You might also like

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Loan Classfication, Rescheduling, WriteOffDocument21 pagesLoan Classfication, Rescheduling, WriteOffsagortemenosNo ratings yet

- Final Accounts: Manufacturing, Trading and P&L A/cDocument51 pagesFinal Accounts: Manufacturing, Trading and P&L A/cAnit Jacob Philip100% (1)

- FABM 2nd Sem Long QuizzesDocument8 pagesFABM 2nd Sem Long QuizzesJeamie SayotoNo ratings yet

- 1 - Global Talent Management and Global Talent Challenges Strategic OpportunitiesDocument27 pages1 - Global Talent Management and Global Talent Challenges Strategic OpportunitiesSweta SinhaNo ratings yet

- Executive Order No 292 (Books 1-3) AND RA 9492Document18 pagesExecutive Order No 292 (Books 1-3) AND RA 9492June Lester100% (1)

- IPC Rape Laws Research PaperDocument25 pagesIPC Rape Laws Research PaperSwati KishoreNo ratings yet

- Bahasa Inggris Fakultas Hukum Semester 1Document54 pagesBahasa Inggris Fakultas Hukum Semester 1Pandji Purnawarman83% (6)

- FM 415 - Quiz #1Document4 pagesFM 415 - Quiz #1Rose Gwenn VillanuevaNo ratings yet

- Additional Data For The Statements 31052022Document3 pagesAdditional Data For The Statements 31052022wallavilesNo ratings yet

- LS4-7 (3) MARIANO - EditedDocument16 pagesLS4-7 (3) MARIANO - EditedarnelNo ratings yet

- Accounting Slides Income StatmentDocument20 pagesAccounting Slides Income StatmentEdouard Rivet-BonjeanNo ratings yet

- LP - Entrepreneurship Week 16Document9 pagesLP - Entrepreneurship Week 16Romnick SarmientoNo ratings yet

- AccountsDocument12 pagesAccountsKhadeeja ShoukathNo ratings yet

- Left Column For Inner Computation - Right Column For Totals - Peso Sign at The Beginning Amount and at Final Answer TwoDocument6 pagesLeft Column For Inner Computation - Right Column For Totals - Peso Sign at The Beginning Amount and at Final Answer Twoamberle smithNo ratings yet

- Statement of Comprehensive Income: Presentation of Financial StatementsDocument17 pagesStatement of Comprehensive Income: Presentation of Financial StatementsClaire GarciaNo ratings yet

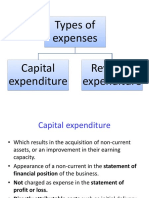

- Types of Expenses Capital Expenditure Revenue ExpenditureDocument8 pagesTypes of Expenses Capital Expenditure Revenue ExpenditureChong Kuan PeiNo ratings yet

- Types of Business According To Activities: Prepared By: Prof. Jonah C. PardilloDocument60 pagesTypes of Business According To Activities: Prepared By: Prof. Jonah C. PardilloShaneil MatulaNo ratings yet

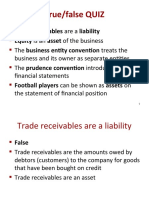

- 11CBSE Chapter 2 Basic Accounting TermDocument11 pages11CBSE Chapter 2 Basic Accounting TermSanyam YadavNo ratings yet

- Week 006 007 Types of Business According To ActivitiesDocument62 pagesWeek 006 007 Types of Business According To ActivitiesKatherine Jane GeronaNo ratings yet

- Income Statement, Further ConsiderationsDocument26 pagesIncome Statement, Further ConsiderationsRashik RayatNo ratings yet

- Chapter 05 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Document196 pagesChapter 05 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Awais Azeemi100% (3)

- Class Notes: Class: XI Topic: Financial StatementDocument3 pagesClass Notes: Class: XI Topic: Financial StatementRajeev ShuklaNo ratings yet

- FABM2-Chapter 2Document31 pagesFABM2-Chapter 2Marjon GarabelNo ratings yet

- Type of Finance OfficeDocument26 pagesType of Finance Officenurul nadiaNo ratings yet

- Income StatementsDocument5 pagesIncome StatementsAdetunbi TolulopeNo ratings yet

- Chapter 3 Inventories and Cost of Goods SoldDocument84 pagesChapter 3 Inventories and Cost of Goods SoldSampanna Shrestha100% (1)

- Discussion Guide - Chapter 5Document7 pagesDiscussion Guide - Chapter 5Khoi NguyenNo ratings yet

- Fabm ReviewerDocument16 pagesFabm Reviewersab lightningNo ratings yet

- 5 6172302118171443573 PDFDocument3 pages5 6172302118171443573 PDFPavan RaiNo ratings yet

- Business Combinations, Goodwill and IntangiblesDocument63 pagesBusiness Combinations, Goodwill and IntangiblesTigist AlemayehuNo ratings yet

- 2 140201115744 Phpapp01Document20 pages2 140201115744 Phpapp01Tannu GuptaNo ratings yet

- Chapter 5 WileyDocument28 pagesChapter 5 Wileyp876468No ratings yet

- Sci Multi StepDocument20 pagesSci Multi StepJoselyn AmonNo ratings yet

- Revise ConceptsDocument9 pagesRevise ConceptsPanther GG YTNo ratings yet

- Acf100 New ImportantDocument10 pagesAcf100 New ImportantNikunjGuptaNo ratings yet

- CH03Document50 pagesCH03Hesly Irawanda NaibahoNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument26 pagesAccounting Cycle of A Merchandising BusinessAngel ManaloNo ratings yet

- Unit 4Document85 pagesUnit 4Ankush Singh100% (1)

- Statement of Comprehensive IncomeDocument33 pagesStatement of Comprehensive IncomeZalvy Gwen RecimoNo ratings yet

- ACCT Midterm 2Document26 pagesACCT Midterm 2Gene'sNo ratings yet

- Week 4 T3 Lectures 7 & 8 Income Statement I With SolutionsDocument59 pagesWeek 4 T3 Lectures 7 & 8 Income Statement I With SolutionsAbdullah HashmatNo ratings yet

- Unit 1 Book Keeping, Accounting, AS & IFRS PDFDocument43 pagesUnit 1 Book Keeping, Accounting, AS & IFRS PDFShreyash PardeshiNo ratings yet

- Final Accounts NotesDocument6 pagesFinal Accounts NotesVinay K TanguturNo ratings yet

- Lesson 19Document45 pagesLesson 19nabila qayyumNo ratings yet

- Accounting 1 Module 5Document15 pagesAccounting 1 Module 5Rose Marie Recorte100% (1)

- Finals - Fina 221Document14 pagesFinals - Fina 221MARITONI MEDALLANo ratings yet

- Statement of Comprehensive IncomeDocument25 pagesStatement of Comprehensive IncomeAngel Nichole ValenciaNo ratings yet

- Chapter # 8: Financial StatementsDocument18 pagesChapter # 8: Financial Statementsfahad BataviaNo ratings yet

- Business FinanceDocument3 pagesBusiness Financesk001No ratings yet

- BAFS Basic ConceptDocument12 pagesBAFS Basic Conceptmilkbear03No ratings yet

- LAS ABM - FABM12 Ic D 7 Week 3Document9 pagesLAS ABM - FABM12 Ic D 7 Week 3ROMMEL RABONo ratings yet

- Capital and Revenue Expenditure and ReceiptsDocument7 pagesCapital and Revenue Expenditure and ReceiptsjamiemangsangNo ratings yet

- AccountingDocument14 pagesAccountingSUNNY SIDE UPNo ratings yet

- Accounting O/A LevelsDocument106 pagesAccounting O/A Levelsmeelas123100% (2)

- Business MathematicsDocument84 pagesBusiness MathematicsChris Tin0% (1)

- Activity 5Document11 pagesActivity 5Ebs DandaNo ratings yet

- 04 Finance On A SheetDocument2 pages04 Finance On A Sheetkacper.wojcieszak08No ratings yet

- The Working CapitalDocument68 pagesThe Working CapitalLalla fakhitaNo ratings yet

- Income Statement 2022Document37 pagesIncome Statement 2022Vinay MehtaNo ratings yet

- Week4 Handout WORKEDDocument14 pagesWeek4 Handout WORKEDLecia Lebby CNo ratings yet

- 8 Capital and RevenueDocument8 pages8 Capital and RevenuePrabhat KharelNo ratings yet

- Minus Sales Returns, Discounts, and Allowances) Minus Cost of SalesDocument7 pagesMinus Sales Returns, Discounts, and Allowances) Minus Cost of Salesclothing shoptalkNo ratings yet

- English Analysing Themes and Ideas Presentation Beige Pink Lined StyleDocument50 pagesEnglish Analysing Themes and Ideas Presentation Beige Pink Lined StyleThryzze Abby ParochaNo ratings yet

- Creative WritingDocument6 pagesCreative WritingThryzze Abby ParochaNo ratings yet

- EntrepDocument5 pagesEntrepThryzze Abby ParochaNo ratings yet

- cOM ENGDocument6 pagescOM ENGThryzze Abby ParochaNo ratings yet

- Barbarism: A User's GuideDocument11 pagesBarbarism: A User's GuideJahir IslamNo ratings yet

- Solar DC CablesDocument3 pagesSolar DC CablesDibyendu MaityNo ratings yet

- Economics DifferencesDocument5 pagesEconomics DifferencesAyappaNo ratings yet

- Cloud Computing NotesDocument21 pagesCloud Computing NotesH117 Survase KrutikaNo ratings yet

- Keith Haring Foundation v. Colored Thumb - ComplaintDocument22 pagesKeith Haring Foundation v. Colored Thumb - ComplaintSarah BursteinNo ratings yet

- Actgfr ch02Document21 pagesActgfr ch02chingNo ratings yet

- Attendance Register Cum PayslipDocument13 pagesAttendance Register Cum PaysliphimanshuNo ratings yet

- Quectel GSM BT Application Note V1.2Document48 pagesQuectel GSM BT Application Note V1.2MaiDungNo ratings yet

- Resume - Olivia KDocument2 pagesResume - Olivia Kapi-438483578No ratings yet

- BackgroundDocument8 pagesBackgroundhey lucy!No ratings yet

- 1 PBDocument6 pages1 PBAkanksha SinghNo ratings yet

- An Essay On The History of Civil Society (1767) - Adam Ferguson FacsDocument476 pagesAn Essay On The History of Civil Society (1767) - Adam Ferguson Facsdp1974100% (1)

- Kahama CVDocument3 pagesKahama CVpcfan church100% (2)

- Security Industry Digital PlanDocument17 pagesSecurity Industry Digital PlanAdrianta WardhanaNo ratings yet

- Chitepo Assasination ReportDocument84 pagesChitepo Assasination ReportPeter GwizoNo ratings yet

- Comparatives and Superlatives PRACTICEDocument1 pageComparatives and Superlatives PRACTICENayeli AraujoNo ratings yet

- One Summer Night: Ambrose BierceDocument7 pagesOne Summer Night: Ambrose Bierce恩洁白No ratings yet

- r220 1Document216 pagesr220 1Mark CheneyNo ratings yet

- Form C3.1 Single Work Permit Change in Employer Application For Recruiting Temping AgentsDocument5 pagesForm C3.1 Single Work Permit Change in Employer Application For Recruiting Temping AgentsPG Venkatesh YadavNo ratings yet

- Modal Verbs: Bill Likes To Show Off. Form Sentences Using The Present PerfectDocument2 pagesModal Verbs: Bill Likes To Show Off. Form Sentences Using The Present PerfectEvaNo ratings yet

- Hurricane Sandy: How The Continuum Hospitals of New York Served The NYC CommunitiesDocument6 pagesHurricane Sandy: How The Continuum Hospitals of New York Served The NYC CommunitiesContinuum Hospitals of New YorkNo ratings yet

- Andhra Pradesh Teacher Eligibility Test (APTET) 2022: Commissioner of School Education, Government of APDocument7 pagesAndhra Pradesh Teacher Eligibility Test (APTET) 2022: Commissioner of School Education, Government of APcrazy crazyNo ratings yet

- AA Eth Energy Sector Presentation LondonDocument24 pagesAA Eth Energy Sector Presentation London654321No ratings yet