The External Environment and Organization's CultureHidden UniverseNo ratings yet

- MGT 212 - Chapter 1 (Part 1) - Managers and You in The WorkplaceDocument27 pagesMGT 212 - Chapter 1 (Part 1) - Managers and You in The WorkplaceHidden UniverseNo ratings yet

- MGT 212 - Chapter 1 (Part 1) - Managers and You in The WorkplaceDocument27 pagesMGT 212 - Chapter 1 (Part 1) - Managers and You in The WorkplaceHidden UniverseNo ratings yet

- MGT 212 - Chapter 1 (Part 1) - Managers and You in The WorkplaceDocument27 pagesMGT 212 - Chapter 1 (Part 1) - Managers and You in The WorkplaceHidden UniverseNo ratings yet

- MGT 212 - Chapter 1 (Part 1) - Managers and You in The WorkplaceDocument27 pagesMGT 212 - Chapter 1 (Part 1) - Managers and You in The WorkplaceHidden UniverseNo ratings yet

- A Report On Information Communication Technology ICT Sector of BangladeshDocument17 pagesA Report On Information Communication Technology ICT Sector of BangladeshS M Shamim শামীমNo ratings yet

- Management Information System. MIS-107Document9 pagesManagement Information System. MIS-107Hidden UniverseNo ratings yet

- Midterm Fin Oo4Document82 pagesMidterm Fin Oo4patricia gunio100% (1)

- Jollibee Audited FsDocument88 pagesJollibee Audited FsCedric Adams50% (2)

- Company Profile ShineWing Indonesia 2020Document19 pagesCompany Profile ShineWing Indonesia 2020cindy wiriaatmadjaNo ratings yet

- Chapter 2Document27 pagesChapter 2yewjie100% (1)

- Group 2 Auditing and Corporate GovernanceDocument18 pagesGroup 2 Auditing and Corporate GovernanceAmaan SaifiNo ratings yet

- Audit ReportsDocument46 pagesAudit ReportsJamaNo ratings yet

- Cag Duties and Powers of The Comptroller and Auditor General of India PDFDocument7 pagesCag Duties and Powers of The Comptroller and Auditor General of India PDFAshish Singh NegiNo ratings yet

- BPM-Financial Modelling Fundamentals-Practical ExerciseDocument24 pagesBPM-Financial Modelling Fundamentals-Practical ExerciseSiddharth GuptaNo ratings yet

- Laundry Shop Transactions August 2020Document11 pagesLaundry Shop Transactions August 2020Donabelle Marimon0% (1)

- Chapter 07 - Inventory Costing and COGSDocument12 pagesChapter 07 - Inventory Costing and COGSxxmbetaNo ratings yet

- Grant Thornton Business COmbination PDFDocument51 pagesGrant Thornton Business COmbination PDFPuneet SharmaNo ratings yet

- Shipment Monitoring FinalDocument303 pagesShipment Monitoring FinalArvin TejonesNo ratings yet

- Chapter 7. Student CH 7-14 Build A Model: AssetsDocument5 pagesChapter 7. Student CH 7-14 Build A Model: Assetsseth litchfieldNo ratings yet

- HUAWEIDocument18 pagesHUAWEIAswini Kumar BhuyanNo ratings yet

- 2014 Accounting Specimen Paper 1 Mark Scheme PDFDocument8 pages2014 Accounting Specimen Paper 1 Mark Scheme PDFSpike RockNo ratings yet

- Jollibee Foods Corporation Financial Statements and Independent Auditor's ReportDocument140 pagesJollibee Foods Corporation Financial Statements and Independent Auditor's Report채문길No ratings yet

- 2023 Course Outline FIA 214Document7 pages2023 Course Outline FIA 214Mika-eelNo ratings yet

- Boeing Stock Analysis ReportDocument2 pagesBoeing Stock Analysis ReportInvestingSidekick100% (1)

- Tutorial 6Document4 pagesTutorial 6NurSyazwaniRosliNo ratings yet

- Intercom PDocument20 pagesIntercom PLanze Micheal LadrillonoNo ratings yet

- 74845bos60515 FoundationDocument7 pages74845bos60515 Foundationshashank singhNo ratings yet

- BSA 2105 Business TaxDocument12 pagesBSA 2105 Business Taxkayeselle maclangNo ratings yet

- Dubai World Central Free ZoneDocument4 pagesDubai World Central Free ZoneKpiDubaiNo ratings yet

- Finance & Account Executive with 6+ years of SAP FICO experienceDocument3 pagesFinance & Account Executive with 6+ years of SAP FICO experienceSHIVANANDNo ratings yet

- Deb Stevens' Resignation LetterDocument3 pagesDeb Stevens' Resignation LetterDenise NelsonNo ratings yet

- M. Com Advanced Accounting II Sem C.No. 211Document342 pagesM. Com Advanced Accounting II Sem C.No. 211hariNo ratings yet

- Senior High School Department: Quarter 3 - Module 11: Preparing Trial BalanceDocument8 pagesSenior High School Department: Quarter 3 - Module 11: Preparing Trial BalanceJaye RuantoNo ratings yet

- Syllabus in Accounting Information SystemDocument7 pagesSyllabus in Accounting Information SystemJinx Cyrus Rodillo100% (1)

- Tugas Latihan 4 PDFDocument2 pagesTugas Latihan 4 PDFRadit Ramdan NopriantoNo ratings yet