You might also like

- The Portable MBA in Finance and AccountingFrom EverandThe Portable MBA in Finance and AccountingRating: 4 out of 5 stars4/5 (19)

- IFRS Guidebook - 2019 Edition (2018, AccountingTools, Inc.) Steven M. BraggDocument508 pagesIFRS Guidebook - 2019 Edition (2018, AccountingTools, Inc.) Steven M. Braggal chemiste100% (7)

- Coursebook Chapter 10 AnswersDocument2 pagesCoursebook Chapter 10 AnswersAhmed Zeeshan100% (4)

- VII. Restaurant Metrics and How To Calculate ThemDocument12 pagesVII. Restaurant Metrics and How To Calculate Themwynlaba100% (1)

- Bookkeeping NC 3 Review GuideDocument6 pagesBookkeeping NC 3 Review GuideCatherine Hidalgo100% (1)

- HBS Mercury CaseDocument4 pagesHBS Mercury CaseDavid Petru100% (1)

- ACCA Financial Management: Topic Area: - Investment Appraisal - Part 1 - Supplementary Notes - Practice QuestionsDocument24 pagesACCA Financial Management: Topic Area: - Investment Appraisal - Part 1 - Supplementary Notes - Practice QuestionsTaariq Abdul-MajeedNo ratings yet

- AAA Accounting Standards Part 1Document3 pagesAAA Accounting Standards Part 1Gauri WastNo ratings yet

- Applied Auditing by CabreraDocument25 pagesApplied Auditing by CabreraClarize R. Mabiog67% (9)

- Audit and Assurance - Real EstateDocument23 pagesAudit and Assurance - Real EstateMary DenizeNo ratings yet

- The Professional CPA Review SchoolDocument24 pagesThe Professional CPA Review SchoolKYLE LEIGHZANDER VICENTENo ratings yet

- Survey of Accounting 5th Edition Edmonds Solutions Manual 1Document86 pagesSurvey of Accounting 5th Edition Edmonds Solutions Manual 1melody100% (48)

- CH 18-Revenue Recognition - KiesoDocument41 pagesCH 18-Revenue Recognition - Kiesofransiskawidya100% (1)

- Business PlanDocument16 pagesBusiness PlanRenalyn De Pedro0% (2)

- Consolidated Mines vs. CTADocument2 pagesConsolidated Mines vs. CTAJam ZaldivarNo ratings yet

- Sample Business Plan - Car HireDocument16 pagesSample Business Plan - Car HireBuali Yahya100% (5)

- Business Combinations: Associate Professor Parmod ChandDocument32 pagesBusiness Combinations: Associate Professor Parmod ChandSunila DeviNo ratings yet

- DividendDocument34 pagesDividendquoteNo ratings yet

- Chap016 Financial Reporting AnalysisDocument15 pagesChap016 Financial Reporting AnalysisThalia SandersNo ratings yet

- Importance of AccountingDocument5 pagesImportance of AccountingPRAJWAL S NNo ratings yet

- Consolidated Financial Statements: Intercompany TransactionsDocument23 pagesConsolidated Financial Statements: Intercompany TransactionsDr-Mohammad Nahawi-Abu AwsNo ratings yet

- Tax and Accounting Aspects of LeasesDocument9 pagesTax and Accounting Aspects of LeasesJulie MarianNo ratings yet

- Section 19Document24 pagesSection 19Abata BageyuNo ratings yet

- Accounting - TheoryDocument33 pagesAccounting - TheoryRashel SheikhNo ratings yet

- Introduction To Managerial AccountingDocument49 pagesIntroduction To Managerial AccountingTreasure's TreasureNo ratings yet

- FA Session 1Document75 pagesFA Session 1keenodiidNo ratings yet

- CH 05Document59 pagesCH 05نوف حميدNo ratings yet

- Survey of Accounting 5Th Edition Edmonds Solutions Manual Full Chapter PDFDocument36 pagesSurvey of Accounting 5Th Edition Edmonds Solutions Manual Full Chapter PDFsusan.ross888100% (11)

- Chapter 3Document23 pagesChapter 3Shevon FortuneNo ratings yet

- Survey of Accounting 4Th Edition Edmonds Solutions Manual Full Chapter PDFDocument36 pagesSurvey of Accounting 4Th Edition Edmonds Solutions Manual Full Chapter PDFsusan.ross888100% (12)

- Survey of Accounting 4th Edition Edmonds Solutions Manual 1Document83 pagesSurvey of Accounting 4th Edition Edmonds Solutions Manual 1louis100% (46)

- PFRS 3, Business CombinationsDocument39 pagesPFRS 3, Business Combinationsjulia4razoNo ratings yet

- Chapter 16 - LeasingDocument20 pagesChapter 16 - LeasingADNAN FAROOQNo ratings yet

- Financial Accounting Theory (Sem V) PDFDocument4 pagesFinancial Accounting Theory (Sem V) PDFHarshal JainNo ratings yet

- Group Accounting - IDocument15 pagesGroup Accounting - ISajid IqbalNo ratings yet

- Topic 4 - Lecture Slides - Part IDocument25 pagesTopic 4 - Lecture Slides - Part INeha LalNo ratings yet

- Topic 1Document49 pagesTopic 1TafadzwaNo ratings yet

- Jawaban Chapter 19Document21 pagesJawaban Chapter 19Stephanie Felicia TiffanyNo ratings yet

- Jawaban Chapter 19Document21 pagesJawaban Chapter 19Stephanie Felicia TiffanyNo ratings yet

- Jawaban Chapter 19Document21 pagesJawaban Chapter 19Stephanie Felicia TiffanyNo ratings yet

- Chapter 6Document49 pagesChapter 6hibongoNo ratings yet

- Objectives of Financial Reporting Objectives of Financial ReportingDocument30 pagesObjectives of Financial Reporting Objectives of Financial ReportingXuuuuuNo ratings yet

- MD SAQUIB KHAN J Management and AccountingDocument25 pagesMD SAQUIB KHAN J Management and AccountingMaths TeacherNo ratings yet

- Financial Reporting 1 BACT 303Document33 pagesFinancial Reporting 1 BACT 303emeraldNo ratings yet

- Lecture 3 (D) Creative AccountingDocument17 pagesLecture 3 (D) Creative AccountingZiyodullo IsroilovNo ratings yet

- Ver1.2Document8 pagesVer1.2Ambrish ChaudharyNo ratings yet

- Lecture 2 and 3 Semester 1Document45 pagesLecture 2 and 3 Semester 1Sara Abdelrahim Makkawi100% (1)

- Reporting Interview GuideDocument7 pagesReporting Interview Guideidrees bajjarNo ratings yet

- Accounting Concepts and ConventionsDocument59 pagesAccounting Concepts and Conventionsiiidddkkk 230No ratings yet

- IFRS 16 - Mepov20Document4 pagesIFRS 16 - Mepov20Ahmed MohamadyNo ratings yet

- The Accounting Treatment of Goodwill: When Will FASB Stop Changing The Rules?Document18 pagesThe Accounting Treatment of Goodwill: When Will FASB Stop Changing The Rules?Hamna AzeezNo ratings yet

- IFRS 16 Impact On Valuations v2 PDFDocument52 pagesIFRS 16 Impact On Valuations v2 PDFLeenin DominguezNo ratings yet

- International Accounting: - Topic: Financial Reporting of JapanDocument6 pagesInternational Accounting: - Topic: Financial Reporting of JapanPrathibha. M PrathiNo ratings yet

- Business CombinationsDocument2 pagesBusiness Combinationsssslll2No ratings yet

- International Accounting: - Topic: Financial Reporting of JapanDocument6 pagesInternational Accounting: - Topic: Financial Reporting of JapanPrathibha. M PrathiNo ratings yet

- Pfrs For Smes - 31aug20118Document6 pagesPfrs For Smes - 31aug20118Joseph II MendozaNo ratings yet

- Goodwill (Accounting) : AccountancyDocument3 pagesGoodwill (Accounting) : AccountancypravilvspNo ratings yet

- Defense Hostile TakeoverDocument12 pagesDefense Hostile TakeoverCookies And CreamNo ratings yet

- Acc Unit-19-AnswersDocument6 pagesAcc Unit-19-AnswersGeorgeNo ratings yet

- IFRS-15 PresentationDocument28 pagesIFRS-15 PresentationNAZNIN SULTANA RININo ratings yet

- Installment SalesDocument2 pagesInstallment SalesMary Joy CruzNo ratings yet

- Installment SalesDocument3 pagesInstallment SalesMary Joy CruzNo ratings yet

- Accounting Principles and Policies: Transaction Relevant PrincipleDocument5 pagesAccounting Principles and Policies: Transaction Relevant PrincipleKenshin HayashiNo ratings yet

- I. 1. Acquisition Method: Non-Controlling Interest Consolidated StatementDocument14 pagesI. 1. Acquisition Method: Non-Controlling Interest Consolidated StatementCookies And CreamNo ratings yet

- Some of The Generally Accepted Accounting Principles (Gaap)Document11 pagesSome of The Generally Accepted Accounting Principles (Gaap)Abdifatah AbdilahiNo ratings yet

- BAW 4614 Advanced Financial Accounting ReportingDocument52 pagesBAW 4614 Advanced Financial Accounting ReportingTEE YAN YING UnknownNo ratings yet

- Module 1A - ACCCOB2 - Introduction To Financial Accounting - FHVDocument25 pagesModule 1A - ACCCOB2 - Introduction To Financial Accounting - FHVCale Robert RascoNo ratings yet

- CPA Financial Accounting and Reporting: Second EditionFrom EverandCPA Financial Accounting and Reporting: Second EditionNo ratings yet

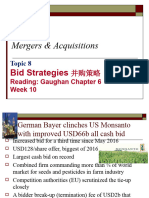

- Bid Strategies (Week 11)Document51 pagesBid Strategies (Week 11)IvanKoNo ratings yet

- Ch03 - Measuring YieldDocument48 pagesCh03 - Measuring YieldIvanKoNo ratings yet

- Takeover Defences (Week 12) SDocument41 pagesTakeover Defences (Week 12) SIvanKoNo ratings yet

- Lecture 5 - Market Misconduct - Discussion ProblemDocument1 pageLecture 5 - Market Misconduct - Discussion ProblemIvanKoNo ratings yet

- Derivatives Finance Lecture 1Document66 pagesDerivatives Finance Lecture 1IvanKoNo ratings yet

- Derivatives Finance Lecture 2Document49 pagesDerivatives Finance Lecture 2IvanKoNo ratings yet

- Week 1 - Overview - Fund Pitching and Business PlanDocument26 pagesWeek 1 - Overview - Fund Pitching and Business PlanIvanKoNo ratings yet

- Godrej GRP Annual ReprtDocument9 pagesGodrej GRP Annual ReprtNandu ReddyNo ratings yet

- Acct 557Document10 pagesAcct 557kihumbaeNo ratings yet

- Practical Accounting 2 Business Combination Lecture NotesDocument2 pagesPractical Accounting 2 Business Combination Lecture NotesPatricia Ann TamposNo ratings yet

- Mark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC02) Paper 01Document19 pagesMark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC02) Paper 01Asma YasinNo ratings yet

- Entrepreneurial FinanceDocument112 pagesEntrepreneurial FinanceJohnny BravoNo ratings yet

- Activity - Chapter 4Document2 pagesActivity - Chapter 4Greta DuqueNo ratings yet

- Employee Benefits Exercises - Pensions and LT BenefitsDocument3 pagesEmployee Benefits Exercises - Pensions and LT BenefitsAcads LangNo ratings yet

- 262-Article Text-719-1-10-20220208Document9 pages262-Article Text-719-1-10-20220208bakerNo ratings yet

- AFARicpaDocument23 pagesAFARicpaRegine YbañezNo ratings yet

- Ia 2 Ppe She 1Document22 pagesIa 2 Ppe She 1AlisonNo ratings yet

- Research 2023Document52 pagesResearch 2023Logo KrdoNo ratings yet

- GAURAV Ratio AnalysisDocument60 pagesGAURAV Ratio AnalysisPoonam KolgeNo ratings yet

- Jaya College of Arts and Science Department of ManagDocument4 pagesJaya College of Arts and Science Department of ManagMythili KarthikeyanNo ratings yet

- ECO111 - Quizze02- NGUYỄN ĐĂNG MẠNHDocument8 pagesECO111 - Quizze02- NGUYỄN ĐĂNG MẠNHMạnh NguyễnNo ratings yet

- Glo-Stick, Inc.: Financial Statement Investigation A02-11-2015Document3 pagesGlo-Stick, Inc.: Financial Statement Investigation A02-11-2015碧莹成No ratings yet

- Final IND AS Summary For Nov 19-CA PS BeniwalDocument15 pagesFinal IND AS Summary For Nov 19-CA PS BeniwalChirag AggarwalNo ratings yet

- BADVAC1X - MOD 6 TemplatesDocument16 pagesBADVAC1X - MOD 6 TemplatesDarius DelacruzNo ratings yet

- Account GPDocument22 pagesAccount GPNurul SyuhadaNo ratings yet

- Chapter 1 Nature of Management Accounting MA vs. FA Macaraeg MarcelinoDocument24 pagesChapter 1 Nature of Management Accounting MA vs. FA Macaraeg MarcelinoJohn BernabeNo ratings yet

- 10-14 InstallmentDocument4 pages10-14 InstallmentMary Ingrid Arellano RabulanNo ratings yet

- QUIZ 6 - Answer 1Document10 pagesQUIZ 6 - Answer 1milbert.degraciaNo ratings yet

- Soal Special Edition Akuntansi Keuangan Menengah IIDocument2 pagesSoal Special Edition Akuntansi Keuangan Menengah IIZephyra ViolettaNo ratings yet