You might also like

- Merged Midterm SomeDocument92 pagesMerged Midterm SomeAbhay SahuNo ratings yet

- 3014accounting For ManagementDocument2 pages3014accounting For ManagementSatyanarayana AmarapinniNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Overheads: Allocation, Apportionment & AbsorptionDocument39 pagesOverheads: Allocation, Apportionment & AbsorptionManju DoreNo ratings yet

- Chapter - 01 - Overview - of - Management - Accounting - Doc - Filename UTF-8''Chapter 01 Overview of Management AccountingDocument3 pagesChapter - 01 - Overview - of - Management - Accounting - Doc - Filename UTF-8''Chapter 01 Overview of Management AccountingNasrinTonni AhmedNo ratings yet

- Time Value of Money: Production and Operations Management - R B Khanna © Prentice Hall IndiaDocument130 pagesTime Value of Money: Production and Operations Management - R B Khanna © Prentice Hall IndiararaNo ratings yet

- ABC vs Traditional Costing MethodsDocument54 pagesABC vs Traditional Costing MethodsTaufik AhmmedNo ratings yet

- Financial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsDocument55 pagesFinancial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsmukul3087_305865623No ratings yet

- 53 Activity Based CostingDocument19 pages53 Activity Based CostingUmar SulemanNo ratings yet

- Chapter 2Document15 pagesChapter 2Tiya AmuNo ratings yet

- CIMA - P2 - Performance Management - Specimen Papers - Qs - Nov - 2009Document16 pagesCIMA - P2 - Performance Management - Specimen Papers - Qs - Nov - 2009e_NomadNo ratings yet

- Final Term Exam - Managerial Accounting - Summer 2020 11092020 103926pmDocument2 pagesFinal Term Exam - Managerial Accounting - Summer 2020 11092020 103926pmAbdul SamiNo ratings yet

- Short Term Decision Making: Vincent Joseph D. Disu, CPPS, MbaDocument22 pagesShort Term Decision Making: Vincent Joseph D. Disu, CPPS, MbaMaria Maganda MalditaNo ratings yet

- Unit IiDocument6 pagesUnit Iisalagar_meNo ratings yet

- Module 2 Replacement MethodsDocument51 pagesModule 2 Replacement MethodsRamees KpNo ratings yet

- PERT and CPM Project Management TechniquesDocument39 pagesPERT and CPM Project Management TechniquesNiruban So CoolNo ratings yet

- Cost AllocationDocument52 pagesCost Allocationalafitoso MedinaNo ratings yet

- Answer: Cost of Raw Material Consumed 500,000Document6 pagesAnswer: Cost of Raw Material Consumed 500,000Tabish KhanNo ratings yet

- DocumentDocument5 pagesDocumentNUR ADILAHNo ratings yet

- Methos of PricingDocument18 pagesMethos of PricingKhelin ShahNo ratings yet

- Midterm ExaminationDocument33 pagesMidterm ExaminationEmmanuel VillafuerteNo ratings yet

- Foundations in Accountancy Ffa/Acca F: Nguyen Thi Phuong Mai (PHD, Cpa VN) Email: Maintp@Ftu - Edu.VnDocument166 pagesFoundations in Accountancy Ffa/Acca F: Nguyen Thi Phuong Mai (PHD, Cpa VN) Email: Maintp@Ftu - Edu.VnMy TranNo ratings yet

- Midterm Examination Review - Strategic Cost ManagementDocument67 pagesMidterm Examination Review - Strategic Cost ManagementEmmanuel VillafuerteNo ratings yet

- Cost and Management AccountingDocument5 pagesCost and Management AccountingSolve AssignmentNo ratings yet

- ACTIVITY BASED COSTING EXPLAINEDDocument13 pagesACTIVITY BASED COSTING EXPLAINEDDiwakar Entertainment DoseNo ratings yet

- Managerial Accounting by James JiambalvoDocument52 pagesManagerial Accounting by James JiambalvoAhmed AliNo ratings yet

- Scm.1 - Strategic Management AccountingDocument20 pagesScm.1 - Strategic Management AccountingPrincess BersaminaNo ratings yet

- BTEC Level 4 HND Diploma in Business Final Examination FrontsheetDocument5 pagesBTEC Level 4 HND Diploma in Business Final Examination FrontsheetTri HaNo ratings yet

- 5 Fun ConceptDocument6 pages5 Fun ConceptBhavuk SharmaNo ratings yet

- Lab 4Document7 pagesLab 4abu hasanNo ratings yet

- OutputDocument85 pagesOutputKwame Simpe OforiNo ratings yet

- MG WE FNSACC517 Provide Management Accounting InformationDocument9 pagesMG WE FNSACC517 Provide Management Accounting InformationGurpreet KaurNo ratings yet

- Standard Costing - Answer KeyDocument6 pagesStandard Costing - Answer KeyRoselyn LumbaoNo ratings yet

- Cga-Canada Management Accounting Fundamentals (Ma1) Examination March 2014 Marks Time: 3 HoursDocument18 pagesCga-Canada Management Accounting Fundamentals (Ma1) Examination March 2014 Marks Time: 3 HoursasNo ratings yet

- NewCh09 In-Class Problems, Horngren13e-MY COPY (X2)Document11 pagesNewCh09 In-Class Problems, Horngren13e-MY COPY (X2)nataizyaNo ratings yet

- Costing PresentationDocument16 pagesCosting PresentationSarah Jane Ste MarieNo ratings yet

- Property, Plant and EquipmentDocument66 pagesProperty, Plant and EquipmentThanos The titanNo ratings yet

- Job Costing and Balance Scorecard NotesDocument4 pagesJob Costing and Balance Scorecard NotesArun HariharanNo ratings yet

- Two-Dimensional ABC and Activity-Based Costing ViewDocument19 pagesTwo-Dimensional ABC and Activity-Based Costing ViewSneha BajpaiNo ratings yet

- Paper - 4: Cost Accounting and Financial Management Section A: Cost Accounting QuestionsDocument22 pagesPaper - 4: Cost Accounting and Financial Management Section A: Cost Accounting QuestionsSneha VermaNo ratings yet

- Chapter 5 Just in Time and Backflush AccountingDocument11 pagesChapter 5 Just in Time and Backflush AccountingSteffany RoqueNo ratings yet

- Management Accounting For Financial ServicesDocument4 pagesManagement Accounting For Financial ServicesMuhammad KashifNo ratings yet

- Advance Cost & Management AccountingDocument3 pagesAdvance Cost & Management AccountingRana Adnan SaifNo ratings yet

- Management Accounting & Decisions II - Activity-Based CostingDocument24 pagesManagement Accounting & Decisions II - Activity-Based CostingDouglas Leong Jian-HaoNo ratings yet

- Incremental Analysis: Relevant Costs for Specific DecisionsDocument5 pagesIncremental Analysis: Relevant Costs for Specific DecisionsEdilyn Joy Flores SalaNo ratings yet

- CHAPTER 4: Differential Cost Analysis (Relevant Costing) KaebDocument6 pagesCHAPTER 4: Differential Cost Analysis (Relevant Costing) KaebMark Gelo WinchesterNo ratings yet

- Vol 1. Advanced Management Accounting - CVP Analysis and Decision MakingDocument41 pagesVol 1. Advanced Management Accounting - CVP Analysis and Decision MakingvishnuvermaNo ratings yet

- (C-4.1) 5. Overheads - FormattedDocument30 pages(C-4.1) 5. Overheads - FormattedSam KingNo ratings yet

- Mas Ho No. 2 Relevant CostingDocument7 pagesMas Ho No. 2 Relevant CostingRenz Francis LimNo ratings yet

- AccountingDocument4 pagesAccountingLemuel ReñaNo ratings yet

- Budgeting 101: By: Limheya Lester Glenn National University-ManilaDocument42 pagesBudgeting 101: By: Limheya Lester Glenn National University-ManilaXXXXXXXXXXXXXXXXXXNo ratings yet

- ABC Costing and Activity-Based ManagementDocument30 pagesABC Costing and Activity-Based ManagementSyifa Putri MaharaniNo ratings yet

- Activity Based CostingDocument49 pagesActivity Based CostingEdson EdwardNo ratings yet

- FM 02Document4 pagesFM 02Jimit ShahNo ratings yet

- Assignment 6Document2 pagesAssignment 6Geoff MacarateNo ratings yet

- Decision Making and Relevant InformationDocument78 pagesDecision Making and Relevant InformationAbdul Rehman SubhanNo ratings yet

- Chapter04 000 PDFDocument27 pagesChapter04 000 PDFgracel angela tolejanoNo ratings yet

- 1-Delivering Quality Services of SME-Based Construction Firms in The Philippines PDFDocument6 pages1-Delivering Quality Services of SME-Based Construction Firms in The Philippines PDFjbjuanzonNo ratings yet

- Improving Inventory Control and Customer Loyalty at Confetti ShoesDocument4 pagesImproving Inventory Control and Customer Loyalty at Confetti ShoesJulmar Joseph Misa100% (1)

- FP Lean Warehouse OperationsDocument8 pagesFP Lean Warehouse OperationsIbrahim SkakriNo ratings yet

- Financial Investment ExercisesDocument16 pagesFinancial Investment ExercisesBội Ngọc100% (1)

- National Research Foundation to Boost India's Research OutputDocument48 pagesNational Research Foundation to Boost India's Research OutputR JayalathNo ratings yet

- Shariah Princiles in Islamic Securities Bba, Murabahah, Istisna & SalamDocument47 pagesShariah Princiles in Islamic Securities Bba, Murabahah, Istisna & Salamilyan_izaniNo ratings yet

- Final Year Project Proposal Presentation Group #13Document14 pagesFinal Year Project Proposal Presentation Group #13Usama JahangirNo ratings yet

- Money Market FinalDocument6 pagesMoney Market FinalPriyanka SharmaNo ratings yet

- 10 Pay With Return of Premium of MR SrinivasDocument4 pages10 Pay With Return of Premium of MR SrinivasvasuNo ratings yet

- Rural Marketing 260214 PDFDocument282 pagesRural Marketing 260214 PDFarulsureshNo ratings yet

- BSc Management Financial Accounting Assignment Cash BudgetDocument17 pagesBSc Management Financial Accounting Assignment Cash BudgetNethmi JayawardhanaNo ratings yet

- 3 Absorption Vs Variable CostingDocument16 pages3 Absorption Vs Variable CostingXyril MañagoNo ratings yet

- Income DistributionDocument5 pagesIncome DistributionRishiiieeeznNo ratings yet

- The MRP II Hierarchy Planning FrameworkDocument17 pagesThe MRP II Hierarchy Planning FrameworkPrasath KmkNo ratings yet

- Gulayan Sa Paaralan 2023 Project ProposalDocument3 pagesGulayan Sa Paaralan 2023 Project ProposalP Olarte ESNo ratings yet

- Chapter I: Management and The Nature of Management AccountingDocument11 pagesChapter I: Management and The Nature of Management AccountingMark ManuntagNo ratings yet

- Dell LBO model case studyDocument21 pagesDell LBO model case studyMohd IzwanNo ratings yet

- Japan Since 1980Document330 pagesJapan Since 1980JianBre100% (3)

- Dachser MG PDFDocument24 pagesDachser MG PDFWan Sek ChoonNo ratings yet

- ABC Implementation Ethics Cma Adapted Applewood ElectronicDocument2 pagesABC Implementation Ethics Cma Adapted Applewood Electronictrilocksp SinghNo ratings yet

- Dampak Globalisasi terhadap Akuntansi dan Konvergensi PSAK ke IFRSDocument34 pagesDampak Globalisasi terhadap Akuntansi dan Konvergensi PSAK ke IFRSAdi Al HadiNo ratings yet

- Management of Financial Services PDFDocument76 pagesManagement of Financial Services PDFManisha Nagpal100% (1)

- Congo Whitepaper 9.2019Document12 pagesCongo Whitepaper 9.2019Gostino Lok100% (2)

- Internet Marketing Plan GuideDocument5 pagesInternet Marketing Plan GuideMario MitevskiNo ratings yet

- Logbook Gac022Document6 pagesLogbook Gac022PaulinaNo ratings yet

- Riskandreturnanalysisof NSEcompaniesDocument5 pagesRiskandreturnanalysisof NSEcompaniesSHIVANI CHAVANNo ratings yet

- SC rules on scope and limitations of taxation, tax vs regulatory feesDocument23 pagesSC rules on scope and limitations of taxation, tax vs regulatory feesArrianne ObiasNo ratings yet

- Cooperatives and Rural MarketsDocument168 pagesCooperatives and Rural MarketsDhanraj WaghmareNo ratings yet

- SBN 473Document27 pagesSBN 473Admin DivisionNo ratings yet

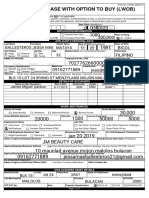

- Lwob - Application-Form Edited Edited EditedDocument2 pagesLwob - Application-Form Edited Edited Editedjessamaeballesteros21100% (1)