You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Additional Financial Reporting Issuesch8Document25 pagesAdditional Financial Reporting Issuesch8muudey sheikhNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Package 1Document141 pagesPackage 1muudey sheikhNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- As-9 Revenue RecognitionDocument6 pagesAs-9 Revenue Recognitionmuudey sheikhNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Depreciation Accounting PPT at BEC DOMSDocument19 pagesDepreciation Accounting PPT at BEC DOMSmuudey sheikh100% (1)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Cash Is The Most Important Aspect of Operating A BusinessDocument5 pagesCash Is The Most Important Aspect of Operating A Businessmuudey sheikhNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Chapter Three: Opportunity Cost of Capital and Capital BudgetingDocument20 pagesChapter Three: Opportunity Cost of Capital and Capital Budgetingmuudey sheikhNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Usefulness of Accounting Information To Investors and CreditorsDocument19 pagesUsefulness of Accounting Information To Investors and Creditorsmuudey sheikhNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Chapter Ten: Criticisms of Absorption Cost Systems: Incentive To OverproduceDocument16 pagesChapter Ten: Criticisms of Absorption Cost Systems: Incentive To Overproducemuudey sheikhNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Chapter Six: Budgets and BudgetingDocument21 pagesChapter Six: Budgets and Budgetingmuudey sheikhNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Chapter Eight: Cost Allocation: PracticesDocument20 pagesChapter Eight: Cost Allocation: Practicesmuudey sheikhNo ratings yet

- Network Analysis Part 5 Minimum DurationDocument17 pagesNetwork Analysis Part 5 Minimum Durationmuudey sheikhNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Chapter 10 7e SolutionsDocument33 pagesChapter 10 7e Solutionsmuudey sheikhNo ratings yet

- Grizzly Bears: in British ColumbiaDocument6 pagesGrizzly Bears: in British Columbiamuudey sheikhNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Chapter 8 7e SolutionsDocument50 pagesChapter 8 7e Solutionsmuudey sheikhNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Topic 1 - Introduction To Technical AnalysisDocument11 pagesTopic 1 - Introduction To Technical AnalysisZatch Series UnlimitedNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Bond ValuationDocument19 pagesBond ValuationJANHVI HEDANo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Haas UG Courses For CPA Licensure 1Document4 pagesHaas UG Courses For CPA Licensure 1asim riazNo ratings yet

- A Case Study in Transforming of Retail Stock TradeDocument24 pagesA Case Study in Transforming of Retail Stock Tradeapi-3835230No ratings yet

- Economic Activity and Financial VolatilityDocument16 pagesEconomic Activity and Financial VolatilityKamil Mehdi AbbasNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Corporate LiquidationDocument6 pagesCorporate LiquidationJBNo ratings yet

- 2022 - CLC - Securities and Investment Analysis - ACBSP FormatDocument9 pages2022 - CLC - Securities and Investment Analysis - ACBSP Formatpthieuanh123No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- CPG Financial Model and Valuation v2Document10 pagesCPG Financial Model and Valuation v2Mohammed YASEENNo ratings yet

- Computational Finance An Introductory Course With RDocument305 pagesComputational Finance An Introductory Course With RMCA89% (9)

- 3rd Sem Question Bank PDFDocument79 pages3rd Sem Question Bank PDFMausam Ghimire67% (3)

- CFA L-2 Performance Tracker '23Document11 pagesCFA L-2 Performance Tracker '23AradhyaNo ratings yet

- (1.2) FS Analysis ReviewerDocument3 pages(1.2) FS Analysis ReviewerstgcastillonesNo ratings yet

- PORTFOLIO MANAGEMENT SERVICES - AN INVESTMENT OPTION Sharekhan 2Document73 pagesPORTFOLIO MANAGEMENT SERVICES - AN INVESTMENT OPTION Sharekhan 2niceprachi0% (1)

- Value Line PublishingDocument11 pagesValue Line PublishingIrka Dewi Tanemaru100% (3)

- Chapter 12 LiabilitiesDocument5 pagesChapter 12 LiabilitiesAngelica Joy ManaoisNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Chapter 5Document25 pagesChapter 5Tanzeel HussainNo ratings yet

- Ford Inc Statement of Financial PositionDocument3 pagesFord Inc Statement of Financial PositionTina PascualNo ratings yet

- 11-Managing Interest Rate Risk GAPDocument26 pages11-Managing Interest Rate Risk GAPNongnectar NamwhanNo ratings yet

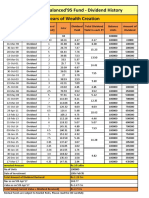

- Dividend HistoryDocument1 pageDividend HistoryJeetendra KumarNo ratings yet

- Forex Indicators GuideDocument2 pagesForex Indicators GuideMike Ng0% (2)

- PROOF OF CASH - DIT and OC - Answers in Sample ProbsDocument4 pagesPROOF OF CASH - DIT and OC - Answers in Sample ProbsGilbert MoralesNo ratings yet

- In Problem 10 16 We Projected Financial Statements For Wal Mart Stores 126776Document2 pagesIn Problem 10 16 We Projected Financial Statements For Wal Mart Stores 126776Amit PandeyNo ratings yet

- Corporate Finance Theory: Formula SheetDocument5 pagesCorporate Finance Theory: Formula SheeticeslothNo ratings yet

- ACFINA2 SyllabusDocument6 pagesACFINA2 SyllabusabbyNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- RAMACHANDRANDocument40 pagesRAMACHANDRANYoges YogeswaranNo ratings yet

- Financing of Project: DR Anurag AgnihotriDocument79 pagesFinancing of Project: DR Anurag AgnihotriAnvesha TyagiNo ratings yet

- InvestDocument7 pagesInvestsweetyNo ratings yet

- ACC 202 - Financial Accounting IIDocument6 pagesACC 202 - Financial Accounting IIRahul raj SahNo ratings yet

- Replicate Vix in SpreadsheetDocument12 pagesReplicate Vix in Spreadsheetbearsq0% (1)

- ENTREPRENEURSHIP Q1 Module 4Document13 pagesENTREPRENEURSHIP Q1 Module 4sbeachariceNo ratings yet