You might also like

- Soal Ujian Akhir: Intermediate Financial Management Kelas: Magister Ilmu Management /feb Usu 1Document4 pagesSoal Ujian Akhir: Intermediate Financial Management Kelas: Magister Ilmu Management /feb Usu 1ninaNo ratings yet

- The Keynesian System II Money, Interest, and IncomeDocument28 pagesThe Keynesian System II Money, Interest, and IncomeVenkatesh Venu GopalNo ratings yet

- ISLMDocument4 pagesISLMmapuordominic1No ratings yet

- The Keynesian ModelDocument37 pagesThe Keynesian ModelmahamNo ratings yet

- Module 2 - PPT - 1 - The Classical Macroeconomic Model - Part I PDFDocument15 pagesModule 2 - PPT - 1 - The Classical Macroeconomic Model - Part I PDFChristian Cedrick OlmonNo ratings yet

- Lecture 2Document26 pagesLecture 2PratyushGarewalNo ratings yet

- Is LMDocument21 pagesIs LMtushar kathuria100% (1)

- E435 CCLM s13Document4 pagesE435 CCLM s13Park Seo YoonNo ratings yet

- Is LM Model Class LectureDocument35 pagesIs LM Model Class LectureRamaranjan Chatterjee100% (3)

- The LM Curve With Money TargetingDocument25 pagesThe LM Curve With Money TargetingVeronicaNo ratings yet

- Is LM SummaryDocument16 pagesIs LM SummaryReal LiveNo ratings yet

- IS-LM ModelDocument34 pagesIS-LM ModelAyush AcharyaNo ratings yet

- MacroC4 The Money MarketDocument50 pagesMacroC4 The Money MarketNguyễn Khắc Quý HươngNo ratings yet

- Class PPT On 26th-Feb'21Document4 pagesClass PPT On 26th-Feb'21Kunal PurohitNo ratings yet

- Session 9 Reading 1. This Set of Slides 2. From The Text Material Chapter - 5Document33 pagesSession 9 Reading 1. This Set of Slides 2. From The Text Material Chapter - 5AkshitSoniNo ratings yet

- IS-LM Model of Determination of Interest RatesDocument14 pagesIS-LM Model of Determination of Interest Ratesnamanjain2290No ratings yet

- Macroeconomic Theory ISLMDocument21 pagesMacroeconomic Theory ISLMDhurba KarkiNo ratings yet

- Closed Economy1Document38 pagesClosed Economy1Addai SamuelNo ratings yet

- Macroeconomics 6Document28 pagesMacroeconomics 6Quần hoaNo ratings yet

- Money and Interest Rates: 7.1 Asset Equilibrium, Reviewed 7.2 IS-LM Model 7.3 Price and Aggregate DemandDocument48 pagesMoney and Interest Rates: 7.1 Asset Equilibrium, Reviewed 7.2 IS-LM Model 7.3 Price and Aggregate DemandMara RamosNo ratings yet

- Income Determination Including Money and Interest: The IS - LM ModelDocument21 pagesIncome Determination Including Money and Interest: The IS - LM ModelDixith GandheNo ratings yet

- EC2102 - The Asset MarketDocument41 pagesEC2102 - The Asset MarketsanjeeNo ratings yet

- Chapter 6. Economy in The Short Run: The Is - LM ModelDocument28 pagesChapter 6. Economy in The Short Run: The Is - LM ModelMinh HangNo ratings yet

- S8 The IS-LM ModelDocument32 pagesS8 The IS-LM ModelthreexlmusketeersNo ratings yet

- IS - LM ModelDocument5 pagesIS - LM ModelAbhishek SinhaNo ratings yet

- Macroeconomics 2021/2022: Practice Lesson 1 Prof. Marco Di Domizio EmailDocument10 pagesMacroeconomics 2021/2022: Practice Lesson 1 Prof. Marco Di Domizio EmailghadiNo ratings yet

- IS LM CurveDocument29 pagesIS LM CurveutsavNo ratings yet

- Is LM and General EquilibrimDocument28 pagesIs LM and General EquilibrimBibek Sh Khadgi100% (2)

- 2022 Introduction To Economics Notes 18Document42 pages2022 Introduction To Economics Notes 18Nghia Tuan NghiaNo ratings yet

- S8 The IS-LM ModelDocument35 pagesS8 The IS-LM ModelShrija Majumder BJ22152No ratings yet

- 5is LMDocument30 pages5is LMashutosh patwariyaNo ratings yet

- Introduction To EconomicsDocument7 pagesIntroduction To Economicsapi-15511392No ratings yet

- Is-Lm ModelDocument10 pagesIs-Lm ModelSayam RoyNo ratings yet

- IS-LM ModelDocument78 pagesIS-LM Modelsaty16No ratings yet

- Session 8 & 9 - IsLMDocument30 pagesSession 8 & 9 - IsLMAyusha MakenNo ratings yet

- 5 - The Is-Lm-Fe ModelDocument80 pages5 - The Is-Lm-Fe ModelZenyuiNo ratings yet

- Mundel Flemming Model HardvardDocument13 pagesMundel Flemming Model Hardvarditalos1977No ratings yet

- Monetary Model: Econ302, Fall 2004 Professor Lutz HendricksDocument27 pagesMonetary Model: Econ302, Fall 2004 Professor Lutz HendricksPeter FinzellNo ratings yet

- Meb MergedDocument120 pagesMeb MergedMEHUL PALNo ratings yet

- Is-Lm Model of The Economy 4Document11 pagesIs-Lm Model of The Economy 4Akshay PatilNo ratings yet

- Lec 2 IS - LMDocument42 pagesLec 2 IS - LMDương ThùyNo ratings yet

- American Economic AssociationDocument6 pagesAmerican Economic Associationsimao_sabrosa7794No ratings yet

- MacroeconomicsDocument9 pagesMacroeconomicsAshish ParidaNo ratings yet

- Chapter 11Document17 pagesChapter 11Teak TatteeNo ratings yet

- The Is-Lm Model: ECON 2123: MacroeconomicsDocument56 pagesThe Is-Lm Model: ECON 2123: MacroeconomicskatecwsNo ratings yet

- IS-LM (Macroeconomics)Document11 pagesIS-LM (Macroeconomics)GETinTOthE SySteMNo ratings yet

- Macroeconomics I: Aggregate Demand II: Applying The IS-LM ModelDocument27 pagesMacroeconomics I: Aggregate Demand II: Applying The IS-LM Model우상백No ratings yet

- The Small Open EconomyDocument21 pagesThe Small Open EconomyVrinda ModaNo ratings yet

- Ilovepdf MergedDocument107 pagesIlovepdf MergedMEHUL PALNo ratings yet

- MPP 3Document25 pagesMPP 3Nghaktea J. FanaiNo ratings yet

- C) IS LM ModelDocument19 pagesC) IS LM ModelJeny ChatterjeeNo ratings yet

- Unit 2Document50 pagesUnit 2Astha ParmanandkaNo ratings yet

- Week 6 The is-LM ModelDocument32 pagesWeek 6 The is-LM ModelBiswajit DasNo ratings yet

- TERM 1-Credits 3 (Core) TAPMI, Manipal Session 11: Prof Madhu & Prof RajasulochanaDocument20 pagesTERM 1-Credits 3 (Core) TAPMI, Manipal Session 11: Prof Madhu & Prof RajasulochanaAnonymous cxOemPo3No ratings yet

- Unit 1: Neoclassical Keynesian SynthesisDocument18 pagesUnit 1: Neoclassical Keynesian SynthesisAmanda RuthNo ratings yet

- Chapter 8 - Money Supply & DemandDocument23 pagesChapter 8 - Money Supply & DemandĐỉnh Kout NamNo ratings yet

- Chap 8Document24 pagesChap 8nbh167705No ratings yet

- Solutions Problem Set 1 Macro II (14.452) How Well Does The IS-LM Model Fit Postwar U.S. Data?Document7 pagesSolutions Problem Set 1 Macro II (14.452) How Well Does The IS-LM Model Fit Postwar U.S. Data?m7shahidNo ratings yet

- From Gold Standards to Quantitative Easing A History of Monetary PolicyFrom EverandFrom Gold Standards to Quantitative Easing A History of Monetary PolicyNo ratings yet

- Exercise 2 (2.0 Points) : VJCC Institute Final Term ExamDocument3 pagesExercise 2 (2.0 Points) : VJCC Institute Final Term ExamK59 VU NGOC HIEUNo ratings yet

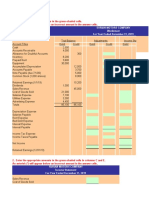

- Income StatementDocument2 pagesIncome StatementelninothekidNo ratings yet

- Acc 115 - P2Document9 pagesAcc 115 - P2Riezel PepitoNo ratings yet

- Assignment 4 What Is MoneyDocument6 pagesAssignment 4 What Is MoneyMuhammad HarisNo ratings yet

- Self PPT On Money and CreditDocument15 pagesSelf PPT On Money and CreditTripti SinghaNo ratings yet

- Algebra For College Students 8th Edition Blitzer Test Bank DownloadDocument94 pagesAlgebra For College Students 8th Edition Blitzer Test Bank DownloadAlan Maxwell100% (23)

- Economics Harbour Notes Part 2 (3) - 201-252Document52 pagesEconomics Harbour Notes Part 2 (3) - 201-252AyushiNo ratings yet

- BBA 207 Exam 2 - Chapters 4, 5 & 6Document6 pagesBBA 207 Exam 2 - Chapters 4, 5 & 6AdrtyNo ratings yet

- 7.29.22 - PM - Loans and Receivables Long TermDocument4 pages7.29.22 - PM - Loans and Receivables Long TermAether SkywardNo ratings yet

- Mishkin Chap 5Document30 pagesMishkin Chap 5Tricia KiethNo ratings yet

- Financial RatioDocument7 pagesFinancial Ratiotimothy454No ratings yet

- Paper11 Syl22 Dec23 Set2 SolDocument16 pagesPaper11 Syl22 Dec23 Set2 Solajithsm39No ratings yet

- University of Tunis Tunis Business SchoolDocument7 pagesUniversity of Tunis Tunis Business Schoolcyrine chahbaniNo ratings yet

- Interest RatesDocument8 pagesInterest RatesThúy LêNo ratings yet

- ECN209 International Finance MidTerm Coursework ExamDocument7 pagesECN209 International Finance MidTerm Coursework Examhunainzia744No ratings yet

- Mini Test 1 2 Autumn 2023 1Document4 pagesMini Test 1 2 Autumn 2023 1aquarius21012003No ratings yet

- Financial Instruments - IPSAS Slides PresentationDocument40 pagesFinancial Instruments - IPSAS Slides PresentationJOHN TUMWEBAZENo ratings yet

- Liquidity Ratios: Working Capital To Total Asset RatioDocument3 pagesLiquidity Ratios: Working Capital To Total Asset RatioBlueBladeNo ratings yet

- Interest Rate Hedging-Examples: Arshad HassanDocument32 pagesInterest Rate Hedging-Examples: Arshad HassanirfanhaidersewagNo ratings yet

- GM Simple and General AnnuityDocument39 pagesGM Simple and General AnnuityKaizel BritosNo ratings yet

- Wahlen Int3e EX03-12Document6 pagesWahlen Int3e EX03-12林義哲No ratings yet

- JPM 1997 409612Document13 pagesJPM 1997 409612lorololloNo ratings yet

- 2B. Corporate Finance: Part 2 Unit 2Document158 pages2B. Corporate Finance: Part 2 Unit 2Karan GoelNo ratings yet

- LN10 EitemanDocument35 pagesLN10 EitemanFong 99No ratings yet

- Mortgage Lab Reflective WritingDocument4 pagesMortgage Lab Reflective Writingapi-345263725No ratings yet

- The Sections of A Tax ReturnDocument2 pagesThe Sections of A Tax ReturnLJBernardoNo ratings yet

- Lecture 13 Money Growth and InflationDocument56 pagesLecture 13 Money Growth and InflationLâm NhiNo ratings yet

- Finman QuizDocument65 pagesFinman QuizChrista LenzNo ratings yet

- Mid Term IFM 2023Document2 pagesMid Term IFM 2023thutrangonedNo ratings yet