You might also like

- Chapter 16Document16 pagesChapter 16soniadhingra1805No ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- ACFrOgDLfhxtIOwMb77mrPSB6zPbwJ nCGMj4u3t nqJm5cxUZU HylVBI0B54-mcxc-rNjgLkEXuSk9WcTCRA-Q5RJl9LL1h4L O7yYO6Yn Gu4bo-k0Dj1aRelUsY PDFDocument23 pagesACFrOgDLfhxtIOwMb77mrPSB6zPbwJ nCGMj4u3t nqJm5cxUZU HylVBI0B54-mcxc-rNjgLkEXuSk9WcTCRA-Q5RJl9LL1h4L O7yYO6Yn Gu4bo-k0Dj1aRelUsY PDFPrashant TodkarNo ratings yet

- Rental Property Investing: A Handbook and Guide for Becoming a Landlord!From EverandRental Property Investing: A Handbook and Guide for Becoming a Landlord!No ratings yet

- Depreciation Methods and AccountingDocument24 pagesDepreciation Methods and Accountingdishydashy88No ratings yet

- DepreciationDocument28 pagesDepreciationREHANRAJNo ratings yet

- Chapter 7 DepDocument18 pagesChapter 7 DepvandhanaNo ratings yet

- DEP1Document13 pagesDEP1MVK SRINIVASA RAONo ratings yet

- Depreciation Provisions and Reserves Class 11 NotesDocument48 pagesDepreciation Provisions and Reserves Class 11 Notesjainayan8190No ratings yet

- Fin 440 Chapter 9Document19 pagesFin 440 Chapter 9Mehedi HasanNo ratings yet

- DepreciationDocument26 pagesDepreciationSHENUNo ratings yet

- Unit 3 Depreciation AccountingDocument38 pagesUnit 3 Depreciation AccountingBharathi RajuNo ratings yet

- Depreciation of Non Current AssetsDocument27 pagesDepreciation of Non Current Assetskimuli FreddieNo ratings yet

- FIN 408 - Ch.8Document18 pagesFIN 408 - Ch.8Shohidul Islam SaykatNo ratings yet

- T.Deva Prasad: GAYATRI Degree & PG CollegeDocument23 pagesT.Deva Prasad: GAYATRI Degree & PG Collegethella deva prasadNo ratings yet

- DepreciationDocument14 pagesDepreciationprjiviNo ratings yet

- Basic Financial AccountingDocument13 pagesBasic Financial Accountingalok beheraNo ratings yet

- Depreciation, Provisions and ReservesDocument27 pagesDepreciation, Provisions and Reservesabhinandbabu314No ratings yet

- Capital Budgeting: Satish SinghDocument21 pagesCapital Budgeting: Satish SinghSatish Singh ॐ100% (1)

- Depreciation 2023-2024 Iisjed Class For 12th Standard CBSEDocument29 pagesDepreciation 2023-2024 Iisjed Class For 12th Standard CBSETaLHa iNaM sameerNo ratings yet

- DepreciationDocument14 pagesDepreciationsujata kumariNo ratings yet

- Accounting Concept: C I D C CDocument9 pagesAccounting Concept: C I D C CRana FahadNo ratings yet

- Theory of DepreciationDocument7 pagesTheory of DepreciationNaman TyagiNo ratings yet

- Abm 1Document7 pagesAbm 1Sachin ManjhiNo ratings yet

- Engineering Economic Lecture 6Document27 pagesEngineering Economic Lecture 6omar meroNo ratings yet

- 03 How To Calculate Present Values-2Document23 pages03 How To Calculate Present Values-2melekkbass10No ratings yet

- DepreciationDocument7 pagesDepreciationSoumendra RoyNo ratings yet

- Methods of DepreciationDocument12 pagesMethods of Depreciationamun din100% (1)

- Chap 014 Capital BudgetingDocument120 pagesChap 014 Capital BudgetingAsere Jazmin100% (1)

- Session 78 - Cashflows of Capital BudgetingDocument32 pagesSession 78 - Cashflows of Capital Budgeting11219203nguyen.nhungNo ratings yet

- DepreciationDocument3 pagesDepreciationvaibhavksingh099No ratings yet

- MODULE 6 Topic 1Document34 pagesMODULE 6 Topic 1Lowie Aldani SantosNo ratings yet

- Depreciation and Provision For DepreciationDocument2 pagesDepreciation and Provision For DepreciationAnsha Twilight14No ratings yet

- Accounting For Managers - 4Document27 pagesAccounting For Managers - 42123 Rohit TiwariNo ratings yet

- DepreciationnnDocument127 pagesDepreciationnnHYDER ALINo ratings yet

- MEFADocument24 pagesMEFASai Teja MadhaNo ratings yet

- Depreciation-AS 6: Typical Problems Areas of Fixed AccountingDocument4 pagesDepreciation-AS 6: Typical Problems Areas of Fixed AccountingRevanth NvNo ratings yet

- Capital BudgetingDocument2 pagesCapital Budgetingmengjun0987654311No ratings yet

- Depreciation: Concept Objectives Causes Depreciation MethodsDocument12 pagesDepreciation: Concept Objectives Causes Depreciation MethodsSachin SahooNo ratings yet

- EEF - Financial Statement - Winter 2021Document26 pagesEEF - Financial Statement - Winter 2021djvdbravoNo ratings yet

- DepreciationDocument2 pagesDepreciationAiswarya HariNo ratings yet

- Depreciation AccountingDocument9 pagesDepreciation Accountingu1909030No ratings yet

- Earnings Quality Microsoft. Jet. RentWayDocument25 pagesEarnings Quality Microsoft. Jet. RentWayDebasis DashNo ratings yet

- Fixed Assets and DepreciationDocument7 pagesFixed Assets and DepreciationArun PeterNo ratings yet

- 01 FM&I Chap 7 Part 2 Stock MKTDocument89 pages01 FM&I Chap 7 Part 2 Stock MKTHoàng Lan AnhNo ratings yet

- EEC Unit5-DepreciationDocument4 pagesEEC Unit5-DepreciationSankara nathNo ratings yet

- Ch-7 Notes and Project WorkDocument7 pagesCh-7 Notes and Project WorksnehasishNo ratings yet

- Accounting o LevelsDocument6 pagesAccounting o LevelsHira KhanNo ratings yet

- Chapter 7 DepreciationDocument50 pagesChapter 7 Depreciationpriyam.200409No ratings yet

- Financial Aspects in Renewable Energy: 2 FEBRUARY 2018Document26 pagesFinancial Aspects in Renewable Energy: 2 FEBRUARY 2018Vrushabh DongeNo ratings yet

- Accounting Concept: Fair Value Matching PrincipleDocument13 pagesAccounting Concept: Fair Value Matching PrincipleJohn ArthurNo ratings yet

- Accountancy 7Document65 pagesAccountancy 7Arif ShaikhNo ratings yet

- BBA-305 Cost & Management AccountingDocument57 pagesBBA-305 Cost & Management Accountingstarkol.c2023112971No ratings yet

- Asset-V1 VIT+BMT1005+2020+type@asset+block@Depreciation-video MaterialDocument44 pagesAsset-V1 VIT+BMT1005+2020+type@asset+block@Depreciation-video MaterialAYUSH GURTU 17BEC0185No ratings yet

- Business Finance Notes-11Document8 pagesBusiness Finance Notes-11Anonymus PershonNo ratings yet

- Accounting For DepreciationDocument31 pagesAccounting For DepreciationImran KhanNo ratings yet

- Capital BudgetingDocument12 pagesCapital Budgetingsunnykumar.m2325No ratings yet

- 4 Elements of FS, Recognition, Measurement and DisclosureDocument34 pages4 Elements of FS, Recognition, Measurement and DisclosureJustin BituaNo ratings yet

- Double Declining Balance Depreciation. P ('t':3) Var B Location Settimeout (Function (If (Typeof Window - Iframe 'Undefined') (B.href B.href ) ), 15000)Document2 pagesDouble Declining Balance Depreciation. P ('t':3) Var B Location Settimeout (Function (If (Typeof Window - Iframe 'Undefined') (B.href B.href ) ), 15000)Johan Mustiko WNo ratings yet

- DemonetisationDocument44 pagesDemonetisationPriya SonuNo ratings yet

- Insurance in Construction Projects CATEGORIES PART IDocument2 pagesInsurance in Construction Projects CATEGORIES PART IAbdul Rahman Sabra100% (2)

- Chapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashDocument35 pagesChapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashEmey CalbayNo ratings yet

- MGT201 Midterm Solved 8 Papers Quisses by Ali KhannDocument74 pagesMGT201 Midterm Solved 8 Papers Quisses by Ali KhannmaryamNo ratings yet

- Accounting 12 Week 10 & 11Document33 pagesAccounting 12 Week 10 & 11cecilia capiliNo ratings yet

- Audit of LiabilitiesDocument12 pagesAudit of LiabilitiesAcier KozukiNo ratings yet

- Bu 270121Document93 pagesBu 270121Abhinav BakhlaNo ratings yet

- Cost Acctg. - HO#4Document3 pagesCost Acctg. - HO#4Erika mae DPNo ratings yet

- Assignment-1: Interpretation of The Financial Statements For Jones Corporation and Smith CorporationDocument8 pagesAssignment-1: Interpretation of The Financial Statements For Jones Corporation and Smith CorporationfatemaNo ratings yet

- Avanse Education Loan For Abroad StudyDocument16 pagesAvanse Education Loan For Abroad StudyGurbani Kaur SuriNo ratings yet

- Project Report FOR 1000 MT Cold Storage: Details of Project Cost and Means of FinanceDocument11 pagesProject Report FOR 1000 MT Cold Storage: Details of Project Cost and Means of FinancePraveenKDNo ratings yet

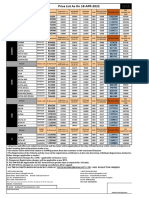

- Price List As On 18-APR-2022: VariantDocument1 pagePrice List As On 18-APR-2022: VariantKolkata Jyote MotorsNo ratings yet

- A Report On The PMC BankDocument8 pagesA Report On The PMC BankSHIKHAR MOHANNo ratings yet

- Custom Account Statement TPR 04!10!2019Document3 pagesCustom Account Statement TPR 04!10!2019sudhir kumar sharmaNo ratings yet

- Stetment 10 PDFDocument4 pagesStetment 10 PDFvaraprasadNo ratings yet

- UnlockedDocument36 pagesUnlockedMayank ShrivastavaNo ratings yet

- AFN Formula Method Answer: A Diff: M 19. Financial Plan Answer: e Diff: M NDocument1 pageAFN Formula Method Answer: A Diff: M 19. Financial Plan Answer: e Diff: M NKaye JavellanaNo ratings yet

- Declaration 3840321246075Document7 pagesDeclaration 3840321246075Qais NasirNo ratings yet

- Fi AssignmentDocument9 pagesFi Assignmentyohannes kindalem0% (1)

- Bab 5 Statement of Financial Position and Statement of Cash Flows (Autosaved)Document99 pagesBab 5 Statement of Financial Position and Statement of Cash Flows (Autosaved)Maha Sarkowi SiranNo ratings yet

- A Research Project On: "A Comparative Study On Financial Performance of 2 Public Sectors Banks (Sbi and Bank of Baroda) "Document39 pagesA Research Project On: "A Comparative Study On Financial Performance of 2 Public Sectors Banks (Sbi and Bank of Baroda) "Daman Deep Singh ArnejaNo ratings yet

- BPI v. CADocument2 pagesBPI v. CAheinnahNo ratings yet

- Chapter 31: Financial Distress: Original Claim Distribution of Liquidating ValueDocument2 pagesChapter 31: Financial Distress: Original Claim Distribution of Liquidating ValueEhsan MohitiNo ratings yet

- Bajaj Allianz General Insurance Company LTDDocument5 pagesBajaj Allianz General Insurance Company LTDUnknownNo ratings yet

- CUET 2023 AccountancyDocument6 pagesCUET 2023 AccountancysubaashahaNo ratings yet

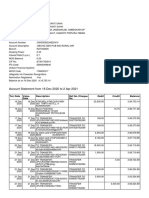

- Account Statement From 16 Dec 2020 To 2 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 16 Dec 2020 To 2 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSuhan SahaNo ratings yet

- Putnam Absolute Return Funds BrochureDocument5 pagesPutnam Absolute Return Funds BrochurePutnam InvestmentsNo ratings yet

- 2024 02 2 15 14 37 Statement - 1706867077138Document29 pages2024 02 2 15 14 37 Statement - 1706867077138Anil NayakNo ratings yet

- Valuation ArgusDocument36 pagesValuation ArgusViraj MehtaNo ratings yet

- Engagement Letter For Accounting Services: TitleDocument1 pageEngagement Letter For Accounting Services: TitleFrancisqueteNo ratings yet