You might also like

- Anz Pensioner Advantage Statement: Welcome To Your Anz Account at A GlanceDocument12 pagesAnz Pensioner Advantage Statement: Welcome To Your Anz Account at A GlanceMohitNo ratings yet

- Manufacturing Process Audit: Example ReportDocument25 pagesManufacturing Process Audit: Example ReportJawad rahmanaccaNo ratings yet

- Debt RestructureDocument10 pagesDebt RestructureBeryl VerzosaNo ratings yet

- Marginal costing concepts explainedDocument16 pagesMarginal costing concepts explainedFarrukhsg100% (2)

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Due DilligenceDocument26 pagesDue Dilligencedonny_khosla100% (1)

- 13.1 Objective 13.1: Chapter 13 Pricing Decisions and Cost ManagementDocument43 pages13.1 Objective 13.1: Chapter 13 Pricing Decisions and Cost ManagementAlanood WaelNo ratings yet

- Chapter 13 Quiz: The Following Data Apply To Questions 6 and 7Document41 pagesChapter 13 Quiz: The Following Data Apply To Questions 6 and 7Dellya PutriNo ratings yet

- Money Mastermind Vol 1 PDFDocument283 pagesMoney Mastermind Vol 1 PDFKatya SivkovaNo ratings yet

- Langfield-Smith7e IRM Ch20Document38 pagesLangfield-Smith7e IRM Ch20Sophia Duong100% (5)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- CVP Analysis & Decision MakingDocument67 pagesCVP Analysis & Decision MakingcmukherjeeNo ratings yet

- Target Costing Presentation FinalDocument57 pagesTarget Costing Presentation FinalMr Dampha100% (1)

- Pricing Decisions F5 NotesDocument4 pagesPricing Decisions F5 NotesSiddiqua KashifNo ratings yet

- Cost II CH 4Document6 pagesCost II CH 4Ebsa AdemeNo ratings yet

- Chapter Six Pricing Decisions: Major Influences On Pricing DecisionDocument6 pagesChapter Six Pricing Decisions: Major Influences On Pricing DecisionTESFAY GEBRECHERKOSNo ratings yet

- Introduction To PricingDocument11 pagesIntroduction To PricingMuhammad Hamza ZahidNo ratings yet

- Cost & Pricing StrategiesDocument5 pagesCost & Pricing StrategiesMoti BekeleNo ratings yet

- Pricing & Channels of DistributionDocument60 pagesPricing & Channels of Distributionsumeet kcNo ratings yet

- Chapter 5Document26 pagesChapter 5Hoàng Phương ThảoNo ratings yet

- Chap 5 - Pricing CalculationsDocument46 pagesChap 5 - Pricing CalculationsNguyễn Ngọc HàNo ratings yet

- Economic Analysis Policy - IDocument30 pagesEconomic Analysis Policy - IThaddeus De MenezesNo ratings yet

- Principles of Business Decisions - SEction IDocument4 pagesPrinciples of Business Decisions - SEction ISheethalNo ratings yet

- Activity Based CostingDocument2 pagesActivity Based CostingTesfish AssefaNo ratings yet

- Price Unit 2Document11 pagesPrice Unit 2MathiosNo ratings yet

- Chapter 6cost IIDocument5 pagesChapter 6cost IITammy 27No ratings yet

- AC 203 Principles of Accounting III Final Exam WorksheetDocument6 pagesAC 203 Principles of Accounting III Final Exam WorksheetLương Thế CườngNo ratings yet

- 7_Pricing Decisions.pptxDocument12 pages7_Pricing Decisions.pptxCharisse Ahnne TosloladoNo ratings yet

- Marginal Costing: Definition: (CIMA London)Document4 pagesMarginal Costing: Definition: (CIMA London)Pankaj2cNo ratings yet

- Chapter 7 - Pricing Decisions - Student VersionDocument35 pagesChapter 7 - Pricing Decisions - Student VersionPiece of WritingsNo ratings yet

- Chapter 3 Cost IDocument64 pagesChapter 3 Cost IBikila MalasaNo ratings yet

- 12 - Chapter15 PresentationDocument36 pages12 - Chapter15 Presentationsiwarr93No ratings yet

- Model Question Paper Cost and Management AccountingDocument6 pagesModel Question Paper Cost and Management AccountingSuhas BRNo ratings yet

- Nota Topik 2Document14 pagesNota Topik 2Nurul Ain Kisz'tinaNo ratings yet

- Strategic Cost Management - Semester SummaryDocument15 pagesStrategic Cost Management - Semester SummaryivandimaunahannnNo ratings yet

- ACCT 202 - Ch8-HandoutDocument63 pagesACCT 202 - Ch8-HandoutRenesmee SwanNo ratings yet

- "You Don't Sell Through Price. You Sell The Price" Price Is The Marketing-Mix Element That Produces Revenue The Others Produce CostDocument22 pages"You Don't Sell Through Price. You Sell The Price" Price Is The Marketing-Mix Element That Produces Revenue The Others Produce Cost200eduNo ratings yet

- Managerial Accounting Module 2 ActivityDocument7 pagesManagerial Accounting Module 2 ActivityDesy Joy UrotNo ratings yet

- Break Win AnalysisDocument14 pagesBreak Win Analysiskian obdinNo ratings yet

- Purpose of costing: value inventory, record costs, price products, make decisionsDocument13 pagesPurpose of costing: value inventory, record costs, price products, make decisionsSiddiqua KashifNo ratings yet

- Welcome: We Belong To "Group-6"Document26 pagesWelcome: We Belong To "Group-6"Rifat LimonNo ratings yet

- TLE ExploratoryCookery7 Q1M5Week6 OKDocument9 pagesTLE ExploratoryCookery7 Q1M5Week6 OKAmelita Benignos OsorioNo ratings yet

- Pricing DecisionsDocument34 pagesPricing Decisionszombies_meNo ratings yet

- Pricing and Short Term Decision Making (Edited)Document58 pagesPricing and Short Term Decision Making (Edited)Vaibhav SuchdevaNo ratings yet

- The Second P: PRICEDocument22 pagesThe Second P: PRICEJudy Ann PrincipeNo ratings yet

- Organizational Overview of Tasty (Pvt) LtdDocument43 pagesOrganizational Overview of Tasty (Pvt) LtdCalistus FernandoNo ratings yet

- 18 5 18 7 18 8 18 9 18 10Document11 pages18 5 18 7 18 8 18 9 18 10ReyhanNo ratings yet

- Pricing Products and Services: Per Unit TotalDocument3 pagesPricing Products and Services: Per Unit TotalSherwin Francis MendozaNo ratings yet

- Lec 4BDocument12 pagesLec 4Bjule160606No ratings yet

- PricingDocument35 pagesPricingSauban AhmedNo ratings yet

- Module 6: Internal Analysis of The Company 6.1. Opportunity CostDocument7 pagesModule 6: Internal Analysis of The Company 6.1. Opportunity CostSanjayNo ratings yet

- Marketing Management Price StrategyDocument30 pagesMarketing Management Price StrategyChali KumaraNo ratings yet

- Questions - CVP Analysis and Decision MakingDocument58 pagesQuestions - CVP Analysis and Decision Makinghukumsingh01juneNo ratings yet

- CH 08Document69 pagesCH 08Monica ReyesNo ratings yet

- Cost Analysis: 1) Opportunity Costs and Outlay CostsDocument8 pagesCost Analysis: 1) Opportunity Costs and Outlay Costsakash creationNo ratings yet

- Q2 SSLM2 Principles of Marketing LAgcaoiliDocument7 pagesQ2 SSLM2 Principles of Marketing LAgcaoiliDaniel Guanzon TanNo ratings yet

- University of Technical Education University of Sunderland: Ho Chi Minh City - 2009Document19 pagesUniversity of Technical Education University of Sunderland: Ho Chi Minh City - 2009Đặng Thanh ThảoNo ratings yet

- Marginal Costing FundamentalsDocument22 pagesMarginal Costing FundamentalsYatriShahNo ratings yet

- Cost and Management Accounting 6Pca7RQV4i8tDocument12 pagesCost and Management Accounting 6Pca7RQV4i8takhlaqur rahmanNo ratings yet

- Relevant Costing NotesDocument30 pagesRelevant Costing NotesJungkook100% (1)

- Econ SG Chap08Document20 pagesEcon SG Chap08CLNo ratings yet

- Handout 9-Pricing DecisionDocument4 pagesHandout 9-Pricing DecisionJoyciee BacaniNo ratings yet

- Handout 9-Pricing DecisionDocument4 pagesHandout 9-Pricing DecisionJoyciee BacaniNo ratings yet

- Pricing and Costing Reporting QuizshitDocument2 pagesPricing and Costing Reporting QuizshitJan Marc ConcioNo ratings yet

- Methos of PricingDocument18 pagesMethos of PricingKhelin ShahNo ratings yet

- Sesion 4Document19 pagesSesion 4PANDHARE SIDDHESHNo ratings yet

- Sesion 5Document19 pagesSesion 5PANDHARE SIDDHESHNo ratings yet

- Working Capital ManagementDocument19 pagesWorking Capital ManagementPANDHARE SIDDHESHNo ratings yet

- Sesion 7Document13 pagesSesion 7PANDHARE SIDDHESHNo ratings yet

- Sesion 6Document20 pagesSesion 6PANDHARE SIDDHESHNo ratings yet

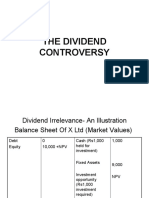

- The Dividend Controversy 1Document30 pagesThe Dividend Controversy 1AayushNo ratings yet

- Lease Financing1Document28 pagesLease Financing1PANDHARE SIDDHESHNo ratings yet

- Financial LeverageDocument49 pagesFinancial LeverageLavanya SinhaNo ratings yet

- Joint CostsDocument40 pagesJoint CostsPANDHARE SIDDHESHNo ratings yet

- The Capital Structure TheoriesDocument61 pagesThe Capital Structure TheoriesAayushNo ratings yet

- Strategic Tools for Mgt AccountantsDocument15 pagesStrategic Tools for Mgt AccountantsPANDHARE SIDDHESHNo ratings yet

- Mundell Fleming Open Economy ModelDocument19 pagesMundell Fleming Open Economy ModelPANDHARE SIDDHESHNo ratings yet

- Ch13. Flexible Budget-AkmDocument44 pagesCh13. Flexible Budget-AkmPANDHARE SIDDHESHNo ratings yet

- Business PlanDocument13 pagesBusiness PlanShilpaNo ratings yet

- Strategic Brand ManagementDocument4 pagesStrategic Brand Managementivan rickyNo ratings yet

- Ch09 TB RankinDocument6 pagesCh09 TB RankinAnton Vitali100% (1)

- Print - Udyam Registration Certificate1234Document3 pagesPrint - Udyam Registration Certificate1234Jaydipsinh SolankiNo ratings yet

- Oblicon 12 - Contracts CH 2 Notes PDFDocument7 pagesOblicon 12 - Contracts CH 2 Notes PDFJoy LuNo ratings yet

- TayalDocument8 pagesTayalAhsrah Htan AhjNo ratings yet

- MarriottDocument10 pagesMarriottimwkyaNo ratings yet

- Multifamily Express: Real Estate Capital MarketsDocument1 pageMultifamily Express: Real Estate Capital MarketsbobNo ratings yet

- 8 Common Business Plan Mistakes PDFDocument4 pages8 Common Business Plan Mistakes PDFNelPermatoNo ratings yet

- SBOM System for Genset Material InventoryDocument5 pagesSBOM System for Genset Material InventoryWahyu Utomo AjiNo ratings yet

- COSC 6301 - Computer Security - OverviewDocument48 pagesCOSC 6301 - Computer Security - OverviewmailtosiscoNo ratings yet

- Chapter 1aDocument33 pagesChapter 1aVasunNo ratings yet

- Export Overdues Export Overdues: Prepared By: Hina MukarramDocument24 pagesExport Overdues Export Overdues: Prepared By: Hina MukarramAnonymous NM8Ej4mONo ratings yet

- Application Form For Mudra Loan ShishuDocument2 pagesApplication Form For Mudra Loan ShishuSree DigitalNo ratings yet

- Safari - 03-Oct-2023 at 10:27 AMDocument1 pageSafari - 03-Oct-2023 at 10:27 AMVijay BhaskarNo ratings yet

- Week 5 - Performance Task 2Document2 pagesWeek 5 - Performance Task 2Eurika Nicole BeceosNo ratings yet

- Penentuan Pengungkapan Sustainability Report Dengan GRI Standar Pada Sektor Non-KeuanganDocument13 pagesPenentuan Pengungkapan Sustainability Report Dengan GRI Standar Pada Sektor Non-KeuanganAfifah FatinNo ratings yet

- Summary On StarbucksDocument3 pagesSummary On StarbucksSaleem BhattiNo ratings yet

- Tally ERP 9 Tutorial With ExamplesDocument3 pagesTally ERP 9 Tutorial With ExamplesAnurag KumarNo ratings yet

- Supreme Court Rules on Tax Treatment of Dividend Income for Life Insurance CompaniesDocument12 pagesSupreme Court Rules on Tax Treatment of Dividend Income for Life Insurance CompaniesCharles MagistradoNo ratings yet

- Unit - I - Over View of ManagementDocument17 pagesUnit - I - Over View of ManagementabavithraaNo ratings yet

- Auditing 2nd Sem AY 2020-2021 Institutional Mock Board ExamDocument10 pagesAuditing 2nd Sem AY 2020-2021 Institutional Mock Board ExamGet BurnNo ratings yet

- Fico Interview PrepDocument112 pagesFico Interview PrepSOURABH KUMBHARNo ratings yet

- Psycho Sport LimitedDocument3 pagesPsycho Sport LimitedhvvNo ratings yet

- 3.2022 Sample DE THI Business EnglishDocument4 pages3.2022 Sample DE THI Business EnglishTrần Thị Tố NhưNo ratings yet