You might also like

- "Pic Carpet": Lucknow University A Business Plan ONDocument33 pages"Pic Carpet": Lucknow University A Business Plan ONPranav60% (5)

- Demand Worksheet PDFDocument2 pagesDemand Worksheet PDFDipti NagarNo ratings yet

- Mountain of Monopoly ProblemsDocument8 pagesMountain of Monopoly ProblemsPatricia Borjas GomezNo ratings yet

- Strategic Management Report - National FoodsDocument24 pagesStrategic Management Report - National Foodssana100% (4)

- Supply, Demand and Market Equilibrium: Ka-Fu WongDocument65 pagesSupply, Demand and Market Equilibrium: Ka-Fu WongGavin SayogoNo ratings yet

- Lecture 3Document53 pagesLecture 3Zong Zheng SunNo ratings yet

- Supply and Demand: Mcgraw-Hill/IrwinDocument41 pagesSupply and Demand: Mcgraw-Hill/IrwinjackaccyouNo ratings yet

- Economics For Managers: Session 2 Introduction To Demand and SupplyDocument38 pagesEconomics For Managers: Session 2 Introduction To Demand and SupplyVipulNo ratings yet

- PGP Micro (Session 4)Document36 pagesPGP Micro (Session 4)sjkkjs jkzBkjNo ratings yet

- ECO2201 - Slides - 3.1 - Demand and SupplyDocument68 pagesECO2201 - Slides - 3.1 - Demand and Supplyjokerightwegmail.com joke1233No ratings yet

- Unit 8 Lesson 1Document12 pagesUnit 8 Lesson 1shermatt0No ratings yet

- Theory of Supply and Demand: Hall and Lieberman, 3 Edition, Thomson South-Western, Chapter 3Document61 pagesTheory of Supply and Demand: Hall and Lieberman, 3 Edition, Thomson South-Western, Chapter 3M Reza SyahputraNo ratings yet

- Supply Demand FacilDocument25 pagesSupply Demand FacilRemonNo ratings yet

- Demand NotesDocument38 pagesDemand NotesPriya YadavNo ratings yet

- ECONOMICSSUMMARY1WITHMCQDocument335 pagesECONOMICSSUMMARY1WITHMCQvasu174No ratings yet

- ECON1210 Price DiscriminationDocument48 pagesECON1210 Price DiscriminationTsz Ling CHANNo ratings yet

- Frank8e Chapter03 PPT FinalDocument44 pagesFrank8e Chapter03 PPT FinalNgọc Linh NguyễnNo ratings yet

- Frank8e Chapter03 PPT FinalDocument50 pagesFrank8e Chapter03 PPT Finalsanwal agrawalNo ratings yet

- Topic 3 - 4 - Demand and SupplyDocument90 pagesTopic 3 - 4 - Demand and Supplykiatang04No ratings yet

- Microeconomics: Principles of Economics (5ed)Document36 pagesMicroeconomics: Principles of Economics (5ed)Le Trinh Anh (K17 HCM)No ratings yet

- Module 5 & 6Document66 pagesModule 5 & 6esther031216No ratings yet

- Microeconomic Principles SPRING 2001 MIDTERM ONE - AnswersDocument13 pagesMicroeconomic Principles SPRING 2001 MIDTERM ONE - AnswersirsaNo ratings yet

- DemandDocument27 pagesDemandFatima UniaNo ratings yet

- Chap003-Supply and Demand-ProfDocument92 pagesChap003-Supply and Demand-ProfKiky MuzaqiNo ratings yet

- Demand, Supply, Equilibrium: Managerial Economics Reviewer For Quiz #2Document5 pagesDemand, Supply, Equilibrium: Managerial Economics Reviewer For Quiz #2Kimberly AnneNo ratings yet

- Unit - 2-Class SlidesDocument42 pagesUnit - 2-Class Slidescrissy fisherNo ratings yet

- Applied Econ Week 3 - SabDocument7 pagesApplied Econ Week 3 - SabColeen Heart Migue PortonNo ratings yet

- Elasticity and Its ApplicationDocument44 pagesElasticity and Its ApplicationchanpeinNo ratings yet

- Theory of Demand: Prepared By: Divina MonterolaDocument22 pagesTheory of Demand: Prepared By: Divina MonterolalhysNo ratings yet

- Microeconomics: Theory of Supply and DemandDocument59 pagesMicroeconomics: Theory of Supply and DemandhmxesbNo ratings yet

- Microeconomics: Theory of Supply and DemandDocument59 pagesMicroeconomics: Theory of Supply and Demandim_shahNo ratings yet

- Problem - Supply Demand Elastictity WelfareDocument2 pagesProblem - Supply Demand Elastictity WelfareBá Phong LêNo ratings yet

- Chapter 3 NotesDocument38 pagesChapter 3 NotesHanan MohamedNo ratings yet

- Lecture No 4 - Supply and DemandDocument72 pagesLecture No 4 - Supply and DemandAhsan AtifNo ratings yet

- Business Economics: Lecture - 2Document60 pagesBusiness Economics: Lecture - 2Tayyaba JawedNo ratings yet

- NEW Presentation III - Demand AnalysisDocument21 pagesNEW Presentation III - Demand AnalysisIshika AgarwalNo ratings yet

- Lesson 3 - Supply and DemandDocument43 pagesLesson 3 - Supply and DemandCharles Corporal ReyesNo ratings yet

- Macroeconomics - Arnold - Chapter 3Document21 pagesMacroeconomics - Arnold - Chapter 3tsam181618No ratings yet

- Economía de Minerales: Demand and UtilityDocument23 pagesEconomía de Minerales: Demand and UtilityLucasPedroTomacoBayotNo ratings yet

- Mod 1 Review FilesDocument14 pagesMod 1 Review FilesMakayla KrohseNo ratings yet

- Elasticity: Chapter in A NutshellDocument17 pagesElasticity: Chapter in A NutshellSeng TheamNo ratings yet

- Economics Supply and Demand PowerpointDocument25 pagesEconomics Supply and Demand PowerpointJoshua AsucroNo ratings yet

- Chapter 05Document13 pagesChapter 05Akram ApNo ratings yet

- MIC 3e SSG Ch4 PDFDocument14 pagesMIC 3e SSG Ch4 PDFJina NjNo ratings yet

- A Review On The Law of Supply and Demand (Part 1)Document25 pagesA Review On The Law of Supply and Demand (Part 1)Janiña NatividadNo ratings yet

- Replicating Options With Positions in Stock and Cash: Why The Principle Makes SenseDocument9 pagesReplicating Options With Positions in Stock and Cash: Why The Principle Makes Senselib_01No ratings yet

- Principles SSG Ch5Document13 pagesPrinciples SSG Ch5Tingwei HuangNo ratings yet

- Derivatives and HedgingsDocument60 pagesDerivatives and HedgingsHuynh Le Kim HaNo ratings yet

- Microeconomics 1Document5 pagesMicroeconomics 1James Ronald HeisenbergNo ratings yet

- CH 5 Elasticity and Its ApplicationDocument39 pagesCH 5 Elasticity and Its ApplicationSakibNo ratings yet

- Elasticity and Its ApplicationDocument38 pagesElasticity and Its ApplicationSwastikNo ratings yet

- Demand Supply and MarketDocument45 pagesDemand Supply and MarketAryan AggarwalNo ratings yet

- Module6 - Simple PricingDocument13 pagesModule6 - Simple PricingSindac, Maria Celiamel Gabrielle C.No ratings yet

- Unit 2market Diagram and Market EquilibriumDocument57 pagesUnit 2market Diagram and Market Equilibriumcrissy fisherNo ratings yet

- UntitledDocument2 pagesUntitledwanNo ratings yet

- Dwnload Full Options Futures and Other Derivatives 8th Edition Hull Test Bank PDFDocument35 pagesDwnload Full Options Futures and Other Derivatives 8th Edition Hull Test Bank PDFwhalemanfrauleinshlwvz100% (10)

- Econ 101 (8X) Lecture #4 September 2021Document33 pagesEcon 101 (8X) Lecture #4 September 2021vinod srivasNo ratings yet

- Session 9Document16 pagesSession 9spamxacc7No ratings yet

- Problem Supply Demand and PoliciesDocument2 pagesProblem Supply Demand and PoliciesTonny NguyenNo ratings yet

- Economics Project YsDocument21 pagesEconomics Project YsYashasvi SharmaNo ratings yet

- Introduction To Demand Analysis & ForecastingDocument17 pagesIntroduction To Demand Analysis & ForecastingAdil Bin KhalidNo ratings yet

- Econ 1210 ElasticityDocument81 pagesEcon 1210 ElasticityCM LeungNo ratings yet

- ECON 1210 Cost and Profit Maximization Under CompetitonDocument53 pagesECON 1210 Cost and Profit Maximization Under CompetitonCM LeungNo ratings yet

- Business, Accounting and Financial Studies Mock Examination Paper 1Document24 pagesBusiness, Accounting and Financial Studies Mock Examination Paper 1CM LeungNo ratings yet

- Econ 1210 Compartive Statics of Market EquilibriumDocument69 pagesEcon 1210 Compartive Statics of Market EquilibriumCM LeungNo ratings yet

- Dogecoin Has Its Day, As Cryptocurrency Fans Push It Up: AdvertisementDocument3 pagesDogecoin Has Its Day, As Cryptocurrency Fans Push It Up: AdvertisementJoloNo ratings yet

- Customer PerceptionDocument9 pagesCustomer Perceptionnavdeep2309No ratings yet

- Presentation On Amul Case StudyDocument17 pagesPresentation On Amul Case StudyEshita ChakrabartyNo ratings yet

- Advertising in SocietyDocument22 pagesAdvertising in SocietyDushyant MudgalNo ratings yet

- PepsiCo Decision Criteria & Altenative SolutionDocument3 pagesPepsiCo Decision Criteria & Altenative Solutionk100% (1)

- Marriott SolutionDocument3 pagesMarriott Solutiondlealsmes100% (1)

- F9 - FM - Financial Management: NotesDocument76 pagesF9 - FM - Financial Management: NotesAshfaq Ul Haq OniNo ratings yet

- IbmDocument59 pagesIbmDarren_Fung_8729No ratings yet

- Break-Even Analysis Week 5Document12 pagesBreak-Even Analysis Week 5Melanie Cruz ConventoNo ratings yet

- (VAT) in To: Clarifying (RR) No. The The Tax of (TaxDocument13 pages(VAT) in To: Clarifying (RR) No. The The Tax of (TaxShiela Marie Maraon100% (1)

- Intermediate-Accounting Handout Chap 14Document3 pagesIntermediate-Accounting Handout Chap 14Joanne Rheena BooNo ratings yet

- Duration of BondDocument9 pagesDuration of BondUbaid DarNo ratings yet

- Bodie Investments 12e IM CH13Document3 pagesBodie Investments 12e IM CH13lexon_kbNo ratings yet

- International Business Dynamics: Case Study-1Document4 pagesInternational Business Dynamics: Case Study-1Santosh ArakeriNo ratings yet

- Stock Valuation MethodsDocument5 pagesStock Valuation MethodsgoodthoughtsNo ratings yet

- Purchasing and Supply Chain Management 3rd Edition Benton Test BankDocument26 pagesPurchasing and Supply Chain Management 3rd Edition Benton Test BankGaryDavisfdzb100% (49)

- Chap 2 Solutions PDFDocument19 pagesChap 2 Solutions PDFanon_461458122No ratings yet

- 06.money Market and Bond MarketDocument20 pages06.money Market and Bond MarketYogun BayonaNo ratings yet

- Marketing 91Document6 pagesMarketing 91Deepak Kalonia JangraNo ratings yet

- 20-30 MCQDocument3 pages20-30 MCQlorrynorry100% (1)

- Grish MaDocument2 pagesGrish MaAbhishek AgarwalNo ratings yet

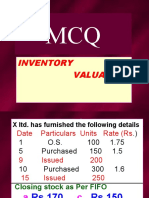

- MCQ Inventory Valuation LBSIMDocument49 pagesMCQ Inventory Valuation LBSIMSumit SharmaNo ratings yet

- Branding HS TalksDocument17 pagesBranding HS TalksumairNo ratings yet

- Your Adv Safebalance Banking: Account SummaryDocument10 pagesYour Adv Safebalance Banking: Account SummaryLaura Del valleNo ratings yet

- The Impact of Social Media Advertisement To The Preference of The Philippine CollageDocument4 pagesThe Impact of Social Media Advertisement To The Preference of The Philippine CollageSabrinna Andrea TanginanNo ratings yet

- Hindustan Petroleum Corporation LTDDocument7 pagesHindustan Petroleum Corporation LTDSaurabh Sharma100% (1)

- SCRADocument33 pagesSCRAAnmol KhuranaNo ratings yet

- DCF Valuation Financial ModelingDocument10 pagesDCF Valuation Financial ModelingHilal MilmoNo ratings yet