You might also like

- Heinz Case SolutionDocument4 pagesHeinz Case SolutionNischal Upreti0% (2)

- Proposal To Rent Kiosk in MallDocument6 pagesProposal To Rent Kiosk in MallYOUNEED TRADINGNo ratings yet

- 2018 06 25 - Bloomberg - Businessweek USA PDFDocument80 pages2018 06 25 - Bloomberg - Businessweek USA PDFPaco FernandezNo ratings yet

- MAG'Impact: The High-Performance Impactor: Cubicity and SimplicityDocument5 pagesMAG'Impact: The High-Performance Impactor: Cubicity and SimplicityPrekelNo ratings yet

- PDF Report Jakpat Brand Health Tracking Q1 of 2019 - Instant Noodle Free Version 19047Document15 pagesPDF Report Jakpat Brand Health Tracking Q1 of 2019 - Instant Noodle Free Version 19047J Septanti100% (1)

- Groww Stock Account Opening Form-1Document21 pagesGroww Stock Account Opening Form-1Karamsigh rawat 9277No ratings yet

- Group 18 Session 4 Assignment Kraft-Heinz MergerDocument6 pagesGroup 18 Session 4 Assignment Kraft-Heinz MergerAishwarya Yadav BJ20064No ratings yet

- Anyflip Com Btqyh EuddDocument4 pagesAnyflip Com Btqyh EuddMarusya BatataNo ratings yet

- Man Fleeing Drug Bust Dies When Undercover NYPD Cop Throws Cooler atDocument1 pageMan Fleeing Drug Bust Dies When Undercover NYPD Cop Throws Cooler atRamonita GarciaNo ratings yet

- Human Resources Strategy: Recruiting and Hiring Talented PeopleDocument2 pagesHuman Resources Strategy: Recruiting and Hiring Talented PeopleSimaSenNo ratings yet

- BA School091109Document1 pageBA School091109swim03No ratings yet

- Education: Project: Develop The Supply Chain Model For Adhesives (Incl. Stationary) and Wood Finishes CategoriesDocument1 pageEducation: Project: Develop The Supply Chain Model For Adhesives (Incl. Stationary) and Wood Finishes CategoriesVaibhav GuptaNo ratings yet

- 12 PSPO - APAC - MayDocument1 page12 PSPO - APAC - Maychellappan29No ratings yet

- Dividend Stocks Sharesmagazine AjbellDocument65 pagesDividend Stocks Sharesmagazine Ajbellmeditationinstitute.netNo ratings yet

- 2022 INTI ProgrammeGuide BrochureDocument8 pages2022 INTI ProgrammeGuide BrochureTakudzwa Dean MangenaNo ratings yet

- Employees As CustomersDocument1 pageEmployees As CustomersNoel Saji PaulNo ratings yet

- Healthcare Plus Policy: Icicilombard 1800 2666Document2 pagesHealthcare Plus Policy: Icicilombard 1800 2666Baby SivaNo ratings yet

- CPF Annual Report 2020Document22 pagesCPF Annual Report 2020AlioNo ratings yet

- 240 Retail Companies in Gurgaon - Gurugram - AmbitionBoxDocument6 pages240 Retail Companies in Gurgaon - Gurugram - AmbitionBoxblr.visheshNo ratings yet

- Sri Lankan Bank Account ComparisonDocument9 pagesSri Lankan Bank Account ComparisonThusitha DalpathaduNo ratings yet

- Star Outpatient Care Insurance Policy Brochure v.1 Ebook PDFDocument6 pagesStar Outpatient Care Insurance Policy Brochure v.1 Ebook PDFlalith mohanNo ratings yet

- Dr. M. Anil Ramesh's 3rd Article Published in Young Hans On 26-05-2014Document1 pageDr. M. Anil Ramesh's 3rd Article Published in Young Hans On 26-05-2014Anil RameshNo ratings yet

- InfraDocument1 pageInfraJamamamaNo ratings yet

- Denah LT 1Document1 pageDenah LT 1Stevanus RyanNo ratings yet

- Select Parameters: Pump Family SP, SP-G, Sp-Ne, Spe SPDocument1 pageSelect Parameters: Pump Family SP, SP-G, Sp-Ne, Spe SPlarryshuiNo ratings yet

- Star Super Surplus Floater BrochureDocument14 pagesStar Super Surplus Floater BrochureBeenu BhallaNo ratings yet

- Scape Report E Commerce 2023Document1 pageScape Report E Commerce 2023George MillardNo ratings yet

- Ninja Foodi Power Blender & Processor System, Smoothie Bowl Maker & Nutrient Extractor, 1400WP SmartTORQUE 6 Auto-iQ Silver SS3Document1 pageNinja Foodi Power Blender & Processor System, Smoothie Bowl Maker & Nutrient Extractor, 1400WP SmartTORQUE 6 Auto-iQ Silver SS3Dani FavoritoNo ratings yet

- Mindmap Continuous Learning InvolvationDocument1 pageMindmap Continuous Learning InvolvationEdison Reus SilveiraNo ratings yet

- Gayatri Enclave BrouchereDocument2 pagesGayatri Enclave BrouchereKoshekay Srinivas RaoNo ratings yet

- Summer Report ParveenDocument44 pagesSummer Report Parveenpaawansharma003No ratings yet

- New Book Reveals Who Is Really in Charge of The White HouseDocument1 pageNew Book Reveals Who Is Really in Charge of The White HouseRamonita GarciaNo ratings yet

- Online Resources For Science Laboratories (POD) - Remote TeachingDocument2 pagesOnline Resources For Science Laboratories (POD) - Remote TeachingBaiye RandolfNo ratings yet

- Principles of Microeconomics (Chapter 20)Document26 pagesPrinciples of Microeconomics (Chapter 20)Thanh-Phu TranNo ratings yet

- Buy Blue Jeans For Men by The Indian Garage Co OnlineDocument2 pagesBuy Blue Jeans For Men by The Indian Garage Co Onlineavinash_golechhaNo ratings yet

- SNI Application - Flow ChartDocument3 pagesSNI Application - Flow Chartaiman ismailNo ratings yet

- LOB of TUPAD BeneficiariesDocument1 pageLOB of TUPAD Beneficiariesandrea.babonNo ratings yet

- Sales Note Goodricke Group LTD 02072018 FinDocument10 pagesSales Note Goodricke Group LTD 02072018 FinNikhil KumarNo ratings yet

- Mangal May 21Document12 pagesMangal May 21Saurabh SinghNo ratings yet

- NYPD Exodus Continues As Cops Feel 'Squeezed From Every Direction'Document1 pageNYPD Exodus Continues As Cops Feel 'Squeezed From Every Direction'Ramonita GarciaNo ratings yet

- Ethical Audit Report - Harry Fashion Ltd-2020-07-09Document13 pagesEthical Audit Report - Harry Fashion Ltd-2020-07-09Abid HasanNo ratings yet

- 0228 County LineDocument8 pages0228 County LineMineral Wells Index/Weatherford DemocratNo ratings yet

- Apcotex Industries LTD Initiating Coverage 27042016 PDFDocument8 pagesApcotex Industries LTD Initiating Coverage 27042016 PDFbharat005No ratings yet

- Polamco Product Finder PDFDocument1 pagePolamco Product Finder PDFpaula09No ratings yet

- Balance Sheet Eng 05-06Document1 pageBalance Sheet Eng 05-06sashdreamNo ratings yet

- Merritt Morning Market 3352 - November 15Document2 pagesMerritt Morning Market 3352 - November 15Kim LeclairNo ratings yet

- Colombina - Marcia BriosaDocument1 pageColombina - Marcia BriosaDonatella MaisanoNo ratings yet

- Publication of Sale of Stressed Financial Assets - August 2022 EnglishDocument1 pagePublication of Sale of Stressed Financial Assets - August 2022 EnglishVILAS GAIKARNo ratings yet

- How To Create Group in Tally PrimeDocument3 pagesHow To Create Group in Tally PrimeAmit GuptaNo ratings yet

- Innovality Brochure Excellent-M Xb1046EDocument3 pagesInnovality Brochure Excellent-M Xb1046ERobert MontañezNo ratings yet

- Contoh Quotation Photoshoot 2023Document1 pageContoh Quotation Photoshoot 2023Fadhli IbrahimNo ratings yet

- Employment IncomeDocument29 pagesEmployment IncomeJalees Ul HassanNo ratings yet

- Rupeeseed Technology Venture PVT LTD: Current Month April To DateDocument1 pageRupeeseed Technology Venture PVT LTD: Current Month April To DateBablu GuptaNo ratings yet

- MY Melalife November 2019 - ENG - LowresDocument23 pagesMY Melalife November 2019 - ENG - LowreshoonNo ratings yet

- Summer Intership - Guna Singh J Glory PackageDocument29 pagesSummer Intership - Guna Singh J Glory PackageGuna 46 SinghNo ratings yet

- Chapter 5 Design of Goods and Services OpmDocument1 pageChapter 5 Design of Goods and Services Opmnurfarhana6789No ratings yet

- (10022765) Small MSP (DRG 004) - R10 - 10.01.2019Document1 page(10022765) Small MSP (DRG 004) - R10 - 10.01.2019yash prajapatiNo ratings yet

- Arketeer: NJ Media GroupDocument24 pagesArketeer: NJ Media GroupCoolerAdsNo ratings yet

- 0206 Chennai ClassifiedDocument4 pages0206 Chennai ClassifiedPrachi PrachiNo ratings yet

- D3-17. PLAN PROFIL UP CIBADAK 21+082.862-Layout1Document1 pageD3-17. PLAN PROFIL UP CIBADAK 21+082.862-Layout1arashNo ratings yet

- gnss-sp-26.790 - Model - PDF GenDocument1 pagegnss-sp-26.790 - Model - PDF GenviswanathNo ratings yet

- Creora Commitment To Excellence in Personal HygieneDocument5 pagesCreora Commitment To Excellence in Personal HygienePutri Indah PermatasariNo ratings yet

- Problem Solving 4 Today, Grade 3: Daily Skill PracticeFrom EverandProblem Solving 4 Today, Grade 3: Daily Skill PracticeNo ratings yet

- Prism RoboDocument11 pagesPrism Robodeepak mishraNo ratings yet

- Secom GroupDocument8 pagesSecom Groupdeepak mishra100% (1)

- Auto LoanDocument5 pagesAuto Loandeepak mishraNo ratings yet

- Banking LawDocument9 pagesBanking Lawdeepak mishraNo ratings yet

- T Bill - CP - CD Pricing & Secondary Market TransactionsDocument4 pagesT Bill - CP - CD Pricing & Secondary Market Transactionsdeepak mishraNo ratings yet

- Derivatives - AnnirudhDocument34 pagesDerivatives - Annirudhdeepak mishraNo ratings yet

- Project Digital Transformation of Financial ServicesDocument1 pageProject Digital Transformation of Financial Servicesdeepak mishraNo ratings yet

- Methodology Dow Jones Sustainability IndicesDocument38 pagesMethodology Dow Jones Sustainability IndicesBrianNo ratings yet

- Course Outline S1 2022Document5 pagesCourse Outline S1 2022Woon TNNo ratings yet

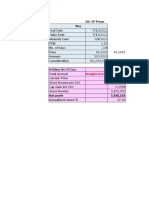

- Mutual Fund Portfolio Tracker Using MS ExcelDocument1,546 pagesMutual Fund Portfolio Tracker Using MS Excelrajanvaidya11100% (2)

- Q3 2023 PitchBook Analyst Note Introducing The Pre-Seed DatasetDocument14 pagesQ3 2023 PitchBook Analyst Note Introducing The Pre-Seed DatasetyurigitahyNo ratings yet

- Property Scout Introduction - Prospecting For ProfitsDocument12 pagesProperty Scout Introduction - Prospecting For ProfitsMichael Durden100% (1)

- Geeta Saar Vol 15Document6 pagesGeeta Saar Vol 15Advay SinghNo ratings yet

- ZICA Accountancy Programme Students HandbookDocument72 pagesZICA Accountancy Programme Students HandbookVainess S Zulu100% (1)

- Chapter 01 - Accounting in ActionDocument69 pagesChapter 01 - Accounting in ActionFatman RulesNo ratings yet

- Adnan Mirzoyev CVDocument2 pagesAdnan Mirzoyev CVZhanna AkopyanNo ratings yet

- The 5 Percent CanaryDocument26 pagesThe 5 Percent CanaryjpnietolsNo ratings yet

- Midterm SolveDocument3 pagesMidterm SolveMD Hafizul Islam HafizNo ratings yet

- Test Bank Chap 009Document19 pagesTest Bank Chap 009BẢO CHÂU GIANo ratings yet

- Mid-Term Examination: University of Economics and Law - Vietnam National University - HCMCDocument7 pagesMid-Term Examination: University of Economics and Law - Vietnam National University - HCMCNgân Võ Trần TuyếtNo ratings yet

- Black Scholes Model ReportDocument6 pagesBlack Scholes Model ReportminhalNo ratings yet

- BBA in Accounting 1Document7 pagesBBA in Accounting 1NomanNo ratings yet

- FinanceDocument3 pagesFinanceKarim El GazzarNo ratings yet

- Fama & French 2015 PDFDocument22 pagesFama & French 2015 PDFFlorencia ReginaNo ratings yet

- Trading SimulationDocument9 pagesTrading SimulationЭрдэнэ-Очир НОМИНNo ratings yet

- IFF International Flavors and Fragrances Sept 2013 Investor Slide Deck Powerpoint PDFDocument9 pagesIFF International Flavors and Fragrances Sept 2013 Investor Slide Deck Powerpoint PDFAla BasterNo ratings yet

- EF MT5 User Guide Android en Content TabletDocument47 pagesEF MT5 User Guide Android en Content TabletzooorNo ratings yet

- Practice Session Questions - Equity 05112022 031953pmDocument3 pagesPractice Session Questions - Equity 05112022 031953pmMeraj Ali100% (1)

- Business Combination and Consolidated FS Part 1Document6 pagesBusiness Combination and Consolidated FS Part 1markNo ratings yet

- AbsharDocument23 pagesAbsharAbsharNo ratings yet

- FD Question BankDocument5 pagesFD Question Bankruchi agrawalNo ratings yet

- INDICES of Mauritius Stock Exchange IndexesDocument10 pagesINDICES of Mauritius Stock Exchange IndexesAli ShahNo ratings yet

- Investing in Rare Coins With MCDocument14 pagesInvesting in Rare Coins With MCMonetariusCapitalNo ratings yet

- BUS20269 Financial Management Final ExamDocument7 pagesBUS20269 Financial Management Final Examshiyingyang98No ratings yet