You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

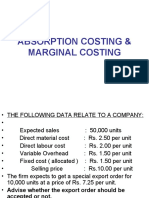

- Absorption and Marginal Costing Worked ExamplesDocument5 pagesAbsorption and Marginal Costing Worked ExamplesSUHRIT BISWASNo ratings yet

- Multi-Step Income Statement - CRDocument16 pagesMulti-Step Income Statement - CRVivian BastoNo ratings yet

- Process CostingDocument83 pagesProcess CostingMohammad MoosaNo ratings yet

- Absorption CostingDocument32 pagesAbsorption Costingsknco50% (2)

- Cost Volume Profit AnalysisDocument20 pagesCost Volume Profit AnalysisSidharth RayNo ratings yet

- Management AccountingDocument11 pagesManagement AccountingMalikwaheedNo ratings yet

- Absorption and Marginal CostingDocument34 pagesAbsorption and Marginal CostingOsama Khan100% (1)

- Cost SheetDocument29 pagesCost Sheetnidhisanjeet0% (1)

- GP AnalysisDocument25 pagesGP Analysismiles1280No ratings yet

- Acccob3 Long Quiz 3 CoverageDocument75 pagesAcccob3 Long Quiz 3 CoverageCaila Joice FavorNo ratings yet

- Jose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyDocument6 pagesJose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyBernadette CaduyacNo ratings yet

- Marginal and Absorption CostingDocument17 pagesMarginal and Absorption CostingHAHAHANo ratings yet

- 3 - Cost Flow Assumptions and Subsequent MeasurementDocument25 pages3 - Cost Flow Assumptions and Subsequent MeasurementJozelle Grace PadelNo ratings yet

- Absorption CostingDocument33 pagesAbsorption CostingMohit PaswanNo ratings yet

- Learning Activity 6 Variable Vs Absorption CostingDocument3 pagesLearning Activity 6 Variable Vs Absorption CostingEnergy Trading QUEZELCO 1No ratings yet

- Management Accounting & Control Variable CostingDocument3 pagesManagement Accounting & Control Variable CostingEnergy Trading QUEZELCO 1No ratings yet

- Assignment of Accounting 2022Document8 pagesAssignment of Accounting 2022sakhawatNo ratings yet

- Unit 1 - InventoriesDocument76 pagesUnit 1 - InventoriesZamarhadebe SilosamahlubiNo ratings yet

- 2.0 Absorption Versus Variable CostingDocument31 pages2.0 Absorption Versus Variable CostingAshutosh DayalNo ratings yet

- Chapter 8 W13Document28 pagesChapter 8 W13Joe JoyNo ratings yet

- CVP Bba 2020Document58 pagesCVP Bba 2020Loreen Maya0% (1)

- Marginal Costing and CVP Analysis: Group 4Document31 pagesMarginal Costing and CVP Analysis: Group 4Aiman Farhan100% (1)

- Chapter 10 - QDocument32 pagesChapter 10 - Qmohammedakbar88No ratings yet

- Grup 7 (Multi Product and Activity Based CVP Analysis) - DikonversiDocument13 pagesGrup 7 (Multi Product and Activity Based CVP Analysis) - DikonversiRahimah ImNo ratings yet

- Marginal CostingDocument30 pagesMarginal Costinganon_3722476140% (1)

- Jawaban MGT BiayaDocument9 pagesJawaban MGT BiayaRessa LiniNo ratings yet

- Marginal and Absorption CostingDocument8 pagesMarginal and Absorption CostingValérie CamangueNo ratings yet

- Cost Contribution Format vs. Traditional Format of Income StatementDocument24 pagesCost Contribution Format vs. Traditional Format of Income StatementFaizan Ahmed KiyaniNo ratings yet

- ACCCOB3Document10 pagesACCCOB3Jenine YamsonNo ratings yet

- Joint Cost - by ProductDocument15 pagesJoint Cost - by ProductRessa LarasatiNo ratings yet

- Cost Accounting Midterm ExamDocument37 pagesCost Accounting Midterm Examshynebright.phNo ratings yet

- Cost & RevenueDocument13 pagesCost & RevenueDeepikaa PoobalarajaNo ratings yet

- Inventory Count SlidesDocument47 pagesInventory Count SlidesHAFIZ MUHAMMAD UMAR FAROOQ RANA100% (1)

- SU3 Inventories Part A 2023-2Document27 pagesSU3 Inventories Part A 2023-2machabelanosiphoNo ratings yet

- Ch19 Guan Hansen MowenDocument38 pagesCh19 Guan Hansen MowenratuhsNo ratings yet

- Absorption Vs MarginalDocument9 pagesAbsorption Vs MarginalSidharth RayNo ratings yet

- Chapter 3Document29 pagesChapter 3natnael hiruyNo ratings yet

- Business Profile: Albay, Kristina Lacson, Joceleen Naldoza, Rominna Noro, Aljerico Ubas, GivenDocument51 pagesBusiness Profile: Albay, Kristina Lacson, Joceleen Naldoza, Rominna Noro, Aljerico Ubas, GivenKCNo ratings yet

- BU7300 - Corporate Finance Capital Budgeting Week 1Document21 pagesBU7300 - Corporate Finance Capital Budgeting Week 1Moony TamimiNo ratings yet

- Absorption Costing (Or Full Costing) and Marginal CostingDocument11 pagesAbsorption Costing (Or Full Costing) and Marginal CostingCharsi Unprofessional BhaiNo ratings yet

- Capital Budgeting: R.KasilingamDocument71 pagesCapital Budgeting: R.Kasilingamvijayadarshini vNo ratings yet

- Accounting For The Merchandising Firm Chapter 7Document56 pagesAccounting For The Merchandising Firm Chapter 7Rupesh PolNo ratings yet

- Process CostingDocument66 pagesProcess Costingarshad mNo ratings yet

- CH 3Document17 pagesCH 3trishanjaliNo ratings yet

- 2 172 18 ToànDocument3 pages2 172 18 ToànlongphungspNo ratings yet

- CVP AnalysisDocument20 pagesCVP AnalysisKopanang LeokanaNo ratings yet

- HOBA Special ProbDocument14 pagesHOBA Special ProbRujean Salar AltejarNo ratings yet

- Chap7vanderbeck ReviewerDocument8 pagesChap7vanderbeck ReviewerSaeym SegoviaNo ratings yet

- Management Accounting Part5Document20 pagesManagement Accounting Part5Trần Doãn HuyNo ratings yet

- Chapter Two Managerial Accounting, Cost Terminologies and ClassificationsDocument26 pagesChapter Two Managerial Accounting, Cost Terminologies and ClassificationsSiraj MohammedNo ratings yet

- Variable CostingDocument34 pagesVariable CostingScraper LancelotNo ratings yet

- Absorption and Variable CostingDocument6 pagesAbsorption and Variable CostingEvangelista, Trisha Gael V.100% (1)

- Cost-Volume-Profit Analysis and Relevant CostingDocument39 pagesCost-Volume-Profit Analysis and Relevant CostingJai AceNo ratings yet

- Understanding To Process CostingDocument43 pagesUnderstanding To Process CostingSarim Saleheen LariNo ratings yet

- Accounting RatiosDocument30 pagesAccounting RatiosPetrinaNo ratings yet

- Variable CostingDocument34 pagesVariable CostingAra Marie MagnayeNo ratings yet

- Fma Assignment 3Document5 pagesFma Assignment 3Abdul AhmedNo ratings yet

- Questions and Answers For MGT 3 000 Level 23Document15 pagesQuestions and Answers For MGT 3 000 Level 23Monsonedu IkechukwuNo ratings yet

- Lecture 12 Strategies in Action Continuation Version 2Document45 pagesLecture 12 Strategies in Action Continuation Version 2Catherine LeroNo ratings yet

- Module 12 MACC423 Eugene A RuanoDocument14 pagesModule 12 MACC423 Eugene A RuanoCatherine LeroNo ratings yet

- JOB ORDER COSTING BSOM 4A Accounting FDocument58 pagesJOB ORDER COSTING BSOM 4A Accounting FCatherine LeroNo ratings yet

- Eugene A Ruano Module 2 BTax223Document8 pagesEugene A Ruano Module 2 BTax223Catherine LeroNo ratings yet