MINISTRY OF FINANCE AND ECONOMIC DEVELOPMENT-MOFED

Training on Fixed Assets and Stock Management

�Government Owned Fixed Assets Management GOFAM By Teshome Teklehaimanot

�DAY ONE

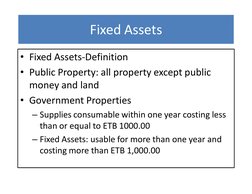

�Fixed Assets

Fixed Assets-Definition Public Property: all property except public money and land Government Properties

Supplies consumable within one year costing less than or equal to ETB 1000.00 Fixed Assets: usable for more than one year and costing more than ETB 1,000.00

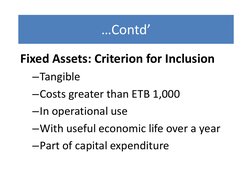

�Contd

Fixed Assets: Criterion for Inclusion

Tangible Costs greater than ETB 1,000 In operational use With useful economic life over a year Part of capital expenditure

�Fixed Assets Depreciation and RV

Depreciation Nominal value Residual value Book Value: Cost-Accumulated Depreciation

�Depreciation

Cost expiration

Wear and tear Obsolescence, inadequacy

Useful Life

Expected period of use Expected Production Capacity

Residual Value Depreciable Amount

�Contd

Cost: all amounts paid to acquire and place the assets and ready it for service.

Locally Purchased Foreign Purchases Constructed assets Donated assets Confiscated assets Acquired through other means

�COA

Codes for Detailed coding of Assets are from 4100 through 4999 (Ethiopian Government Financial Manual) Fixed Assets

4500-4519 construction in process 4520-4599 are reserved for property and equipment

�??? Big Point: Fixed Assets Should be expensed for Budget and reporting purpose Fixed Assets should be capitalized but not transferred to GL

�Categorization of Property and Equipment

Vehicle and Other Vehicular Transport Air Craft and Boats Plant and Machinery Military Equipment Building-Residential Building-Non Residential Infrastructure Military Purpose Buildings Furnisher and Fixtures

�CIP Assets

CIP-Building Residential CIP-Building Non Residential CIP-Infrastructure CIP-Military Purpose Building

�Major Maintenance

Shall be considered as capital expenditure

Life extension Capacity enhancement

Beware of overvaluation

�Management Structure

Fixed Asset Management Cycle Birth to Death of an asset

Receipt to Stores Issues Transfers Back to Stores Retirement

�Stores Management

Each Public Body needs to setup a used FA stores for items returned from users

�Government Procurement and Property Administration Agency (GPPAA)

Issue directives for GOFAM Collects information of FA In each government body there is a FAMU, fixed asset management unit

ICC: Initial Comprehensive Count Regular management season

�Valuation

Cost Determination

Valuation during initial comprehensive count Valuation during final disposal

�Initial Comprehensive Count (ICC)

The FAMU should establish the Government Owned Fixed Assets Data as an input. ICC Activities

Before Count During count After Count

�Maintenance of Fixed Assets

FAMU is responsible for protecting and maintaining the fixed assets

�Filing System for the UC and FAR

�Fixed Asset Records

Receipts of Fixed Assets to Stores

Model 19

Fixed Assets in Stores Fixed Assets under Construction Fixed Asset Information Tracked

Type Location etc

�Assigning PIN and Marking of FA in Use

Property Identification Number: PIN

Unique identifier given consecutively Numeric, alphabetic, or alpha-numeric

Marking and labeling

�Annual Physical Data (APC)

Annual Physical Count is a legal requirement Annual Summary Schedule for end of year reporting

�Valuation of Fixed Assets

Valuation: Determining the cost or value of an asset in use Actual cost or Determined in accordance with the directives from MOFED (if actual cost is not determinable)

�Changes to the Register

Newly Received assets to store: Model 19 Fixed Assets Requested and Issued: new Form

�Accounting Treatment of FA

Accounting Basis

Cash Basis Accounting Modified Basis of Accounting ***??? Accrual Basis of Accounting

Transitional arrangement is introduced in the FGE Accounting and Reporting Accounting for Other Assets and Liabilities

�Contd

Entries in the Memorandum (Fixed Asset Books)

Recording cost of fixed assets Recording values of fixed assets returned to stores Recording depreciation Accumulating and recording costs of CIP