You might also like

- Tax Formula and Tax Determination An Overview of Property TransactionsDocument23 pagesTax Formula and Tax Determination An Overview of Property TransactionsJames Riley Case100% (1)

- CPA Exam REG Area 04 - Individual TaxationDocument3 pagesCPA Exam REG Area 04 - Individual TaxationManny MarroquinNo ratings yet

- Deduction From Gross Income-Deduction Allowed Under Special LawDocument131 pagesDeduction From Gross Income-Deduction Allowed Under Special LawRance Harry Daza0% (2)

- Iphone 6s InvoiceDocument2 pagesIphone 6s InvoiceNouman SheikhNo ratings yet

- American Depository ReceiptDocument11 pagesAmerican Depository ReceiptUrvish Tushar DalalNo ratings yet

- CPAR Deductions (Batch 89) HandoutDocument26 pagesCPAR Deductions (Batch 89) HandoutlllllNo ratings yet

- TAX Allowable Deductions-1Document35 pagesTAX Allowable Deductions-1lyza nedtranNo ratings yet

- Labor Law Case Digests Hernando Bar 2023Document174 pagesLabor Law Case Digests Hernando Bar 2023Sealtiel VillarealNo ratings yet

- CH 2Document71 pagesCH 2Adilene AcostaNo ratings yet

- Notes:: Deduction Individuals Estates Trusts Corp. PartnershipsDocument19 pagesNotes:: Deduction Individuals Estates Trusts Corp. PartnershipsDamdam AlunanNo ratings yet

- TAX-01 Chapter 12 - DeductionsDocument29 pagesTAX-01 Chapter 12 - DeductionsJovince Daño DoceNo ratings yet

- DeductionsDocument29 pagesDeductionsJohnallenson DacosinNo ratings yet

- CPAR Deductions (Batch 92) - HandoutDocument30 pagesCPAR Deductions (Batch 92) - HandoutaudreyNo ratings yet

- Capital Gains Tax: © AccaDocument29 pagesCapital Gains Tax: © AccaRai Ali WafaNo ratings yet

- HA3042 Revision Slides T2 2019 PDFDocument21 pagesHA3042 Revision Slides T2 2019 PDFSahil Aryal Golay VaiNo ratings yet

- Logue Taxation of Individual Income OutlineDocument41 pagesLogue Taxation of Individual Income OutlinearthrodNo ratings yet

- Unit 3 Spec Incl & Exempt IncomeDocument5 pagesUnit 3 Spec Incl & Exempt Incometetelomakgata1No ratings yet

- Sanni Patel Tax AssignmentDocument2 pagesSanni Patel Tax AssignmentbhramaniNo ratings yet

- Benefits Amounting To Php90,000: Taxable Income: Individuals Earning Purely Compensation IncomeDocument10 pagesBenefits Amounting To Php90,000: Taxable Income: Individuals Earning Purely Compensation IncomejenicaNo ratings yet

- AUSTRALIAN TAXATION - Parteng ApatDocument1 pageAUSTRALIAN TAXATION - Parteng ApatVero EntertainmentNo ratings yet

- Lesson 2Document12 pagesLesson 2devravidhan382No ratings yet

- REG-02 F8fe2e8Document52 pagesREG-02 F8fe2e8Vidyadhar TRNo ratings yet

- Corporation Tax - AnnotatedDocument64 pagesCorporation Tax - AnnotatedDr SafaNo ratings yet

- Annual Assumptions Scenario #1 Scenario #2Document8 pagesAnnual Assumptions Scenario #1 Scenario #2codaNo ratings yet

- SCorp 26062022Document27 pagesSCorp 26062022Jagmohan TeamentigrityNo ratings yet

- Direct Tax NotesDocument41 pagesDirect Tax NotesRenandNo ratings yet

- Deductions From Gross IncomeDocument5 pagesDeductions From Gross IncomeShena Gladdys BaylonNo ratings yet

- Taxation 1 - Lecture 1Document5 pagesTaxation 1 - Lecture 1Justin PandherNo ratings yet

- Lecture 26 - 27Document24 pagesLecture 26 - 27Pankaj MahantaNo ratings yet

- Capital Gains Tax Computation: Exempt AssetsDocument15 pagesCapital Gains Tax Computation: Exempt AssetsGayathri SudheerNo ratings yet

- ACCA - Skill Level Paper - F6 (UK) Income Tax ComputationDocument15 pagesACCA - Skill Level Paper - F6 (UK) Income Tax ComputationAnas KhalilNo ratings yet

- Chapter 5 Part 2Document26 pagesChapter 5 Part 2ISLAM KHALED ZSCNo ratings yet

- Dividend: Mr. Atulabhiman AgalaweDocument10 pagesDividend: Mr. Atulabhiman Agalaweatul AgalaweNo ratings yet

- I. Household Sector As An Institutional Sector in NationalDocument11 pagesI. Household Sector As An Institutional Sector in NationalJaqueline PadillaNo ratings yet

- TAX 228 2023 - Special InclusionsDocument29 pagesTAX 228 2023 - Special InclusionsedwardsyaameenNo ratings yet

- TOPIC 4 - Fringe Benefits TaxDocument27 pagesTOPIC 4 - Fringe Benefits TaxAkshita MehtaNo ratings yet

- Kinds of DeductionsDocument3 pagesKinds of DeductionsMeghan Kaye LiwenNo ratings yet

- Tax Financial Planning GuideDocument40 pagesTax Financial Planning Guideditoendutojkt75No ratings yet

- TaxpayerDocument70 pagesTaxpayerAlbert Alcantara BernardoNo ratings yet

- Series Six Workbook PDFDocument156 pagesSeries Six Workbook PDFDafnes ZGNo ratings yet

- Week 1 - Lecture NotesDocument12 pagesWeek 1 - Lecture NotesAbir DullooNo ratings yet

- Rent Income: Dividend Income Other IncomeDocument1 pageRent Income: Dividend Income Other IncomeLhorene Hope DueñasNo ratings yet

- Lecture Slides - Special Inclusions - Module 4 - 2023Document40 pagesLecture Slides - Special Inclusions - Module 4 - 2023sknatey221No ratings yet

- Sfe Cyi Form 2324 oDocument5 pagesSfe Cyi Form 2324 ody9bdbmjwsNo ratings yet

- REVISIONDocument4 pagesREVISIONTâm TốngNo ratings yet

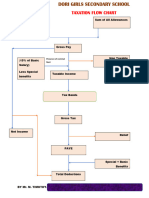

- Taxation Flow ChartDocument3 pagesTaxation Flow Chartpriscandegwa.pnNo ratings yet

- Chapter 5: Corporate Tax Learning ObjectivesDocument19 pagesChapter 5: Corporate Tax Learning ObjectivesLogaa UthyasuriyanNo ratings yet

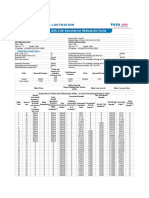

- Mahalife GoldDocument5 pagesMahalife GoldFiniscope - Investment AdvisorsNo ratings yet

- Form 91: Income CalculationsDocument7 pagesForm 91: Income CalculationsTroy StrawnNo ratings yet

- PFMDocument42 pagesPFMRavi PandeyNo ratings yet

- Module 35 Taxes: Partnerships:: 'S CC G C C Se e I 7 .E., o Co - Es Y. S CDocument2 pagesModule 35 Taxes: Partnerships:: 'S CC G C C Se e I 7 .E., o Co - Es Y. S CEl Sayed AbdelgawwadNo ratings yet

- Note 1-Estate Under AdministrationDocument8 pagesNote 1-Estate Under AdministrationNur Dina AbsbNo ratings yet

- TAX - Gross Income (Compensation)Document12 pagesTAX - Gross Income (Compensation)Von Andrei MedinaNo ratings yet

- Taxation - Quick Notes - FinalsDocument17 pagesTaxation - Quick Notes - FinalsRoseanneNo ratings yet

- Taxation HandoutDocument9 pagesTaxation HandoutTricia mae DingsitNo ratings yet

- Life Insurance Needs Analysis: Protec Tion SolutionsDocument3 pagesLife Insurance Needs Analysis: Protec Tion SolutionsDebdeep KarNo ratings yet

- Income Tax Law and It's Computation Sandeep KumarDocument33 pagesIncome Tax Law and It's Computation Sandeep KumarThe PaletteNo ratings yet

- FSA Course Pack Before Mid Balance Sheet PDFDocument16 pagesFSA Course Pack Before Mid Balance Sheet PDFRehman RajpootNo ratings yet

- Taxation - F6 Fa 2020 Volume Ii (4706)Document75 pagesTaxation - F6 Fa 2020 Volume Ii (4706)Jemila ChowrimotooNo ratings yet

- 5.2 Taxation: Igcse /O Level EconomicsDocument10 pages5.2 Taxation: Igcse /O Level Economicsdenny_sitorusNo ratings yet

- IFITC Chapter - 4 - 2019Document38 pagesIFITC Chapter - 4 - 2019Kirill KucherenkoNo ratings yet

- S 8 Allowances 2022Document11 pagesS 8 Allowances 2022v8ysqzd9pbNo ratings yet

- The Creed of Shia From Their Own SourcesDocument10 pagesThe Creed of Shia From Their Own SourcesuddintajNo ratings yet

- Prior Terms AUTHForm La DeltaDocument1 pagePrior Terms AUTHForm La Deltapaulsniff6No ratings yet

- EthicsDocument34 pagesEthicsIvan GustoNo ratings yet

- Corporate Meetings-16-61 PDFDocument46 pagesCorporate Meetings-16-61 PDFanon_16598294No ratings yet

- Global Medical Systems #27, Model House II Street, Basavanagudi, Bengaluru - 560004 2661 7623, 2661 1679 9 4404979Document2 pagesGlobal Medical Systems #27, Model House II Street, Basavanagudi, Bengaluru - 560004 2661 7623, 2661 1679 9 4404979Archesh DeepNo ratings yet

- ALFONSO TUASON Y ANGELES and MARIANO TUASON Y ANGELES Vs Juan PosadasDocument3 pagesALFONSO TUASON Y ANGELES and MARIANO TUASON Y ANGELES Vs Juan PosadasJessie BarredaNo ratings yet

- Synthesis Paper Revision 1Document7 pagesSynthesis Paper Revision 1api-564597486No ratings yet

- Class 12 ProjectsDocument21 pagesClass 12 ProjectsBEAST GAMINGNo ratings yet

- Analyzing Moral Issues 7th Edition Boss Solutions ManualDocument10 pagesAnalyzing Moral Issues 7th Edition Boss Solutions ManualAliciaMcintoshaeiop100% (9)

- Perilaku Birokrasi Dalam Pemberian Pelayanan PublikDocument14 pagesPerilaku Birokrasi Dalam Pemberian Pelayanan Publikadelia dwi yantiNo ratings yet

- The Other Afghan Women The New YorkerDocument43 pagesThe Other Afghan Women The New YorkerJulie ChanNo ratings yet

- Comparison of The HO-3 and The DP-3 FormsDocument2 pagesComparison of The HO-3 and The DP-3 FormsKarly AlleyneNo ratings yet

- Part 3: Practice: DAY 17 Toeic Thầy LongDocument36 pagesPart 3: Practice: DAY 17 Toeic Thầy LongQuỳnh AnhNo ratings yet

- FIN111 Tutorial 4QDocument2 pagesFIN111 Tutorial 4QKai YinNo ratings yet

- Direct Soft 6Document276 pagesDirect Soft 6nestor gonzalez de leonNo ratings yet

- BAM Corp Persentation 01012019Document27 pagesBAM Corp Persentation 01012019Walid El AmineNo ratings yet

- Request For TOR UPVDocument1 pageRequest For TOR UPVgongsilogNo ratings yet

- Formula Sheet Physics 12Document2 pagesFormula Sheet Physics 12RyanVgames MCNo ratings yet

- Booking Report July 5, 2020Document2 pagesBooking Report July 5, 2020WCTV Digital Team67% (3)

- Case Law: Spec Pro Midterms Reviewer (Atty. Chua)Document8 pagesCase Law: Spec Pro Midterms Reviewer (Atty. Chua)kathNo ratings yet

- E Janaza Namaz: (View Details)Document2 pagesE Janaza Namaz: (View Details)raotalhaNo ratings yet

- CV Rafi Cargill, GAR, MCR, AM GROUP and Consultancy EraDocument6 pagesCV Rafi Cargill, GAR, MCR, AM GROUP and Consultancy EranorulainkNo ratings yet

- August TIF Ch12Document19 pagesAugust TIF Ch12Ömer DoganNo ratings yet

- Preface:: Picaresque AdventureDocument18 pagesPreface:: Picaresque AdventureM Tauqeer Ahmed100% (1)

- Archmodels v004 PDFDocument6 pagesArchmodels v004 PDFGabriela López TelloNo ratings yet

- Contract of Employment Form This Agreement Is Made BetweenDocument4 pagesContract of Employment Form This Agreement Is Made BetweenTecla KannonNo ratings yet

- March 2017 PALEDocument23 pagesMarch 2017 PALEBfp Basud Camarines NorteNo ratings yet