You might also like

- Investing with Intelligent ETFs: Strategies for Profiting from the New Breed of SecuritiesFrom EverandInvesting with Intelligent ETFs: Strategies for Profiting from the New Breed of SecuritiesNo ratings yet

- ReillyBrown CH 8 2019Document48 pagesReillyBrown CH 8 2019Aaron HoardNo ratings yet

- ReillyBrown IAPM 11e PPT Ch08Document97 pagesReillyBrown IAPM 11e PPT Ch08rocky wongNo ratings yet

- Chapter 2 - QLDMDTDocument44 pagesChapter 2 - QLDMDTDUYÊN NGUYỄN THỊ MINHNo ratings yet

- ReillyBrown Chapter 9 Fall 2019Document50 pagesReillyBrown Chapter 9 Fall 2019Aaron HoardNo ratings yet

- Tahap-Tahap Penelitian EksperimenDocument11 pagesTahap-Tahap Penelitian EksperimenRicky TampubolonNo ratings yet

- ReillyBrown IAPM 11e PPT Ch02Document72 pagesReillyBrown IAPM 11e PPT Ch02rocky wongNo ratings yet

- ReillyBrown CH 6 2019Document36 pagesReillyBrown CH 6 2019Aaron HoardNo ratings yet

- Nhà quản lý có lý trí và nhà đầu tư thiếu lý tríDocument18 pagesNhà quản lý có lý trí và nhà đầu tư thiếu lý tríTuyết Anh ChuNo ratings yet

- ReillyBrown IAPM 11e PPT Ch06Document67 pagesReillyBrown IAPM 11e PPT Ch06rocky wongNo ratings yet

- Equity Portfolio MGT Strategies Study NotesDocument8 pagesEquity Portfolio MGT Strategies Study Notesbegad.hazemNo ratings yet

- Chapter 15: Equity Portfolio Management Strategies: Analysis of Investments Management of PortfoliosDocument33 pagesChapter 15: Equity Portfolio Management Strategies: Analysis of Investments Management of PortfoliosKavithra KalimuthuNo ratings yet

- Investment Analysis and Portfolio Management 11th Edition Reilly Solutions ManualDocument15 pagesInvestment Analysis and Portfolio Management 11th Edition Reilly Solutions Manualcarriboo.continuo.h591tv100% (20)

- CH 9 PowerpointDocument12 pagesCH 9 PowerpointiisrasyidiNo ratings yet

- ReillyBrown IAPM 11e PPT Ch01Document53 pagesReillyBrown IAPM 11e PPT Ch01rocky wong100% (1)

- AGibson 12e Ch01 AISEDocument29 pagesAGibson 12e Ch01 AISEAbdirahman AdenNo ratings yet

- ReillyBrown IAPM 11e PPT Ch05Document81 pagesReillyBrown IAPM 11e PPT Ch05rocky wongNo ratings yet

- Corporate Governance: PART 3 Strategic Actions: Strategy ImplementationDocument36 pagesCorporate Governance: PART 3 Strategic Actions: Strategy ImplementationBaba YagaNo ratings yet

- Strategic Management: Concepts and Cases 9eDocument30 pagesStrategic Management: Concepts and Cases 9egusti sandhiNo ratings yet

- Chapter 16: Equity Portfolio Management StrategiesDocument29 pagesChapter 16: Equity Portfolio Management StrategiesMohamed HammadNo ratings yet

- C 1Document33 pagesC 1Tử Đằng NguyễnNo ratings yet

- Chapter 5Document8 pagesChapter 5Helmi MohrabNo ratings yet

- Chapter 13 Financial Markets Saving InvestmentDocument61 pagesChapter 13 Financial Markets Saving Investmentlei dcNo ratings yet

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument38 pagesInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownAssfaw KebedeNo ratings yet

- Chap 11 Equity StrategiesDocument72 pagesChap 11 Equity StrategiesYibeltal AssefaNo ratings yet

- Palepu - Chapter 5Document33 pagesPalepu - Chapter 5Dương Quốc TuấnNo ratings yet

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument30 pagesInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownMahmoud M. SulaimanNo ratings yet

- Merger and Acquisition StrategiesDocument45 pagesMerger and Acquisition Strategies--bolabolaNo ratings yet

- CH01 HittDocument16 pagesCH01 HittNurul MaulidaNo ratings yet

- Lecture # 3Document18 pagesLecture # 3salman soomroNo ratings yet

- Chapter 19 Equity Portfolio ManagementDocument32 pagesChapter 19 Equity Portfolio ManagementkegnataNo ratings yet

- Presenting: Equity ManagementDocument44 pagesPresenting: Equity ManagementMohamed HammadNo ratings yet

- Financial Statement Analysis: Charles H. GibsonDocument22 pagesFinancial Statement Analysis: Charles H. GibsonGud BooyNo ratings yet

- Variable Costing For Management Analysis: Managerial Accounting 14eDocument37 pagesVariable Costing For Management Analysis: Managerial Accounting 14ecykenNo ratings yet

- ReillyBrown IAPM 11e PPT Ch12Document68 pagesReillyBrown IAPM 11e PPT Ch12rocky wongNo ratings yet

- Chap. 8. Facility and Work DesignDocument32 pagesChap. 8. Facility and Work DesignRonaldo ConventoNo ratings yet

- Chapter 32 A Macroeconomic Theory of The Open EconomyDocument40 pagesChapter 32 A Macroeconomic Theory of The Open EconomyThảo Linh Vũ NguyễnNo ratings yet

- DTU406 - Lecture 4 - Equity Portfolio ManagementDocument20 pagesDTU406 - Lecture 4 - Equity Portfolio ManagementThuc NguyenNo ratings yet

- Chapter 4Document33 pagesChapter 4noremiNo ratings yet

- INS3032 Chap 1Document45 pagesINS3032 Chap 1Lan Hương VũNo ratings yet

- An Overview of Financial ManagementDocument11 pagesAn Overview of Financial ManagementJanelle Khoo Pei XinNo ratings yet

- Cooperative Strategy PresentationDocument22 pagesCooperative Strategy PresentationSheikaina Mia SiacorNo ratings yet

- Lecture 10 - Corporate Governance PDFDocument37 pagesLecture 10 - Corporate Governance PDFjefribasiuni1517No ratings yet

- FM02 Ch01 ShowDocument53 pagesFM02 Ch01 ShowGunadi SetyawanNo ratings yet

- Inbound 296364456828209019Document23 pagesInbound 296364456828209019joergielav29No ratings yet

- Lecture 5Document52 pagesLecture 5Karissa TanNo ratings yet

- Chapter 5 The Performance of Nontraditional Banking CompaniesDocument37 pagesChapter 5 The Performance of Nontraditional Banking CompaniesIsrael AldereteNo ratings yet

- Chapter 4 Project Integration ManagementDocument36 pagesChapter 4 Project Integration Managementdhoon1223No ratings yet

- Session 3-Intrinsic Valuation-IDocument22 pagesSession 3-Intrinsic Valuation-IHariSharanPanjwaniNo ratings yet

- Chapter 1 OPerations Management and Value ChainDocument31 pagesChapter 1 OPerations Management and Value ChainNadine LumanogNo ratings yet

- 6205 LectureDocument27 pages6205 Lectureapi-3699305No ratings yet

- MSC - Chapter 07Document58 pagesMSC - Chapter 07isratjahanchandmoniNo ratings yet

- Corporate FinanceDocument15 pagesCorporate FinanceWilliam OngNo ratings yet

- Mutual FundsDocument36 pagesMutual FundsShodasakshari VidyaNo ratings yet

- Hitt13e PPT Ch07Document46 pagesHitt13e PPT Ch07Alaa ShaathNo ratings yet

- Chapter 11Document44 pagesChapter 11Ishita SoodNo ratings yet

- FINC6001Document28 pagesFINC6001fodskofkdsofkdsoNo ratings yet

- Chapter 15 (Equity Portfolio Management Strategies)Document24 pagesChapter 15 (Equity Portfolio Management Strategies)Abuzafar Abdullah100% (1)

- International Financial Management 13 Edition: by Jeff MaduraDocument19 pagesInternational Financial Management 13 Edition: by Jeff MaduraAbdulaziz Al-amroNo ratings yet

- AGibson 12e Ch06 AISEDocument42 pagesAGibson 12e Ch06 AISEYi QiNo ratings yet

- Residential Real Estate Introduction Slides - Student Version-1Document120 pagesResidential Real Estate Introduction Slides - Student Version-1Aaron HoardNo ratings yet

- ReillyBrown CH 6 2019Document36 pagesReillyBrown CH 6 2019Aaron HoardNo ratings yet

- Be Water, Be Changing: "You" Is A Fluid Concept, and Your Greatest Asset. Be AdaptableDocument1 pageBe Water, Be Changing: "You" Is A Fluid Concept, and Your Greatest Asset. Be AdaptableAaron HoardNo ratings yet

- Need Some Perspective? Step Back and See The Big Picture WithDocument1 pageNeed Some Perspective? Step Back and See The Big Picture WithAaron HoardNo ratings yet

- StorytellingDocument1 pageStorytellingAaron HoardNo ratings yet

- 201220-20CTRL Alt Del Eng2Document60 pages201220-20CTRL Alt Del Eng2Aaron HoardNo ratings yet

- Toxic LeadershipDocument1 pageToxic LeadershipAaron HoardNo ratings yet

- The Science of Pep TalksDocument1 pageThe Science of Pep TalksAaron HoardNo ratings yet

- Externalities: The Effect of A Transaction of Two Individuals On A Third Party Who Does Not Consent To The TransactionDocument1 pageExternalities: The Effect of A Transaction of Two Individuals On A Third Party Who Does Not Consent To The TransactionAaron HoardNo ratings yet

- MotivationDocument1 pageMotivationAaron HoardNo ratings yet

- THE Ultron Principle: They'Re Just Like PeopleDocument1 pageTHE Ultron Principle: They'Re Just Like PeopleAaron HoardNo ratings yet

- Altruism and Cooperation SlidesDocument38 pagesAltruism and Cooperation SlidesAaron HoardNo ratings yet

- InviteDocument1 pageInviteAaron HoardNo ratings yet

- Bring A BookDocument1 pageBring A BookAaron HoardNo ratings yet

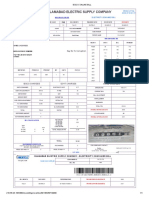

- Islamabad Electric Supply Company: Say No To CorruptionDocument1 pageIslamabad Electric Supply Company: Say No To CorruptionAhmed AliNo ratings yet

- CVP BEP Analysis. Assignments, (In Class) : RequiredDocument3 pagesCVP BEP Analysis. Assignments, (In Class) : Requiredmuhammed shadNo ratings yet

- Demand & Supply: Elasticities & Government-Set PricesDocument33 pagesDemand & Supply: Elasticities & Government-Set PricesSaadatNo ratings yet

- Quiz Semana 3 Introduction To Derivative Securities Pregunta 1Document5 pagesQuiz Semana 3 Introduction To Derivative Securities Pregunta 1Alejandro Forero0% (1)

- Supply and Demand: Managerial Economics: Economic Tools For Today's Decision Makers, 4/e by Paul Keat and Philip YoungDocument42 pagesSupply and Demand: Managerial Economics: Economic Tools For Today's Decision Makers, 4/e by Paul Keat and Philip YoungGAYLY ANN TOLENTINONo ratings yet

- Valuation of Securities 1 - TBPDocument2 pagesValuation of Securities 1 - TBPShaina Monique RangasanNo ratings yet

- Assign 3Document1 pageAssign 3Acua RioNo ratings yet

- Research Proposal EcoDocument30 pagesResearch Proposal EcoMichael SmithNo ratings yet

- 3kVA Quote Jeff (Pylontech Battery)Document1 page3kVA Quote Jeff (Pylontech Battery)az PhillipsNo ratings yet

- Gavin's VSA Trading Plan - Extended Edition (Tom Williams Additional Comments)Document10 pagesGavin's VSA Trading Plan - Extended Edition (Tom Williams Additional Comments)Govind SinghNo ratings yet

- Chester Capsim Report I Professor FeedbackDocument8 pagesChester Capsim Report I Professor Feedbackparamjit badyal100% (1)

- Breakeven Point: Anand R.DeshpandeDocument19 pagesBreakeven Point: Anand R.DeshpandeLIBIN JOSENo ratings yet

- Chapter 5, David Besanko Microeconomics. Assignment2.KobraDocument6 pagesChapter 5, David Besanko Microeconomics. Assignment2.KobrabaqirNo ratings yet

- 7 Best Futures Trading Strategies You Can Use (And 3 To Avoid!) - My Trading SkillsDocument1 page7 Best Futures Trading Strategies You Can Use (And 3 To Avoid!) - My Trading SkillsOussama bensaoudNo ratings yet

- Business Mathematics First Quarter ExaminationDocument2 pagesBusiness Mathematics First Quarter ExaminationTeds TV100% (1)

- Faculty - Accountancy - 2022 - Session 1 - Diploma - Maf251Document7 pagesFaculty - Accountancy - 2022 - Session 1 - Diploma - Maf251NUR FARISHA MOHD AZHARNo ratings yet

- Challenges of International BusinessDocument4 pagesChallenges of International BusinessRikesh SapkotaNo ratings yet

- Candlestick and Volume Analysis PDFDocument2 pagesCandlestick and Volume Analysis PDFthe futureNo ratings yet

- Levi Case StudyDocument2 pagesLevi Case StudyTyler TidbadNo ratings yet

- Stock Market Course ContentDocument12 pagesStock Market Course ContentSrikanth SanipiniNo ratings yet

- WorkBench Case SolutionsDocument6 pagesWorkBench Case SolutionsNihar Ranjan Padhy100% (1)

- Dokumen - Tips - Transfer Pricing QuizDocument5 pagesDokumen - Tips - Transfer Pricing QuizSaeym SegoviaNo ratings yet

- Level 1 Number Operations 2 v2 AnswersDocument8 pagesLevel 1 Number Operations 2 v2 Answersshane sheppardNo ratings yet

- E. All of The Above. A. Total Revenue Equals Total CostDocument22 pagesE. All of The Above. A. Total Revenue Equals Total CostNicole KimNo ratings yet

- Homework 4 (Economics)Document2 pagesHomework 4 (Economics)DeGOAT UyNo ratings yet

- Budget Line QuestionsDocument18 pagesBudget Line QuestionsmanishNo ratings yet

- Paper 14: Strategic Financial Management (SFM) 100 MarksDocument4 pagesPaper 14: Strategic Financial Management (SFM) 100 MarksSridhanyas kitchenNo ratings yet

- Math Word Problems Extension 34 16Document2 pagesMath Word Problems Extension 34 16woof1800No ratings yet

- MTP 1 May 21 QDocument4 pagesMTP 1 May 21 QSampath KumarNo ratings yet

- Something Darvas, Something New: Modifying The Darvas Technique For Today's MarketsDocument5 pagesSomething Darvas, Something New: Modifying The Darvas Technique For Today's MarketsPRABHASH SINGH0% (1)