You might also like

- City Cash Flow StatementDocument2 pagesCity Cash Flow StatementSharon CarilloNo ratings yet

- Ias 7 Statement of Cashflows (F2)Document7 pagesIas 7 Statement of Cashflows (F2)Tawanda Tatenda Herbert100% (1)

- IAS 1 Presentation of Financial Statements (2021)Document17 pagesIAS 1 Presentation of Financial Statements (2021)Tawanda Tatenda Herbert100% (1)

- Cash Flow StatementDocument19 pagesCash Flow StatementCharu100% (1)

- Funds Flow Statement FormatDocument2 pagesFunds Flow Statement FormatBheemeswar ReddyNo ratings yet

- Analyze Cash Flow Statement in 40 CharactersDocument10 pagesAnalyze Cash Flow Statement in 40 CharactersRohit Roy100% (1)

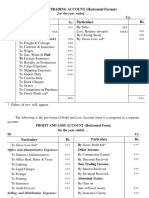

- Proforma of Final AccountsDocument3 pagesProforma of Final AccountsSarath kumar C100% (1)

- 1-Cash Flow StatementDocument21 pages1-Cash Flow StatementOvais Zia100% (1)

- Financial Statement AnalysisDocument46 pagesFinancial Statement AnalysisMusom BBANo ratings yet

- Cash Flow Statement AnalysisDocument3 pagesCash Flow Statement AnalysisSukumarVenkataNo ratings yet

- Cash Flow StatementDocument5 pagesCash Flow StatementDebaditya SenguptaNo ratings yet

- CompanyDocument4 pagesCompanyparwez_0505No ratings yet

- Template For Financial Statements and Question 2 Sept 2023Document4 pagesTemplate For Financial Statements and Question 2 Sept 2023Mohammed akbarNo ratings yet

- POA Formats and Financial StatementsDocument7 pagesPOA Formats and Financial StatementsWilliNo ratings yet

- Final Account VijDocument60 pagesFinal Account Vijamity_acel100% (1)

- Cash Flow StatementDocument16 pagesCash Flow Statementrajesh337masssNo ratings yet

- Fund From OperationDocument1 pageFund From OperationGood VibesNo ratings yet

- General Format For Final AccountsDocument2 pagesGeneral Format For Final AccountsGokulCj GroveNo ratings yet

- Financial Statements of Sole Trader (Unit-04) PDFDocument3 pagesFinancial Statements of Sole Trader (Unit-04) PDFImadNo ratings yet

- Dr. Ajay Dwivedi Professor Department of Financial StudiesDocument16 pagesDr. Ajay Dwivedi Professor Department of Financial StudiesKaran Pratap Singh100% (1)

- Unit - Iii Final Account: I.e., All Manufacturing Expenses, Carriage, Cartage, Freight, Duty EtcDocument9 pagesUnit - Iii Final Account: I.e., All Manufacturing Expenses, Carriage, Cartage, Freight, Duty EtcWelcome 1995No ratings yet

- Is SofpDocument2 pagesIs SofpHilwa FarhanNo ratings yet

- Annex D - SCFDocument44 pagesAnnex D - SCFJohn Eivor Go OrroNo ratings yet

- Operating Activities Are The Transactions From The Revenue Generating ActivitiesDocument3 pagesOperating Activities Are The Transactions From The Revenue Generating ActivitiesRaym FelixNo ratings yet

- Micro Notes On A2 IAL AccountingDocument15 pagesMicro Notes On A2 IAL AccountingRajibul Haque Shumon100% (1)

- Cash Flow Statement: by B.K.VashishthaDocument20 pagesCash Flow Statement: by B.K.VashishthaNadya Shamini100% (1)

- Secondary Book of Account: Prof. S. Y. ShewaleDocument10 pagesSecondary Book of Account: Prof. S. Y. Shewalesneharsh2370No ratings yet

- Fund Flow - RevisedDocument11 pagesFund Flow - RevisedModhish NothumanNo ratings yet

- Cash Flow Statement - FormatDocument2 pagesCash Flow Statement - FormatHassan AsgharNo ratings yet

- Managerial RemunerationDocument1 pageManagerial RemunerationRakshith S BNo ratings yet

- Accountancy All FormulaDocument23 pagesAccountancy All FormulaThe Unknown vlogger100% (1)

- Cash Flow Statement Examples As Per Direct Method: Report Name Sap Report T-CodeDocument6 pagesCash Flow Statement Examples As Per Direct Method: Report Name Sap Report T-Codejainendra100% (1)

- Format of Cash FlowDocument3 pagesFormat of Cash Flowsaldanha889No ratings yet

- Cash FlowDocument5 pagesCash FlowSirdar MukodzaniNo ratings yet

- Cash Flow Statements6Document28 pagesCash Flow Statements6kimuli FreddieNo ratings yet

- Intermediate Accounting Second Sem ReviewerDocument7 pagesIntermediate Accounting Second Sem ReviewerchxrlttxNo ratings yet

- Final AccountsDocument9 pagesFinal AccountsRositaNo ratings yet

- Ias 1-Presentation of Financial StatementsDocument21 pagesIas 1-Presentation of Financial StatementsChumani GqadaNo ratings yet

- Company Final Accounts ChapterDocument13 pagesCompany Final Accounts Chaptershanthala mNo ratings yet

- Preparation of Financial Statement For A Sole TraderDocument8 pagesPreparation of Financial Statement For A Sole TraderDebbie DebzNo ratings yet

- Cash Flow Notes 1Document2 pagesCash Flow Notes 1Kevin JoyNo ratings yet

- More Statement of Cash Flow Exercises-1Document8 pagesMore Statement of Cash Flow Exercises-1Juliana CaroNo ratings yet

- Final - Accounts Format PDFDocument13 pagesFinal - Accounts Format PDFajaychatta100% (1)

- Final - Accounts Format 234 PDFDocument13 pagesFinal - Accounts Format 234 PDFajaychattaNo ratings yet

- Annual Reports and Financial StatementsDocument10 pagesAnnual Reports and Financial Statementsfaith olaNo ratings yet

- Ias 1Document7 pagesIas 1ADEYANJU AKEEMNo ratings yet

- Ias 7 Cash Flow Statement ContinuedDocument8 pagesIas 7 Cash Flow Statement ContinuedMichael Bwire100% (1)

- Vertical Income Statement: FormatDocument5 pagesVertical Income Statement: FormatHermann Schmidt EbengaNo ratings yet

- A. Statement of Financial Position (Balance Sheet)Document5 pagesA. Statement of Financial Position (Balance Sheet)Majane TognoNo ratings yet

- Financial Statements Part A&bDocument6 pagesFinancial Statements Part A&b16115dxbpNo ratings yet

- An Income Statement and A Statement of Financial Position For LawyersDocument5 pagesAn Income Statement and A Statement of Financial Position For Lawyerstapiwa mafunduNo ratings yet

- Company Financials - Cash FlowDocument17 pagesCompany Financials - Cash FlowJack SangNo ratings yet

- Proforma of Trading PL and Balance SheetDocument2 pagesProforma of Trading PL and Balance SheetPranay Sai Garepally100% (3)

- Final Accounts of A BankDocument20 pagesFinal Accounts of A BankgyasiNo ratings yet

- Chapter 7Document15 pagesChapter 7msukri_81No ratings yet

- Notes Cash FlowDocument16 pagesNotes Cash FlowsamundeswaryNo ratings yet

- Chap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)Document18 pagesChap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)7a4374 hisNo ratings yet

- Accounting for manufacturing financial statementsDocument7 pagesAccounting for manufacturing financial statementsAlyx Gabrielle GocoNo ratings yet

- The Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeFrom EverandThe Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeNo ratings yet

- Capital Asset Investment: Strategy, Tactics and ToolsFrom EverandCapital Asset Investment: Strategy, Tactics and ToolsRating: 1 out of 5 stars1/5 (1)

- Corporation Accounting - Treasury SharesDocument4 pagesCorporation Accounting - Treasury SharesGuadaMichelleGripalNo ratings yet

- Types of SwapsDocument25 pagesTypes of SwapsBinal JasaniNo ratings yet

- 1f9w2d3t0kvd-FX Leveling Manual-SmartTraderDocument38 pages1f9w2d3t0kvd-FX Leveling Manual-SmartTraderAlesso KingNo ratings yet

- Account Statement: Penyata AkaunDocument2 pagesAccount Statement: Penyata AkaunAsyraf SyazwanNo ratings yet

- SonyDocument1 pageSonyamran mohammedNo ratings yet

- 10 Must-Read Books For Stock Market BeginnersDocument14 pages10 Must-Read Books For Stock Market BeginnersSovanlal Khamaru100% (1)

- MBA FF Group Project Assignment Fall 2020 - Group B3 (Indus Motor)Document23 pagesMBA FF Group Project Assignment Fall 2020 - Group B3 (Indus Motor)Aliza RizviNo ratings yet

- EMH AssignmentDocument8 pagesEMH AssignmentJonathanNo ratings yet

- Traders Dynamic Indicator TDIDocument26 pagesTraders Dynamic Indicator TDIPurity G. Mugo100% (1)

- BA7202-Financial Management Question BankDocument10 pagesBA7202-Financial Management Question BankHR HMA TECHNo ratings yet

- International Arbitrage and Interest Rate Parity Chapter 7 Flashcards - QuizletDocument11 pagesInternational Arbitrage and Interest Rate Parity Chapter 7 Flashcards - QuizletDa Dark PrinceNo ratings yet

- Mutual Fund ScriptDocument12 pagesMutual Fund ScriptSudheesh Murali NambiarNo ratings yet

- AGRICULTURAL FINANCE Class Notes 1Document23 pagesAGRICULTURAL FINANCE Class Notes 1ouko kevin100% (1)

- The Easy Forex Breakout Trend Trading Simple System Basic Manual VersionDocument30 pagesThe Easy Forex Breakout Trend Trading Simple System Basic Manual VersionChakrey LeaderNo ratings yet

- Buffet Bid For Media GeneralDocument21 pagesBuffet Bid For Media GeneralDahagam Saumith100% (1)

- IFRS 9 - Financial Instruments: Search Site..Document3 pagesIFRS 9 - Financial Instruments: Search Site..kæsiiiNo ratings yet

- KPMG Technical Terms Commercial Accounting and Tax LawDocument44 pagesKPMG Technical Terms Commercial Accounting and Tax LawIosias100% (3)

- Researching market conditions improves negotiationsDocument9 pagesResearching market conditions improves negotiationsMohamed ElsirNo ratings yet

- Karvy - Stockbroking LimitedDocument61 pagesKarvy - Stockbroking Limitedrangupadma67% (3)

- Tugas Aklan TM7Document7 pagesTugas Aklan TM7AdnanNo ratings yet

- Merger of Wella - P - G1Document44 pagesMerger of Wella - P - G1Avi JhaveriNo ratings yet

- ProfitabilityDocument30 pagesProfitabilitySumit KumarNo ratings yet

- Soal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Document9 pagesSoal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Vincenttio le CloudNo ratings yet

- Company Presentation (Blue Chip)Document17 pagesCompany Presentation (Blue Chip)lifechange2020No ratings yet

- 01 Capitalstructure Lecture ADocument76 pages01 Capitalstructure Lecture AKatarina SusaNo ratings yet

- Adani Group - How The World's 3rd Richest Man Is Pulling The Largest Con in Corporate History - Hindenburg ResearchDocument90 pagesAdani Group - How The World's 3rd Richest Man Is Pulling The Largest Con in Corporate History - Hindenburg ResearchmallikarjunbpatilNo ratings yet

- Singapore Airlines Financial AnalysisDocument16 pagesSingapore Airlines Financial AnalysisIncognito VyaktiNo ratings yet

- A STUDY ON PORTFOLIO MANAGEMENTDocument32 pagesA STUDY ON PORTFOLIO MANAGEMENTBiproteep Karmakar0% (1)

- Accounting P1 May-June 2023 EngDocument12 pagesAccounting P1 May-June 2023 EngKaren ErasmusNo ratings yet

- Answer Key Activity 12, 13, & 14Document5 pagesAnswer Key Activity 12, 13, & 14Yor MilizéNo ratings yet