You might also like

- Budgetary ControlDocument28 pagesBudgetary ControlDidie Diyanah0% (1)

- BBAA 31043 Handout 03Document5 pagesBBAA 31043 Handout 03chrystila0307No ratings yet

- Typesofbudgets 12897115325477 Phpapp02Document23 pagesTypesofbudgets 12897115325477 Phpapp02Michael Allen JonesNo ratings yet

- CH 5 Flexible BudgetDocument23 pagesCH 5 Flexible Budgettamirat tadeseNo ratings yet

- MODULE 7 BudgetingDocument6 pagesMODULE 7 BudgetingKatrina Peralta FabianNo ratings yet

- Budgeting P-2Document4 pagesBudgeting P-2Ferb CruzadaNo ratings yet

- Flexible Budgets & Variance AnalysisDocument23 pagesFlexible Budgets & Variance Analysised tuNo ratings yet

- T2 Budgeting Behaviour (A)Document3 pagesT2 Budgeting Behaviour (A)JIN FEN SOONo ratings yet

- P1 1C.50c9001 NotesDocument100 pagesP1 1C.50c9001 Notesshambhavishukla.mba21No ratings yet

- T1 Planning, Budgeting & Controlling (Ans)Document3 pagesT1 Planning, Budgeting & Controlling (Ans)JIN FEN SOONo ratings yet

- Topic 1 Budgeting & Budgetary Control v2020p Part2Document35 pagesTopic 1 Budgeting & Budgetary Control v2020p Part2Siti NadiahNo ratings yet

- Chapter IIDocument17 pagesChapter IIBereket DesalegnNo ratings yet

- MA, CH 06Document9 pagesMA, CH 06Nahom AberaNo ratings yet

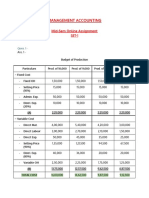

- Arjun Salwan - Management Accounting (SET-1)Document3 pagesArjun Salwan - Management Accounting (SET-1)Arjun SalwanNo ratings yet

- BudgetingDocument62 pagesBudgetingkalamabikoko01No ratings yet

- Budgeting: Afzal Ahmed, Fca Finance Controller NagadDocument19 pagesBudgeting: Afzal Ahmed, Fca Finance Controller NagadsajedulNo ratings yet

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- Cost and Management AccountingDocument5 pagesCost and Management AccountingSolve AssignmentNo ratings yet

- AMAB 233 Management Accounting Semester 2 2017 / 2018: in Budgeting Process DiscussDocument23 pagesAMAB 233 Management Accounting Semester 2 2017 / 2018: in Budgeting Process DiscussFaizah MKNo ratings yet

- Flexible Budgets Direct Cost Variances Management ControlDocument64 pagesFlexible Budgets Direct Cost Variances Management ControlJingxuan LuoNo ratings yet

- CHAPTER FOUR Cost and MGMT ACCTDocument12 pagesCHAPTER FOUR Cost and MGMT ACCTFeleke TerefeNo ratings yet

- Lecture 5-6 BudgetingDocument15 pagesLecture 5-6 BudgetingAfzal AhmedNo ratings yet

- Budgetary Planning and ControlDocument28 pagesBudgetary Planning and ControlJass PablaNo ratings yet

- Udgetary Ontrol: Presented By:-Sonali Mohite (34) Ankita YewleDocument14 pagesUdgetary Ontrol: Presented By:-Sonali Mohite (34) Ankita YewleMansi DeokarNo ratings yet

- Cipfa WB4Document43 pagesCipfa WB4Nassir CeellaabeNo ratings yet

- Chapter IVDocument10 pagesChapter IVeyasuNo ratings yet

- Cost II Chap I-1Document52 pagesCost II Chap I-1Etsub SamuelNo ratings yet

- 2020-08 High-Low Method, Flexible BudgetDocument5 pages2020-08 High-Low Method, Flexible BudgetDenis GonzálezNo ratings yet

- Management Accounting 2009Document19 pagesManagement Accounting 2009wizirangaNo ratings yet

- Technical Article Budgeting - Part 1Document4 pagesTechnical Article Budgeting - Part 1Iqmal khushairiNo ratings yet

- RESPONSIBILITY ACCOUNTING - A System of Accounting Wherein Performance, Based OnDocument8 pagesRESPONSIBILITY ACCOUNTING - A System of Accounting Wherein Performance, Based OnHarvey AguilarNo ratings yet

- Types of Budgeting Techniques: Topic 4Document59 pagesTypes of Budgeting Techniques: Topic 4Sullivan LyaNo ratings yet

- PM Tutorial 1Document5 pagesPM Tutorial 1EmmaNo ratings yet

- Introduction To Cost AccountingDocument40 pagesIntroduction To Cost AccountingMuhammad HabibNo ratings yet

- Budgeting Ch09Document10 pagesBudgeting Ch09CM_NguyenNo ratings yet

- Introduction To Budgets and The Master BudgetDocument33 pagesIntroduction To Budgets and The Master BudgetkunalNo ratings yet

- Planning and Managerial Application: Cost-Volume-Profit Analysis and Variable CostingDocument7 pagesPlanning and Managerial Application: Cost-Volume-Profit Analysis and Variable Costingviren guptaNo ratings yet

- Management Advisory Services: Responsibility Accounting & Transfer PricingDocument9 pagesManagement Advisory Services: Responsibility Accounting & Transfer PricingVanessa Arizo ValenciaNo ratings yet

- FIXED AND FLEXIBLE BUDGETS: KEY DIFFERENCESDocument3 pagesFIXED AND FLEXIBLE BUDGETS: KEY DIFFERENCESSunita BasakNo ratings yet

- FNSACC507 Provide Management Accounting InformationDocument13 pagesFNSACC507 Provide Management Accounting InformationSyed Bilal AliNo ratings yet

- Unit - 4Document40 pagesUnit - 4GHUDIRNo ratings yet

- Responsibility Accounting, Segment Evaluation, and Transfer PricingDocument4 pagesResponsibility Accounting, Segment Evaluation, and Transfer PricingAlliahData100% (1)

- Solution Manual For Managerial Accounting 10th EditionDocument33 pagesSolution Manual For Managerial Accounting 10th EditionVanessaMerrittdqes100% (38)

- Cost 2 ch3Document10 pagesCost 2 ch3Eid AwilNo ratings yet

- Week 8 - Lecture Budgeting v3Document23 pagesWeek 8 - Lecture Budgeting v3NabilNo ratings yet

- Budgetary Control and Responsibilty AccountingDocument34 pagesBudgetary Control and Responsibilty Accountingtentoone50% (4)

- Chapter 1 Introduction To Management AccountingDocument18 pagesChapter 1 Introduction To Management AccountingSumitha Kali ThassNo ratings yet

- Strategic performance measurementDocument97 pagesStrategic performance measurementspongebob SquarepantsNo ratings yet

- Budgetary Control and Responsibility AccountingDocument56 pagesBudgetary Control and Responsibility AccountingNickNo ratings yet

- Strat EssayDocument7 pagesStrat EssaydmangiginNo ratings yet

- Manage Big Red Bicycle BudgetDocument9 pagesManage Big Red Bicycle BudgetCuliikz Ade AblughNo ratings yet

- Budget Control StudentDocument22 pagesBudget Control StudenthnnnaNo ratings yet

- Session 2: Budget As A System by by Dr. Anubha SrivastavaDocument28 pagesSession 2: Budget As A System by by Dr. Anubha SrivastavaanubhaNo ratings yet

- Variable Costing as a Management ToolDocument4 pagesVariable Costing as a Management ToolHaika ContiNo ratings yet

- Budgetary Planning and ControlDocument25 pagesBudgetary Planning and ControlDagnachew TsegayeNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Implementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesFrom EverandImplementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesNo ratings yet

- Financial Performance Measures and Value Creation: the State of the ArtFrom EverandFinancial Performance Measures and Value Creation: the State of the ArtNo ratings yet

- Cost Reduction Strategies for the Manufacturing Sector With Application of Microsoft ExcelFrom EverandCost Reduction Strategies for the Manufacturing Sector With Application of Microsoft ExcelNo ratings yet

- Sentencias Judiciales Que No Fueron Beneficiadas Con El D.S 279-2020-Ef en Calidad de Cosa JuzgadaDocument4 pagesSentencias Judiciales Que No Fueron Beneficiadas Con El D.S 279-2020-Ef en Calidad de Cosa JuzgadaAlex moises Quispe allpasNo ratings yet

- Context CluesDocument2 pagesContext CluesDorepe IconNo ratings yet

- Engineers Australia Code of EthicsDocument4 pagesEngineers Australia Code of EthicsChungsrobot ManufacturingcompanyNo ratings yet

- Human Rights & Social Justice Mission: Application Form For Membership of "HRSJM"Document1 pageHuman Rights & Social Justice Mission: Application Form For Membership of "HRSJM"Venkates WaranNo ratings yet

- Book One: by John Lewis and Andrew AydinDocument6 pagesBook One: by John Lewis and Andrew AydinAbrams BooksNo ratings yet

- Rational choice theory - Understanding individual decision-making through plausible choicesDocument1 pageRational choice theory - Understanding individual decision-making through plausible choicesKaren TanqueridoNo ratings yet

- The Kindhearted SparrowDocument8 pagesThe Kindhearted Sparrowpjas0001No ratings yet

- महारा दुकाने व आ थापना (नोकर चे व सेवाशत चे व नयमन) नयम, २०१८ Form - ‘F'Document3 pagesमहारा दुकाने व आ थापना (नोकर चे व सेवाशत चे व नयमन) नयम, २०१८ Form - ‘F'Sachin SBNo ratings yet

- Module 2 Section 1Document12 pagesModule 2 Section 1Grace CumamaoNo ratings yet

- Entrepreneur ReviewerDocument3 pagesEntrepreneur ReviewerJorlan Evroem R. MarcoNo ratings yet

- Alison M. Jaggar - Susan Bordo - Gender - Body - Knowledge - Feminist Reconstructions of Being and Knowing-Rutgers University Press (1989)Document522 pagesAlison M. Jaggar - Susan Bordo - Gender - Body - Knowledge - Feminist Reconstructions of Being and Knowing-Rutgers University Press (1989)sarmahpuja9No ratings yet

- Chapter 3 - A Firm Production DateDocument2 pagesChapter 3 - A Firm Production Datemae KuanNo ratings yet

- EO 62A Activation of IMTDocument1 pageEO 62A Activation of IMTGeorge Jeffrey TindoyNo ratings yet

- Tingkat Kepuasan PasienDocument7 pagesTingkat Kepuasan PasienRirisNo ratings yet

- Session # 7 - Sociogram As A Diagnositic ToolDocument18 pagesSession # 7 - Sociogram As A Diagnositic ToolSHWETA SINGHAL PGPHRM 2021-23 Batch0% (1)

- Gas Agency Mangament SystemDocument4 pagesGas Agency Mangament SystemPrakash SinghNo ratings yet

- Module 5Document7 pagesModule 5AstxilNo ratings yet

- Lesson 1Document15 pagesLesson 1MARIETTANo ratings yet

- GOOD NEWS, BAD NEWS BANK CUSTOMER SERVICE DILEMMADocument8 pagesGOOD NEWS, BAD NEWS BANK CUSTOMER SERVICE DILEMMAHariharran K SNo ratings yet

- Learning Activity 1: Stand Points On Philosophers PhilosophyDocument4 pagesLearning Activity 1: Stand Points On Philosophers PhilosophyMonica De GuzmanNo ratings yet

- Janis, Irving L. Groupthink (43-44, 46, 74-76)Document6 pagesJanis, Irving L. Groupthink (43-44, 46, 74-76)John Dounas100% (1)

- Initial TQ IphpDocument5 pagesInitial TQ IphpselNo ratings yet

- Referral LetterDocument74 pagesReferral LetterZettee GarciaNo ratings yet

- Nietzsche (L6/L7) : Introduction (Oxford, 2001) Is A Good Place To BeginDocument5 pagesNietzsche (L6/L7) : Introduction (Oxford, 2001) Is A Good Place To BeginMusafraPressNo ratings yet

- Lead To Win Harris en 46749Document7 pagesLead To Win Harris en 46749petraki_boyNo ratings yet

- Bahasa Inggris: Smk/MakDocument5 pagesBahasa Inggris: Smk/MakMrs. GeeGee ChannelNo ratings yet

- DILG Technical Notes for LCAT-VAWC Functionality AssessmentDocument13 pagesDILG Technical Notes for LCAT-VAWC Functionality AssessmentiimignacioNo ratings yet

- Bioethics AssessmentDocument3 pagesBioethics AssessmentElizabethNo ratings yet

- Case Study 03Document2 pagesCase Study 03professorchanakyaNo ratings yet

- Case StudyDocument4 pagesCase StudyAryan Chandra ShandilyaNo ratings yet