You might also like

- Chapter Three 3. Recording Common Transactions of FGEDocument19 pagesChapter Three 3. Recording Common Transactions of FGEGirmaNo ratings yet

- Chapter 3Document38 pagesChapter 3Emebet TesemaNo ratings yet

- Unit 3Document15 pagesUnit 3TIZITAW MASRESHANo ratings yet

- FGE Chapter 3 To 5Document40 pagesFGE Chapter 3 To 5mubarek kemalNo ratings yet

- Chapter Three Analysis of Transactions: 3.1. Cash TransfersDocument10 pagesChapter Three Analysis of Transactions: 3.1. Cash TransfersGedionNo ratings yet

- Example: Assume A Public Body Receives From MOFED A Transfer of Birr 100,000 ForDocument32 pagesExample: Assume A Public Body Receives From MOFED A Transfer of Birr 100,000 ForSentayehu GebeyehuNo ratings yet

- Chapter 3 FGE MinDocument23 pagesChapter 3 FGE MinGedion100% (2)

- Manual 3 - Federal Accounting System Chapter 10. TransactionsDocument47 pagesManual 3 - Federal Accounting System Chapter 10. TransactionsKumera Dinkisa ToleraNo ratings yet

- Chapter 3 Ethiopian Govt AcctingDocument19 pagesChapter 3 Ethiopian Govt AcctingwubeNo ratings yet

- Palaña Nego CasesDocument3 pagesPalaña Nego CasesMary Ann IsananNo ratings yet

- LiabilitiesDocument6 pagesLiabilitiesBS Accoutancy St. SimonNo ratings yet

- Account Title Account Code Debit Credi T: To Recognize Collection of Refund of Overpayment of ExpensesDocument11 pagesAccount Title Account Code Debit Credi T: To Recognize Collection of Refund of Overpayment of ExpensesQuennie DesullanNo ratings yet

- FGE Chapter 4Document58 pagesFGE Chapter 4mubarek kemalNo ratings yet

- Midterms Gov AccountingDocument72 pagesMidterms Gov AccountingEloisa JulieanneNo ratings yet

- Government AccountingDocument25 pagesGovernment AccountingArdyll N100% (1)

- Bank Reconciliation1Document18 pagesBank Reconciliation1Kim Ella50% (2)

- Chapter 3 Part 1Document6 pagesChapter 3 Part 1AliansNo ratings yet

- River Bank Trades HDFC Bank: Reconciliation StatementDocument1 pageRiver Bank Trades HDFC Bank: Reconciliation StatementmoqimNo ratings yet

- Activity For Receipts and CollectionDocument4 pagesActivity For Receipts and CollectionHinataNo ratings yet

- Government Accounting System (NGAS) Manual Had Been Revised As Prompted by The Implementation of The Philippine PublicDocument14 pagesGovernment Accounting System (NGAS) Manual Had Been Revised As Prompted by The Implementation of The Philippine PublicMarco ForelNo ratings yet

- Notes6 DisbursementsDocument15 pagesNotes6 DisbursementsRachel GellerNo ratings yet

- POB1 Test CycleDocument16 pagesPOB1 Test CycleKashyapNo ratings yet

- Outward Telegraphic Transfer Form (2) - TOSOH 008Document2 pagesOutward Telegraphic Transfer Form (2) - TOSOH 008kanishka112No ratings yet

- Funds Transfer Amend FormDocument1 pageFunds Transfer Amend FormDeewan E YaarNo ratings yet

- Funds Transfer Application and Agreement: Q Q Q Q QDocument2 pagesFunds Transfer Application and Agreement: Q Q Q Q QAlejandro L GonzalezNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument38 pagesAccounting For Disbursements and Related TransactionsBerg100% (1)

- ICICI NEFT Application FormDocument1 pageICICI NEFT Application FormAtul Kawale100% (1)

- Project: Payment of Advance of Birr 20,000 Is MadeDocument2 pagesProject: Payment of Advance of Birr 20,000 Is MadeGedionNo ratings yet

- ChecklistDocument1 pageChecklistOmprakash LonikarNo ratings yet

- Rem145r8 MDocument3 pagesRem145r8 MBrijesh Pratap SinghNo ratings yet

- Accountancy-Books of Prime EntryDocument8 pagesAccountancy-Books of Prime EntryGedie Rocamora100% (1)

- CHap 6 Notes Gov AccDocument3 pagesCHap 6 Notes Gov AccLika MejidoNo ratings yet

- Work Flow of Walton OfficeDocument6 pagesWork Flow of Walton OfficeSARFRAZ AHMED BhuttoNo ratings yet

- QUIZ in Government Accounting Disbursements: (Group 3)Document6 pagesQUIZ in Government Accounting Disbursements: (Group 3)TokkiNo ratings yet

- SAP Exercise Controlling Reports RequirementsDocument1 pageSAP Exercise Controlling Reports RequirementsLee SuarezNo ratings yet

- Supplemental AppropriationDocument11 pagesSupplemental AppropriationLily PlantNo ratings yet

- PRF Macalalad PME ReimbursementDocument5 pagesPRF Macalalad PME Reimbursementmelecio.macalalad.jrNo ratings yet

- Addendun FormDocument1 pageAddendun FormjeshurunokhipoNo ratings yet

- Bank Reconciliation StatementDocument13 pagesBank Reconciliation StatementAli Hassan100% (1)

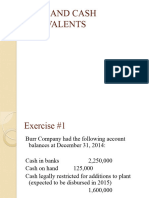

- Cash and Cash EquivalentsDocument38 pagesCash and Cash EquivalentschristianallenmlagosNo ratings yet

- PNB V. CA - 256 SCRA 491 FACTS: DECS Issued A Check in Favor of Abante Marketing Containing A Specific Serial NumberDocument1 pagePNB V. CA - 256 SCRA 491 FACTS: DECS Issued A Check in Favor of Abante Marketing Containing A Specific Serial NumberRL N DeiparineNo ratings yet

- Outstanding Processing FeeDocument2 pagesOutstanding Processing Feeapi-3708362100% (1)

- FIN WI 001 Image Marked PDFDocument10 pagesFIN WI 001 Image Marked PDFGregurius DaniswaraNo ratings yet

- Government Accounting ProblemsDocument4 pagesGovernment Accounting ProblemsApril ManjaresNo ratings yet

- Ama AccountingDocument3 pagesAma AccountingGabriel JacaNo ratings yet

- Accounting For Government and Not-For-Profit Organizations: ACCO 30033Document24 pagesAccounting For Government and Not-For-Profit Organizations: ACCO 30033hehehedontmind me100% (1)

- CA Darshan JainDocument49 pagesCA Darshan JainadiNo ratings yet

- PLP Government Accounting Final ExamDocument4 pagesPLP Government Accounting Final ExamApril ManjaresNo ratings yet

- Deped Coa2011 Observation RecommendationDocument81 pagesDeped Coa2011 Observation RecommendationAnthony Sutton100% (7)

- Module No - Title: MO5 - Disbursements Time Frame: 1 Week - 3 Hrs Learning ObjectivesDocument5 pagesModule No - Title: MO5 - Disbursements Time Frame: 1 Week - 3 Hrs Learning Objectivesbobo kaNo ratings yet

- PLP Government Accounting Mid-Term ExamDocument4 pagesPLP Government Accounting Mid-Term ExamApril Manjares100% (2)

- Bank Reconciliation StatementsDocument8 pagesBank Reconciliation Statementssamaraksingh03No ratings yet

- Cash and Account Receivable: Tugas Pengantar Praktik Pengauditan Pertemuan VDocument18 pagesCash and Account Receivable: Tugas Pengantar Praktik Pengauditan Pertemuan VwillyNo ratings yet

- Module 2Document19 pagesModule 2Cassandra VenecarioNo ratings yet

- Archie Tin PhilDocument91 pagesArchie Tin PhilYrolle Lynart AldeNo ratings yet

- Outstanding Processing FeeDocument2 pagesOutstanding Processing Feeapi-3708362100% (1)

- CHAPTER 3.pptx - ACC9 EditedDocument30 pagesCHAPTER 3.pptx - ACC9 EditedAngelica CastilloNo ratings yet

- Bank Alfalah Clearance DepartmentDocument7 pagesBank Alfalah Clearance Departmenthassan_shazaib100% (1)

- Notes ReceiDocument2 pagesNotes ReceiDIANE EDRANo ratings yet

- Tax 3 PRELIM QUIZZESDocument46 pagesTax 3 PRELIM QUIZZESAngela Miles DizonNo ratings yet

- MAF Mixed and Yield Variances (Eng)Document8 pagesMAF Mixed and Yield Variances (Eng)BirukNo ratings yet

- Nism Equity Derivatives Study NotesDocument27 pagesNism Equity Derivatives Study NotesHemant bhanawatNo ratings yet

- Guia 05 Reading Innovation in BusinessDocument5 pagesGuia 05 Reading Innovation in BusinessDJ Johan-MNo ratings yet

- Welcome To Everest Insurance CoDocument2 pagesWelcome To Everest Insurance Cosrijan consultancyNo ratings yet

- Mis Report Month of Feb 2022Document14 pagesMis Report Month of Feb 2022mikky_kumarNo ratings yet

- Online Syllabus: Arts Marketing Sample Llams 13/Hm&Fn Art 502Document15 pagesOnline Syllabus: Arts Marketing Sample Llams 13/Hm&Fn Art 502Agnes Tika SetiariniNo ratings yet

- Harga Satuan 2018Document33 pagesHarga Satuan 2018Mohammad Reza PahleviNo ratings yet

- TheEconomist 2024 04 20Document344 pagesTheEconomist 2024 04 20RodrigoNo ratings yet

- Universitas Bina Nusantara: Catering)Document2 pagesUniversitas Bina Nusantara: Catering)Aldo PutraNo ratings yet

- ABSLI Multiplier FundDocument1 pageABSLI Multiplier FundTanveer AhmadNo ratings yet

- Nation With Namo Cover Letter - Abhay GuptaDocument1 pageNation With Namo Cover Letter - Abhay GuptaAbhay GuptaNo ratings yet

- Money Maker-Ed Sheeran: Ed Sheeran's Net Worth Versus The Richest Musicians Under 30 (UK and Ireland)Document2 pagesMoney Maker-Ed Sheeran: Ed Sheeran's Net Worth Versus The Richest Musicians Under 30 (UK and Ireland)Marian PîrjolNo ratings yet

- State OF NEW Mexico: Lp-Gas Examinations Candidate Information BulletinDocument14 pagesState OF NEW Mexico: Lp-Gas Examinations Candidate Information BulletinAndrew YazzieNo ratings yet

- Jepretan Layar 2024-01-02 Pada 21.04.17Document41 pagesJepretan Layar 2024-01-02 Pada 21.04.17dewipuspita1900No ratings yet

- Annexure Form II and III AMMAIYAPANAGARDocument3 pagesAnnexure Form II and III AMMAIYAPANAGARGANDHILAL mNo ratings yet

- Instructions For Solo Poles: DetectorDocument2 pagesInstructions For Solo Poles: Detectorchaikal alghifariNo ratings yet

- 314681ea enDocument4 pages314681ea enTalila SidaNo ratings yet

- CPI Trac Nghiem 30 CâuDocument6 pagesCPI Trac Nghiem 30 Câunessyhen6No ratings yet

- Chapter 16: Partnership Liquidation: Advanced AccountingDocument36 pagesChapter 16: Partnership Liquidation: Advanced AccountingSatriany ElitNo ratings yet

- Masterclass 3.2Document6 pagesMasterclass 3.2Amit PrasadNo ratings yet

- A Complete Guide To Volume Price Analysis Read The Book Then Read The Market by Anna Coulling (Z-Lib - Org) (121-180)Document60 pagesA Complete Guide To Volume Price Analysis Read The Book Then Read The Market by Anna Coulling (Z-Lib - Org) (121-180)Getulio José Mattos Do Amaral Filho100% (1)

- The Ultimate Guide To Creating A Brand Messaging StrategyDocument42 pagesThe Ultimate Guide To Creating A Brand Messaging StrategyTrangThuCao100% (1)

- Chapter 2Document52 pagesChapter 2Mehedi Hasan FoyshalNo ratings yet

- Construction Management FoundationsDocument15 pagesConstruction Management FoundationsJuan Pablo CortésNo ratings yet

- Bullying, Cyberbullying and Hate SpeechDocument33 pagesBullying, Cyberbullying and Hate SpeechEve AthanasekouNo ratings yet

- Alno Presentasi July 2020Document16 pagesAlno Presentasi July 2020Iznan KholisNo ratings yet

- Accounting 4 Provisions and ContingenciesDocument4 pagesAccounting 4 Provisions and ContingenciesMicaela EncinasNo ratings yet

- رفاـــــسملل ةيحـــــصلا ةقاـــــطبلا Fiche Sanitaire du Passager / Public Health Passenger Form - CoronavirusDocument1 pageرفاـــــسملل ةيحـــــصلا ةقاـــــطبلا Fiche Sanitaire du Passager / Public Health Passenger Form - CoronavirusBLED PRESSNo ratings yet

- Corporations OutlineDocument44 pagesCorporations Outlinecflash94100% (1)