You might also like

- Financial Statements ExplainedDocument27 pagesFinancial Statements ExplainedanurulxxNo ratings yet

- Net Working Capital Current Assets - Current LiabilitiesDocument11 pagesNet Working Capital Current Assets - Current LiabilitiesRahul YadavNo ratings yet

- Financial Management - Solved Paper 2015-2016 - 5th Sem B.SC HHA - Hmhub - Perfect ? Hub For 120k+ ? Hospitality ?? ? StudentsDocument22 pagesFinancial Management - Solved Paper 2015-2016 - 5th Sem B.SC HHA - Hmhub - Perfect ? Hub For 120k+ ? Hospitality ?? ? StudentsMOVIEZ FUNDANo ratings yet

- FFS - NumericalsDocument5 pagesFFS - NumericalsFunny ManNo ratings yet

- Gujarat Technological UniversityDocument6 pagesGujarat Technological UniversitymansiNo ratings yet

- Cashflowstatement 150402074118 Conversion Gate01Document30 pagesCashflowstatement 150402074118 Conversion Gate01vini2710No ratings yet

- 19 - Ch4 Weekly QuestionsDocument10 pages19 - Ch4 Weekly QuestionsCamilo ToroNo ratings yet

- Gujarat Technological UniversityDocument6 pagesGujarat Technological UniversitymansiNo ratings yet

- Unit IIIDocument9 pagesUnit IIIkuselvNo ratings yet

- Outcome. 3Document24 pagesOutcome. 3Sohel MemonNo ratings yet

- Bus. Finance W3-4 - C5 (Answer)Document5 pagesBus. Finance W3-4 - C5 (Answer)Rory GdLNo ratings yet

- Fund Flow Statement: by Dr. Aleem AnsariDocument18 pagesFund Flow Statement: by Dr. Aleem AnsariPRIYAL GUPTANo ratings yet

- Fin Reporting and FSA-fund Flow Statment 6th Sem by VS (Vinay Shaw0 For MorningDocument12 pagesFin Reporting and FSA-fund Flow Statment 6th Sem by VS (Vinay Shaw0 For MorningSarfraz AhmedNo ratings yet

- Topic 2 - Af09101 - Financial StatementsDocument42 pagesTopic 2 - Af09101 - Financial Statementsarusha afroNo ratings yet

- Chap 2Document16 pagesChap 2RABBINo ratings yet

- Financial Position Report & Cash Flow Statement Analyze Transactions To The AccountDocument32 pagesFinancial Position Report & Cash Flow Statement Analyze Transactions To The AccountRafi EffendyNo ratings yet

- Cashflowstatement 150402074118 Conversion Gate01Document39 pagesCashflowstatement 150402074118 Conversion Gate01vini2710No ratings yet

- Ma Internal Question BankDocument4 pagesMa Internal Question Bankvarmapriya712No ratings yet

- B.B.A., Sem.-IV CC-213: Corporate Financial StatementsDocument4 pagesB.B.A., Sem.-IV CC-213: Corporate Financial StatementsJJ NayakNo ratings yet

- Cash Flow StatementsDocument16 pagesCash Flow Statementsadnan arshadNo ratings yet

- FYJC Book Keeping and Accuntancy Topic Final AccountDocument4 pagesFYJC Book Keeping and Accuntancy Topic Final AccountRavichandraNo ratings yet

- M&a Basic Internal Reconstruction QDocument7 pagesM&a Basic Internal Reconstruction Qayushi aggarwalNo ratings yet

- Funds Flow StatementDocument5 pagesFunds Flow StatementAshfaq ZameerNo ratings yet

- MBA AFM Probs on FS Analysis, Ratio Analysis and Com SizeDocument6 pagesMBA AFM Probs on FS Analysis, Ratio Analysis and Com SizeAngelsony AmmuNo ratings yet

- FR (New) A MTP Final Mar 2021Document17 pagesFR (New) A MTP Final Mar 2021ritz meshNo ratings yet

- Financial StatementDocument40 pagesFinancial StatementbusebeeNo ratings yet

- Cash Flow Analysis - Lec 001Document26 pagesCash Flow Analysis - Lec 001Jocelyn LiwananNo ratings yet

- Cash FlowsDocument15 pagesCash FlowsAkshat DwivediNo ratings yet

- ACMA Unit 5 Problems - CFS PDFDocument3 pagesACMA Unit 5 Problems - CFS PDFPrabhat SinghNo ratings yet

- JKN - Acc - 13 - Question Paper - 131020Document10 pagesJKN - Acc - 13 - Question Paper - 131020adityatiwari122006No ratings yet

- Mendoza - UNIT 1 - Statement of Financial PositionDocument14 pagesMendoza - UNIT 1 - Statement of Financial PositionAim RubiaNo ratings yet

- 3rd Week Cash Flow AnalysisDocument19 pages3rd Week Cash Flow AnalysisCj TolentinoNo ratings yet

- Cashflow Statements Ias7Document11 pagesCashflow Statements Ias7Foni NancyNo ratings yet

- Chapter: Common Size, Comparative and Trend AnalysisDocument6 pagesChapter: Common Size, Comparative and Trend Analysiseldridatech pvt ltdNo ratings yet

- Financial statements analysisDocument3 pagesFinancial statements analysisFEBRI IRAWANNo ratings yet

- Internal Question Bank MA 2022Document7 pagesInternal Question Bank MA 2022singhalsanchit321No ratings yet

- Cash Flow Analysis: Mcgraw-Hill/Irwin © 2004 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument27 pagesCash Flow Analysis: Mcgraw-Hill/Irwin © 2004 The Mcgraw-Hill Companies, Inc., All Rights Reservedmabkhan_25No ratings yet

- RatioDocument24 pagesRatioSadika KhanNo ratings yet

- Lecture No. 2 - Financial Statements & Illustrative ProblemDocument6 pagesLecture No. 2 - Financial Statements & Illustrative ProblemJA LAYUG100% (1)

- ACCA FR Question Pack on Financial ReportingDocument52 pagesACCA FR Question Pack on Financial ReportingVasileios Lymperopoulos100% (1)

- Accountancy - Holiday Homework-Class12Document8 pagesAccountancy - Holiday Homework-Class12Ahill sudershanNo ratings yet

- Previous Year Question Paper (FSA)Document16 pagesPrevious Year Question Paper (FSA)Alisha ShawNo ratings yet

- Preparation & Analysis of Cash Flow StatementsDocument27 pagesPreparation & Analysis of Cash Flow StatementsAniket PanchalNo ratings yet

- Lesson 4 Week 5 FABM 2Document21 pagesLesson 4 Week 5 FABM 2Mikel Nelson AmpoNo ratings yet

- Case 21Document14 pagesCase 21Gabriela LueiroNo ratings yet

- Accounts Home Test 2Document7 pagesAccounts Home Test 2Ashish RaiNo ratings yet

- UNIT-4Document33 pagesUNIT-4b21ai008No ratings yet

- 676fund Flow Statement Solved ProblemsDocument3 pages676fund Flow Statement Solved ProblemsGovind SinghNo ratings yet

- Addtional Cash Flow Problems and SolutionsDocument7 pagesAddtional Cash Flow Problems and SolutionsHossein ParvardehNo ratings yet

- FinanceDocument4 pagesFinancejitendra.jgec8525No ratings yet

- LXL Gr12Accounting 08 Revision Interpretation-of-Financial-Statements 27mar2014 PDFDocument5 pagesLXL Gr12Accounting 08 Revision Interpretation-of-Financial-Statements 27mar2014 PDFNezer Byl P. VergaraNo ratings yet

- RATIO ANALYSIS Q 1 To 4Document5 pagesRATIO ANALYSIS Q 1 To 4gunjan0% (1)

- Lecture No 2Document4 pagesLecture No 2Avia Chelsy DeangNo ratings yet

- MS04Document34 pagesMS04Varun MandalNo ratings yet

- Interpretation of Public Sector Financial StatementsDocument4 pagesInterpretation of Public Sector Financial StatementsEsther AkpanNo ratings yet

- 2023 - Session12 - 13 FSA2 - MBA - SentDocument32 pages2023 - Session12 - 13 FSA2 - MBA - SentAkshat MathurNo ratings yet

- Accounts CH 6 Cash FlowDocument11 pagesAccounts CH 6 Cash Flowapsonline8585No ratings yet

- Laporan Arus KasDocument20 pagesLaporan Arus KasSyuhadakAl-FasuruniNo ratings yet

- FFS & CFSDocument15 pagesFFS & CFSNishaTripathiNo ratings yet

- Solution 2Document75 pagesSolution 2Asiful MowlaNo ratings yet

- BBS - 1st - Financial Accounting and AnalysisDocument46 pagesBBS - 1st - Financial Accounting and AnalysisJALDIMAINo ratings yet

- FABM2 Module 5 - FS AnalysisDocument11 pagesFABM2 Module 5 - FS AnalysisKimberly Abella CabreraNo ratings yet

- Comprehensive Exam FDocument14 pagesComprehensive Exam Fjdiaz_646247100% (1)

- Ap-1403 ReceivablesDocument18 pagesAp-1403 ReceivablesElaine YapNo ratings yet

- Week 7 Homework Lisa ChandlerDocument13 pagesWeek 7 Homework Lisa ChandlerShopno ChuraNo ratings yet

- Entrepreneurship Paper 3 Notes Marketung ManagementDocument23 pagesEntrepreneurship Paper 3 Notes Marketung Managementbashirahyusuf69No ratings yet

- MakalahDocument14 pagesMakalahImam Ank RezpectorNo ratings yet

- ACC 205 Complete Class HomeworkDocument41 pagesACC 205 Complete Class HomeworkAvicciNo ratings yet

- Hampton Suggested AnswersDocument5 pagesHampton Suggested Answersenkay12100% (3)

- Correction of ErrorsDocument15 pagesCorrection of ErrorsEliyah Jhonson100% (1)

- Business Purchase AgreementDocument9 pagesBusiness Purchase AgreementbalbirrNo ratings yet

- Chapter 3 - Accumulating Costs For Products and Services (1-20)Document24 pagesChapter 3 - Accumulating Costs For Products and Services (1-20)JAY AUBREY PINEDA100% (1)

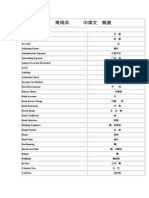

- 常用会计词汇中英文对照表Document8 pages常用会计词汇中英文对照表Owen ZhangNo ratings yet

- Midterm Quiz#1Document10 pagesMidterm Quiz#1Jo KeNo ratings yet

- 3 Choose Level 3 New COC 2011-1-1Document14 pages3 Choose Level 3 New COC 2011-1-1Dagnachew Weldegebriel100% (2)

- Audit of Cash and Cash Equivalents for Accounting StudentsDocument39 pagesAudit of Cash and Cash Equivalents for Accounting StudentsGeneral ScopiNo ratings yet

- Overview of Business Processes: © 2009 Pearson Education, Inc. Publishing As Prentice HallDocument20 pagesOverview of Business Processes: © 2009 Pearson Education, Inc. Publishing As Prentice HallCharles MK ChanNo ratings yet

- Sales: P1-,27A, OAO - 1LZB, O00 - )Document1 pageSales: P1-,27A, OAO - 1LZB, O00 - )Lovely Mae LariosaNo ratings yet

- IFM TB ch19Document11 pagesIFM TB ch19Faizan ChNo ratings yet

- Case Problems On Receivables PDFDocument5 pagesCase Problems On Receivables PDFPangitka100% (1)

- CHP 3Document78 pagesCHP 3Vivek SaraogiNo ratings yet

- R12 Project Accounting SetupsDocument183 pagesR12 Project Accounting SetupsmaddiboinaNo ratings yet

- Financial Statement Analysis Tools and TechniquesDocument11 pagesFinancial Statement Analysis Tools and TechniquesKarlo D. ReclaNo ratings yet

- Intermediate Accounting III ReviewerDocument3 pagesIntermediate Accounting III ReviewerRenalyn PascuaNo ratings yet

- Perpetual Inventory SystemDocument9 pagesPerpetual Inventory SystemAgdum BagdumNo ratings yet

- Financial Accounting Theory Test BankDocument13 pagesFinancial Accounting Theory Test BankPhilip Castro100% (3)

- Orca Share Media1583315619577Document13 pagesOrca Share Media1583315619577Sebastian Vincent Pulga PedrosaNo ratings yet

- Single & Double EntryDocument9 pagesSingle & Double EntryJoel VargheseNo ratings yet

- Financial Accounting Question SetDocument24 pagesFinancial Accounting Question SetAlireza KafaeiNo ratings yet