You might also like

- MT and MX Equivalence TableDocument20 pagesMT and MX Equivalence TablejcskNo ratings yet

- Certificate in Securities Ed15Document340 pagesCertificate in Securities Ed15Westa Geafrica100% (4)

- March PitNews Schaap PDFDocument7 pagesMarch PitNews Schaap PDFRajasekaran MNo ratings yet

- Answer: D. P16, 000Document13 pagesAnswer: D. P16, 000JESSA ANN A. TALABOC100% (2)

- Treasury Operations - Front Office, Back OfficeDocument28 pagesTreasury Operations - Front Office, Back Officeshrikant shinde80% (20)

- Tail Risk Management - PIMCO Paper 2008Document9 pagesTail Risk Management - PIMCO Paper 2008Geouz100% (1)

- Ebook College Accounting A Career Approach 13Th Edition Scott Solutions Manual Full Chapter PDFDocument52 pagesEbook College Accounting A Career Approach 13Th Edition Scott Solutions Manual Full Chapter PDFkhucly5cst100% (9)

- Cash and Cash Equivalent AuditingDocument8 pagesCash and Cash Equivalent Auditing수지No ratings yet

- Accounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionFrom EverandAccounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionRating: 2.5 out of 5 stars2.5/5 (2)

- Capital BudgetingDocument65 pagesCapital Budgetingarjunmba119624No ratings yet

- Book 3 - Financial Markets & Products PDFDocument383 pagesBook 3 - Financial Markets & Products PDFSandesh SinghNo ratings yet

- WWW - Edutap.co - In: Forex Markets - Video 1Document51 pagesWWW - Edutap.co - In: Forex Markets - Video 1SaumyaNo ratings yet

- Principles of Accounts: The Cash Book The Petty Cash BookDocument24 pagesPrinciples of Accounts: The Cash Book The Petty Cash BookAts Sheikh100% (1)

- Ranganatham - Security Analysis and Portfolio Management, 2e (2011)Document3,577 pagesRanganatham - Security Analysis and Portfolio Management, 2e (2011)Yash Raj SinghNo ratings yet

- Bill Williams New Trading DimensionsDocument24 pagesBill Williams New Trading DimensionsAmine Elghazi50% (2)

- Forex Samurai Robot: User's Guide ForDocument7 pagesForex Samurai Robot: User's Guide ForHaslucky Tinashe Makuwaza100% (1)

- Chapter 2 Cashiering and Banking May 2010Document32 pagesChapter 2 Cashiering and Banking May 2010Berbagi UsahaNo ratings yet

- World Map: Middle East Europe Africa Asia North America Central, South America South West PacificDocument32 pagesWorld Map: Middle East Europe Africa Asia North America Central, South America South West Pacificvenkat100% (1)

- Treasury Management OverviewDocument47 pagesTreasury Management Overviewlakshika madushaniNo ratings yet

- 13463course Curriculum Forex PDFDocument13 pages13463course Curriculum Forex PDFshubh.icai0090No ratings yet

- KH Audit Foreign Currency TransactionsDocument6 pagesKH Audit Foreign Currency TransactionsФенимор КупърNo ratings yet

- Lfar by PG 25.03.2021Document47 pagesLfar by PG 25.03.2021Ganesh PhadatareNo ratings yet

- AP - Cash in BankDocument4 pagesAP - Cash in BankNorie Jane CaninoNo ratings yet

- Cash Management Business Process Workshop (BPW) : July 2016 Departmental ReleaseDocument48 pagesCash Management Business Process Workshop (BPW) : July 2016 Departmental ReleaseKavitaNo ratings yet

- What Is SOCA?: Demand Accounts Are Accounts Held at Depository InstitutionsDocument5 pagesWhat Is SOCA?: Demand Accounts Are Accounts Held at Depository InstitutionsRahul YadavNo ratings yet

- Accounting Records (Compatibility Mode)Document9 pagesAccounting Records (Compatibility Mode)MahediNo ratings yet

- Bank and Cash 2023 MS SUNLEARNDocument34 pagesBank and Cash 2023 MS SUNLEARNJustyneNo ratings yet

- Afm - PPT M1Document15 pagesAfm - PPT M1Abhishek JainNo ratings yet

- Cash and Securities DepartmentDocument38 pagesCash and Securities DepartmentHAMMADHRNo ratings yet

- FABM 2 - BankDocument58 pagesFABM 2 - Bankmary rose aragonNo ratings yet

- Bank Branch LFAR CA Ketan SaiyaDocument32 pagesBank Branch LFAR CA Ketan SaiyaJovamar MendozaNo ratings yet

- 5708512020book Keeping and Accounting Module - 1Document62 pages5708512020book Keeping and Accounting Module - 1groot marvelNo ratings yet

- Lecture 5 - Books of Accounts and Double Entry SystemDocument7 pagesLecture 5 - Books of Accounts and Double Entry SystemmallarilecarNo ratings yet

- Mgt101-7 - Bank Reconciliation StatementDocument36 pagesMgt101-7 - Bank Reconciliation StatementUmer MateenNo ratings yet

- Compendium of Cash Operations in Currency Chest and Branches 04.07.2020Document242 pagesCompendium of Cash Operations in Currency Chest and Branches 04.07.2020Goutam MalakarNo ratings yet

- Chapter - 5: Deposit ManagementDocument12 pagesChapter - 5: Deposit ManagementEEL KfWBMZ2.1No ratings yet

- BANK Audit Material 15th March 2013Document23 pagesBANK Audit Material 15th March 2013padmanabha14No ratings yet

- Introduction To Introduction To Introduction To Introduction To Monetary Accounts Monetary Accounts YyDocument30 pagesIntroduction To Introduction To Introduction To Introduction To Monetary Accounts Monetary Accounts YyHaris HandyNo ratings yet

- Summary of Measurement, Presentation and DisclosureDocument17 pagesSummary of Measurement, Presentation and DisclosureMelrose Eugenio ErasgaNo ratings yet

- Functions of RBI: Prof. Divya GuptaDocument22 pagesFunctions of RBI: Prof. Divya GuptaNeha SharmaNo ratings yet

- The JournalDocument24 pagesThe JournalKim DianaNo ratings yet

- 1.150 ATP 2023-24 GR 12 Acc FinalDocument4 pages1.150 ATP 2023-24 GR 12 Acc FinalsiyabongaNo ratings yet

- September Montly Rep 2020Document22 pagesSeptember Montly Rep 2020meskerem hailuNo ratings yet

- 11CBSE Chapter 1 Meaning and Objective of AccountingDocument8 pages11CBSE Chapter 1 Meaning and Objective of AccountingSanyam YadavNo ratings yet

- Session 1 Basic Cash ManagementDocument10 pagesSession 1 Basic Cash ManagementManik MehtaNo ratings yet

- Mcs 35 SyllabusDocument3 pagesMcs 35 SyllabusSebastianNo ratings yet

- Class 10-11Document38 pagesClass 10-11Asif HussainNo ratings yet

- Mgt101-11 - Control AccountsDocument52 pagesMgt101-11 - Control AccountsKamran ArshafNo ratings yet

- Monetary PolicyDocument30 pagesMonetary PolicyJoab Dan Valdivia CoriaNo ratings yet

- Manual of Regulations On Foreign Exchange TransactionsDocument95 pagesManual of Regulations On Foreign Exchange TransactionsShane EstNo ratings yet

- Trial Balance and Rectification of Errors: Accountancy 180Document46 pagesTrial Balance and Rectification of Errors: Accountancy 180kofirNo ratings yet

- Trial Balance and Rectification of Errors: Accountancy 180Document46 pagesTrial Balance and Rectification of Errors: Accountancy 180Abhijeet NarangNo ratings yet

- Class 11 Accountancy NCERT Textbook Chapter 6 Trial Balance and Rectification of ErroesDocument51 pagesClass 11 Accountancy NCERT Textbook Chapter 6 Trial Balance and Rectification of ErroesPathan KausarNo ratings yet

- Branch Accounting PDFDocument18 pagesBranch Accounting PDFSivasruthi DhandapaniNo ratings yet

- Branch AccountingDocument39 pagesBranch Accountingbilalyasir100% (5)

- GR 10 Accounting P2 EngDocument26 pagesGR 10 Accounting P2 Engtapiwamakamure2No ratings yet

- Reference:STFM Chapter 1 ETM Chapter 1Document45 pagesReference:STFM Chapter 1 ETM Chapter 1ismayilovrNo ratings yet

- Handout. WCM - Cash ManagementDocument26 pagesHandout. WCM - Cash ManagementNaia SNo ratings yet

- Act1 Cash ReceiptsDocument17 pagesAct1 Cash ReceiptsStephanie Diane SabadoNo ratings yet

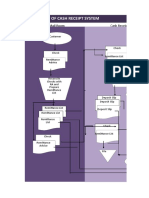

- Flowchart of Cash Receipt System: Mail Room Cash ReceiptsDocument17 pagesFlowchart of Cash Receipt System: Mail Room Cash ReceiptsStephanie Diane SabadoNo ratings yet

- Chapter 9 Accounting For Branches Including Foreign Branches PDFDocument61 pagesChapter 9 Accounting For Branches Including Foreign Branches PDFAkshansh MahajanNo ratings yet

- ACCT1111 Chapter 5 NewDocument47 pagesACCT1111 Chapter 5 NewWky JimNo ratings yet

- De Leon - Interm1 - Module 3 Online Discussion Prompt - Bfac02Document2 pagesDe Leon - Interm1 - Module 3 Online Discussion Prompt - Bfac02Earl De LeonNo ratings yet

- MORFXTDocument95 pagesMORFXTReniel Roquero DiceNo ratings yet

- Long Form Audit Report: Ca Nilesh JoshiDocument33 pagesLong Form Audit Report: Ca Nilesh JoshiCA Faisal VaduvanchalNo ratings yet

- Notes Chapter 6Document2 pagesNotes Chapter 6syafaNo ratings yet

- Internship Report: Company: National Bank of Pakistan Presenter: Rana Muzaffar Iqbal (M-8823)Document34 pagesInternship Report: Company: National Bank of Pakistan Presenter: Rana Muzaffar Iqbal (M-8823)Muzaffar IqbalNo ratings yet

- Treasury Operations in BanksDocument47 pagesTreasury Operations in BanksDuma DumaiNo ratings yet

- Accounts 2 Control Acts PDFDocument14 pagesAccounts 2 Control Acts PDFBaryaNo ratings yet

- Lecture 1 - Concepts and Introduction 4Document63 pagesLecture 1 - Concepts and Introduction 4FarahNo ratings yet

- International Business 15Th Edition Daniels Solutions Manual Full Chapter PDFDocument34 pagesInternational Business 15Th Edition Daniels Solutions Manual Full Chapter PDFthuydieuazfidd100% (9)

- Error Log Inter NoDocument60 pagesError Log Inter NosollyusNo ratings yet

- Bob SsaDocument1 pageBob Ssaranbir9drNo ratings yet

- Poly List April 2020Document17 pagesPoly List April 2020Heber AlvarezNo ratings yet

- Bài tập Unit 3Document9 pagesBài tập Unit 3Thu HàNo ratings yet

- Друштво за маркетинг, трговија и услуги ТАЛЕНТА ДООЕЛ Тетово - OF0032 - 19Document1 pageДруштво за маркетинг, трговија и услуги ТАЛЕНТА ДООЕЛ Тетово - OF0032 - 19Xhevat ZiberiNo ratings yet

- Helios Press Release CAB Payments Lists On The London Stock Exchange - 1Document3 pagesHelios Press Release CAB Payments Lists On The London Stock Exchange - 1b.aggorNo ratings yet

- FECHA: 10/ 06/ 2022: Actívate 1: Write The Following NumbersDocument5 pagesFECHA: 10/ 06/ 2022: Actívate 1: Write The Following Numbersdanna alvarezNo ratings yet

- Forward Rates - June 30 2022Document2 pagesForward Rates - June 30 2022Tiso Blackstar GroupNo ratings yet

- What Is PeercoinDocument2 pagesWhat Is PeercoinlauraNo ratings yet

- Innovative Financial ServicesDocument9 pagesInnovative Financial ServicesShubham GuptaNo ratings yet

- AqEx PitchDeck 20ainDocument25 pagesAqEx PitchDeck 20ainomidreza tabrizianNo ratings yet

- Ultimate List of Important AbbreviationsDocument26 pagesUltimate List of Important Abbreviationsjust cleanNo ratings yet

- Assignment - Exchange Rates 2Document4 pagesAssignment - Exchange Rates 2Praveen Jude CoorayNo ratings yet

- Forex Tester 4 QuickStartGuideDocument151 pagesForex Tester 4 QuickStartGuideempelNo ratings yet

- 1 Case Studies. 2nd SemDocument20 pages1 Case Studies. 2nd SemNeha SinglaNo ratings yet

- The Financial Sector Reforms in IndiaDocument6 pagesThe Financial Sector Reforms in IndiahamidfarahiNo ratings yet

- Pup 20131117 26810Document0 pagesPup 20131117 26810Clark Fabionar SaquingNo ratings yet