You might also like

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Nonp 1 SlidesDocument20 pagesNonp 1 SlidesomponyeprimoganeditseNo ratings yet

- Solutions To Text Book Exercises: Non-Trading ConcernsDocument12 pagesSolutions To Text Book Exercises: Non-Trading ConcernsM JEEVARATHNAM NAIDUNo ratings yet

- Non-Profit Organisations AccountsDocument2 pagesNon-Profit Organisations AccountsMasood Ahmad AadamNo ratings yet

- Accountancy For Non Profit OrgDocument2 pagesAccountancy For Non Profit OrgNazneen Mohammad SabirNo ratings yet

- Accountancy Notes Not For Profit Organisation Problems and SolutionsDocument7 pagesAccountancy Notes Not For Profit Organisation Problems and SolutionsGod乡 DekuNo ratings yet

- Accounting For Not-For-Profit Organisation: G.Vijaya Kumar 9866003883Document36 pagesAccounting For Not-For-Profit Organisation: G.Vijaya Kumar 9866003883Yashwant RaoNo ratings yet

- Accounting For Not For Profit OrganizationsDocument13 pagesAccounting For Not For Profit Organizationswambui gatogoNo ratings yet

- Accounting For Non-Profit Organisation - With SolutionsDocument58 pagesAccounting For Non-Profit Organisation - With SolutionsShivi CholaNo ratings yet

- AFH Important QuestionDocument6 pagesAFH Important Questionmanassadashiv013No ratings yet

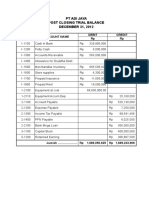

- Jawaban Silus Adijaya 2015Document15 pagesJawaban Silus Adijaya 2015natsu dragnelNo ratings yet

- ST ST STDocument1 pageST ST STAMIN BUHARI ABDUL KHADERNo ratings yet

- Journal Entries (Llandino)Document12 pagesJournal Entries (Llandino)Joy Danielle LlandinoNo ratings yet

- Lesson 2 Statement of Comprehensive IncomeDocument16 pagesLesson 2 Statement of Comprehensive Incomelorraine barrogaNo ratings yet

- Cash Flow QuestionsDocument6 pagesCash Flow QuestionsBhakti GhodkeNo ratings yet

- Tutorial 8 Accounting For Non-Profit Organization-20180522105531Document3 pagesTutorial 8 Accounting For Non-Profit Organization-20180522105531SHARONNo ratings yet

- QuestionDocument5 pagesQuestionakhileshmoney143No ratings yet

- BM Group Work AccountsDocument6 pagesBM Group Work AccountsprimroseNo ratings yet

- Accounting For Non-Profit OrganizationDocument30 pagesAccounting For Non-Profit OrganizationMeshayu RenaNo ratings yet

- FFA Lec 10 UpdatedDocument14 pagesFFA Lec 10 UpdatedBalochNo ratings yet

- Question BankDocument31 pagesQuestion BankmahendrabpatelNo ratings yet

- Proforma of Trading ADocument11 pagesProforma of Trading ASneha AgrawalNo ratings yet

- Presentation2Document9 pagesPresentation2shuklabharat2004No ratings yet

- PERSIJADocument10 pagesPERSIJAricoananta10No ratings yet

- Part - A Unit - 1 Accounting For - Not For Profit Organisations 1 Mark QuestionsDocument5 pagesPart - A Unit - 1 Accounting For - Not For Profit Organisations 1 Mark QuestionsDURAIMURUGAN MIS 17-18 MYP ACCOUNTS STAFFNo ratings yet

- Taxation NotesDocument33 pagesTaxation NotesNaina AgarwalNo ratings yet

- Basic Final AccountQuestions Part 2Document6 pagesBasic Final AccountQuestions Part 2Jahanzaib ButtNo ratings yet

- Week 4 FA Lecture BBDocument24 pagesWeek 4 FA Lecture BBkk23212No ratings yet

- Chapter 5 Exercise 8Document32 pagesChapter 5 Exercise 8Lady Zyanien DevarasNo ratings yet

- Accounting For Non-Profit OrganisationDocument29 pagesAccounting For Non-Profit OrganisationPKC GodNo ratings yet

- Lembar Jawab Laporan KeuanganDocument10 pagesLembar Jawab Laporan Keuanganricoananta10No ratings yet

- Cash FlowDocument2 pagesCash FlowXeher OpNo ratings yet

- Junior Philippine Institute of AccountantsDocument3 pagesJunior Philippine Institute of AccountantsFrancis TumamaoNo ratings yet

- Class Xii 2020-21 (Accountancy) Assignment 1 (Not For Profit Organisation)Document4 pagesClass Xii 2020-21 (Accountancy) Assignment 1 (Not For Profit Organisation)P Janaki RamanNo ratings yet

- Not For Profit Organisations: AccountancyDocument79 pagesNot For Profit Organisations: AccountancySoumendra RoyNo ratings yet

- Exercise 6Document4 pagesExercise 6dumpanonymouslyNo ratings yet

- Club Prepare The Income and Expenditure For The Year Ended 31-3-2016Document3 pagesClub Prepare The Income and Expenditure For The Year Ended 31-3-2016M JEEVARATHNAM NAIDUNo ratings yet

- Chapter 1-Company Accounts Financial Statements of Not-for-Profit OrganisationsDocument56 pagesChapter 1-Company Accounts Financial Statements of Not-for-Profit OrganisationsSachin DevNo ratings yet

- Assignment 1Document6 pagesAssignment 1Nichole TumulakNo ratings yet

- Bank Reconciliation - SolutionsDocument6 pagesBank Reconciliation - SolutionsNIAZ HUSSAINNo ratings yet

- Question Sheet - Non Profit OrganisationDocument7 pagesQuestion Sheet - Non Profit OrganisationShivangi JhawarNo ratings yet

- FAR 2 SledgerDocument6 pagesFAR 2 Sledgerkrystallanedenice.manansalaNo ratings yet

- P&LDocument3 pagesP&LPrincessNo ratings yet

- Unit - 5 Accounting For Non-Trading ConcernsDocument12 pagesUnit - 5 Accounting For Non-Trading ConcernsD20BRM036 SukantNo ratings yet

- Income and Expenditure AccountDocument7 pagesIncome and Expenditure AccountCM_NguyenNo ratings yet

- Non Profit OrganisationDocument5 pagesNon Profit Organisation27h4fbvsy8No ratings yet

- Additional Information:: Particulars Rs Particulars RsDocument3 pagesAdditional Information:: Particulars Rs Particulars RsBHAVIK RATHODNo ratings yet

- Revision Questions - 2 Statement of Cash Flows - SolutionDocument7 pagesRevision Questions - 2 Statement of Cash Flows - SolutionNadjah JNo ratings yet

- Financial Accounting 2015 B Com Part 1 PDocument5 pagesFinancial Accounting 2015 B Com Part 1 PPraver MalhotraNo ratings yet

- Npo CompiledDocument17 pagesNpo Compiledaneupane465No ratings yet

- DR ( ) CR ( ) : Gordon Blair CaféDocument2 pagesDR ( ) CR ( ) : Gordon Blair CaféSam SamNo ratings yet

- Non Trading OrganisationDocument70 pagesNon Trading OrganisationDivyansh TripathiNo ratings yet

- RequiredDocument15 pagesRequiredCheska Anne Mikka RoxasNo ratings yet

- Financial Assumptions: RevenueDocument12 pagesFinancial Assumptions: RevenueKathleeneNo ratings yet

- MQP - MBA - Sem1 - Financial and Management Accounting (DMBA104)Document5 pagesMQP - MBA - Sem1 - Financial and Management Accounting (DMBA104)Rohit SoodNo ratings yet

- Basic Final Accountquestions Part 2Document3 pagesBasic Final Accountquestions Part 2Jahanzaib ButtNo ratings yet

- Fa2 AssingmentDocument6 pagesFa2 Assingmentalia humairahNo ratings yet

- CSEC Principles of AccountsDocument6 pagesCSEC Principles of AccountsNatalie0% (1)

- AFO+ +Mock+TestDocument12 pagesAFO+ +Mock+TestArrow NagNo ratings yet

- JANUARI 2015: PT Maju Sarana Sport Cash Receipt JournalDocument39 pagesJANUARI 2015: PT Maju Sarana Sport Cash Receipt JournalAsna AzyyatiNo ratings yet

- Women and Child Welfare Policy Slogan.Document1 pageWomen and Child Welfare Policy Slogan.BARGAVI SNo ratings yet

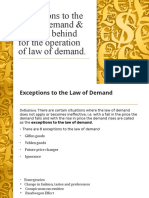

- Exceptions To The Law of DemandDocument5 pagesExceptions To The Law of DemandBARGAVI SNo ratings yet

- Using Law Library (Legal Methods)Document7 pagesUsing Law Library (Legal Methods)BARGAVI SNo ratings yet

- CourtsDocument11 pagesCourtsBARGAVI SNo ratings yet

- Types of CompaniesDocument8 pagesTypes of CompaniesBARGAVI SNo ratings yet

- Example Open Items Via Direct InputDocument8 pagesExample Open Items Via Direct InputSri RamNo ratings yet

- Banking Law - Law Relating To Dishonour of Cheques in India: An Analysis of Section 138 of The Negotiable Instruments ActDocument37 pagesBanking Law - Law Relating To Dishonour of Cheques in India: An Analysis of Section 138 of The Negotiable Instruments ActKashyap Kumar NaikNo ratings yet

- Transaction AcknowledgmentDocument9 pagesTransaction Acknowledgmentgirish geethuNo ratings yet

- Chapter 14 Audit of Cash and Bank BalancesDocument14 pagesChapter 14 Audit of Cash and Bank BalancesChristian LimNo ratings yet

- Cash Flow-Case StudyDocument37 pagesCash Flow-Case StudyNguyen Minh DucNo ratings yet

- Signing Date: 13/12/2023 04:13:18 SGT Signed By: Ds CWT India PVT LTD 2Document3 pagesSigning Date: 13/12/2023 04:13:18 SGT Signed By: Ds CWT India PVT LTD 2Himanshu MishraNo ratings yet

- CMTF-i 1st P ChargeDocument36 pagesCMTF-i 1st P ChargeAlyssia LohNo ratings yet

- R12 FinancialsDocument60 pagesR12 Financialsmukesh697No ratings yet

- Dewata Raya Ep 3Document2 pagesDewata Raya Ep 3Betta UcupNo ratings yet

- Financial & Managerial Accounting: Information For DecisionsDocument120 pagesFinancial & Managerial Accounting: Information For DecisionsmalihaNo ratings yet

- National Highways Authority of India Vs Punjab NatDE20211101211527433COM896528Document29 pagesNational Highways Authority of India Vs Punjab NatDE20211101211527433COM896528aridaman raghuvanshiNo ratings yet

- Blackbook Project On International Banking - 16340Document67 pagesBlackbook Project On International Banking - 16340Vinod ChaurasiyaNo ratings yet

- Tally 9.0 Multiple Choice QuestionsDocument15 pagesTally 9.0 Multiple Choice QuestionsShubham VermaNo ratings yet

- How Much Do You Owe? $103.70 Here's A Breakdown of Your TotalDocument4 pagesHow Much Do You Owe? $103.70 Here's A Breakdown of Your TotalSushilNo ratings yet

- John Dy Vs People of The Philippines and Hon. Court of Appeals G.R. No. 158312 November 14, 2008Document2 pagesJohn Dy Vs People of The Philippines and Hon. Court of Appeals G.R. No. 158312 November 14, 2008Dianne YcoNo ratings yet

- FEE PROPOSAL Student Permit MR Joss Alexander George CheltonDocument5 pagesFEE PROPOSAL Student Permit MR Joss Alexander George CheltonjosscheltonNo ratings yet

- Books of Prime EntryDocument14 pagesBooks of Prime EntryBareera WajidNo ratings yet

- Audit of Cash ActivityDocument13 pagesAudit of Cash ActivityIris FenelleNo ratings yet

- Vendor Agreement: of This Material Is ProhibitedDocument6 pagesVendor Agreement: of This Material Is ProhibitedAbdul AzeemNo ratings yet

- Handbook On DIGITAL Products 20210815125103Document29 pagesHandbook On DIGITAL Products 20210815125103Neos EonsNo ratings yet

- Insta Loan On Card TCDocument3 pagesInsta Loan On Card TCMANIKANDAN ANANTHARAJANNo ratings yet

- Fresh Cut Bank Draft Doa - 2022Document15 pagesFresh Cut Bank Draft Doa - 2022MANOJ VIJAYANNo ratings yet

- Phone Bill Jan 2022Document6 pagesPhone Bill Jan 2022Maxime VogneNo ratings yet

- New Balance $6,751.10 Payment Due Date 10/05/19: American Express Classic Gold CardDocument8 pagesNew Balance $6,751.10 Payment Due Date 10/05/19: American Express Classic Gold CardIrshad aliNo ratings yet

- Fee Protection Agreement - sampLEDocument3 pagesFee Protection Agreement - sampLEmario100% (4)

- Afterpay Research PDFDocument33 pagesAfterpay Research PDFNikhil JoyNo ratings yet

- Barclay - Secure Acceptance WMDocument121 pagesBarclay - Secure Acceptance WMAndra-Mihaela StateNo ratings yet

- Offering Letter Rakernas Federasi Karate Traditional IndonesiaDocument7 pagesOffering Letter Rakernas Federasi Karate Traditional Indonesiadicky gustiandiNo ratings yet

- Sonali BajajDocument90 pagesSonali Bajajranaindia2011100% (1)

- Deemed Conveyance CircularsDocument17 pagesDeemed Conveyance Circularssales leotekNo ratings yet