You might also like

- Lecture 4 GE20803 Version 2 - 21stoctober2015 - 1 in 1Document37 pagesLecture 4 GE20803 Version 2 - 21stoctober2015 - 1 in 1syaaismailNo ratings yet

- Sources of Business FinanceDocument17 pagesSources of Business FinanceOM GARGNo ratings yet

- 2017 Mitsubishi Mirage 97704Document6 pages2017 Mitsubishi Mirage 97704Van OpenianoNo ratings yet

- If-1Document27 pagesIf-1Asad MemonNo ratings yet

- BanksDocument16 pagesBanksTHRISHIA ANN SOLIVANo ratings yet

- Islamic Banking: Presented by Lakshmi and ShameemDocument21 pagesIslamic Banking: Presented by Lakshmi and ShameemvidyaposhakNo ratings yet

- Conventional Bank: This Ideal of Economic Bank May Be A Establishment That Accepts DepositsDocument11 pagesConventional Bank: This Ideal of Economic Bank May Be A Establishment That Accepts DepositsRasheed M IsholaNo ratings yet

- Difference and Similarities in Islamic ADocument16 pagesDifference and Similarities in Islamic ASayed Sharif HashimiNo ratings yet

- Presented To:: Islamic FinanceDocument31 pagesPresented To:: Islamic FinanceRizwan Bin RafiqNo ratings yet

- Supporting Shariah Concepts: Shariah Resolutions in Islamic FinanceDocument20 pagesSupporting Shariah Concepts: Shariah Resolutions in Islamic FinanceMohd Afif bin Ab RazakNo ratings yet

- Uib2612 1730 Lecture 3Document32 pagesUib2612 1730 Lecture 3huiminlim0626No ratings yet

- Money and BankingpptDocument19 pagesMoney and BankingpptSania ZaheerNo ratings yet

- Strategic FinanceDocument15 pagesStrategic FinanceSawaira QureshiNo ratings yet

- Difference Between Conventional & Islamic BankingDocument16 pagesDifference Between Conventional & Islamic BankingMuaaz ButtNo ratings yet

- Banking From Islamic Point of ViewDocument6 pagesBanking From Islamic Point of ViewsaadRaulNo ratings yet

- Islamic Banking SolutionDocument8 pagesIslamic Banking SolutionAsad khan100% (1)

- Banking Products and FacilitiesDocument36 pagesBanking Products and FacilitiesMadihah JamianNo ratings yet

- Individual Assignment: 3 Key Products Offered by Islamic Finance Companies/Bank WindowsDocument16 pagesIndividual Assignment: 3 Key Products Offered by Islamic Finance Companies/Bank WindowsNuwan Tharanga LiyanageNo ratings yet

- Pool Management Profit Calculation Distribution Mechanism PDFDocument32 pagesPool Management Profit Calculation Distribution Mechanism PDFMuhammad ZubairNo ratings yet

- PPTDocument27 pagesPPTafeeraNo ratings yet

- Financing CycleDocument4 pagesFinancing CycleYzah CariagaNo ratings yet

- Week 4 Topic 1 Aqad and Sources of FundsDocument41 pagesWeek 4 Topic 1 Aqad and Sources of Funds2 Ashlih Al TsabatNo ratings yet

- An Introduction To Islamic Banking & Finance ProductsDocument15 pagesAn Introduction To Islamic Banking & Finance Productsim_sNo ratings yet

- Bank IslamDocument41 pagesBank Islamaim_nainaNo ratings yet

- BTP - Unit 2Document49 pagesBTP - Unit 2mannnnNo ratings yet

- Conventional Vs Islamic Trade Finance PDF FreeDocument2 pagesConventional Vs Islamic Trade Finance PDF FreeJAS 0313No ratings yet

- Chapter 5Document24 pagesChapter 5Abdiwahab AbdikadirNo ratings yet

- Al-Wadeah Principal and It's Feature Al-Wadeah Principal and It's FeatureDocument8 pagesAl-Wadeah Principal and It's Feature Al-Wadeah Principal and It's Featurevivekananda RoyNo ratings yet

- ASB-i Application Form 100620Document25 pagesASB-i Application Form 100620nur hazwaniNo ratings yet

- Money & Banking PresentationDocument14 pagesMoney & Banking PresentationMuaaz NaeemNo ratings yet

- By Hamad Abdul Aziz: Kuwait Finance HouseDocument23 pagesBy Hamad Abdul Aziz: Kuwait Finance HouseHamad Abdulaziz100% (1)

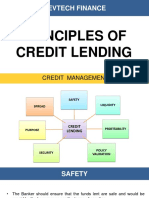

- Principles of Credit LendingDocument10 pagesPrinciples of Credit LendingRa'fat JalladNo ratings yet

- Lecture6 FinancingPart2Document29 pagesLecture6 FinancingPart2Ry NielNo ratings yet

- Lecture5 FinancingPart1Document25 pagesLecture5 FinancingPart1Ry NielNo ratings yet

- Islamic Deposits in PracticeDocument117 pagesIslamic Deposits in PracticeAishiterru Gurl'sNo ratings yet

- Relationship Between Bank & CustomerDocument20 pagesRelationship Between Bank & CustomersafiqulislamNo ratings yet

- Intermediate Accounting NotesDocument7 pagesIntermediate Accounting NotesKyle Angela IlanNo ratings yet

- Islamic Banking and Finance A#5Document6 pagesIslamic Banking and Finance A#5Abdul Wahid KhanNo ratings yet

- Ibria-A Clause in Financial ContractDocument1 pageIbria-A Clause in Financial Contractproffina786No ratings yet

- Final JannaDocument46 pagesFinal JannaLean Syll ValenzuelaNo ratings yet

- Banking ReviewerDocument5 pagesBanking ReviewerBianca MalinabNo ratings yet

- Guideline Ibra' and WaqfDocument24 pagesGuideline Ibra' and WaqfMohammad HanifNo ratings yet

- Savings and InvestmentsDocument30 pagesSavings and InvestmentsLulu BritanniaNo ratings yet

- Introduction To BankingDocument14 pagesIntroduction To Bankingmy automationNo ratings yet

- 05 Islamic Banking - DepositsDocument20 pages05 Islamic Banking - DepositsAmirah ShukriNo ratings yet

- BankingDocument27 pagesBankingObk AkashNo ratings yet

- Islamic Banking and Its Comparison With Conventional Banking Abdullah Al MasudDocument34 pagesIslamic Banking and Its Comparison With Conventional Banking Abdullah Al MasudDevid LuizNo ratings yet

- CH 8.islamic Financial System: DR - Phil.Ninik Sri RahayuDocument19 pagesCH 8.islamic Financial System: DR - Phil.Ninik Sri RahayuCelvin SaputraNo ratings yet

- Deposites Products (Musharakah & Mudarabah)Document27 pagesDeposites Products (Musharakah & Mudarabah)AlHuda Centre of Islamic Banking & Economics (CIBE)No ratings yet

- Bank Baagi HasilDocument33 pagesBank Baagi HasilBahtiar AfandiNo ratings yet

- Difference Between Islamic Banking & Conventional BankingDocument3 pagesDifference Between Islamic Banking & Conventional BankingMuhammad BurhanNo ratings yet

- Bank LendingDocument32 pagesBank LendingFRANCIS JOSEPHNo ratings yet

- Differences Between Conventional Bank and Islamic BankDocument102 pagesDifferences Between Conventional Bank and Islamic Bankmuluneh paulosNo ratings yet

- Loans and Discount FunctionDocument37 pagesLoans and Discount Functionrojon pharmacy80% (5)

- UntitledDocument34 pagesUntitledzamriNo ratings yet

- Difas-2011-Ist-Pr 02-WilsonDocument12 pagesDifas-2011-Ist-Pr 02-WilsonWana MaliNo ratings yet

- Banking and Finance DifferenceDocument4 pagesBanking and Finance DifferenceAyesha HamidNo ratings yet

- Differences Between Conventional Bank and Islamic BankDocument2 pagesDifferences Between Conventional Bank and Islamic BankJerry Khan NiaziNo ratings yet

- Siib - BankingDocument67 pagesSiib - Bankingakashofficial1996No ratings yet

- Closure FormDocument3 pagesClosure FormSriteja JosyulaNo ratings yet

- KKRDocument48 pagesKKRHungreo411100% (1)

- Susmel Foreign Exchange MarketsDocument18 pagesSusmel Foreign Exchange MarketsRAPID M&ENo ratings yet

- Hard AfDocument9 pagesHard AfVincenzo CassanoNo ratings yet

- 604f341e40d3960028590d84 1615803988 ACC 124 - Week 8 9 - ULOcDocument14 pages604f341e40d3960028590d84 1615803988 ACC 124 - Week 8 9 - ULOcFrancine Thea M. LantayaNo ratings yet

- Excel SolverDocument10 pagesExcel SolverSumant SharmaNo ratings yet

- Econ 121 Money and Banking Instructor: Chao WeiDocument3 pagesEcon 121 Money and Banking Instructor: Chao WeiSyed Hassan Raza JafryNo ratings yet

- Acc101 Ia Nguyen Thi Thanh Thuy Hs171230 Mkt1715Document6 pagesAcc101 Ia Nguyen Thi Thanh Thuy Hs171230 Mkt1715Nguyen Thi Thanh ThuyNo ratings yet

- "Dewan Cement": Income Statement 2008 2007 2006 2005 2004Document30 pages"Dewan Cement": Income Statement 2008 2007 2006 2005 2004Asfand Kamal0% (1)

- International FinanceDocument56 pagesInternational FinanceSucheta Das100% (1)

- Case 1 Buffett Report FIN 635Document2 pagesCase 1 Buffett Report FIN 635jack stauberNo ratings yet

- Cash Management WorkbookDocument10 pagesCash Management Workbookanna reham lucmanNo ratings yet

- Consolidated Income Statement or Statement of Profit or Loss and Other Comprehensive IncomeDocument4 pagesConsolidated Income Statement or Statement of Profit or Loss and Other Comprehensive IncomeOmolaja IbukunNo ratings yet

- Tche 303 - Money and Banking Tutorial Assignment 3Document4 pagesTche 303 - Money and Banking Tutorial Assignment 3Tường ThuậtNo ratings yet

- The Determination of Exchange RatesDocument33 pagesThe Determination of Exchange RatesBorn HyperNo ratings yet

- 5-Building A Profit PlanDocument43 pages5-Building A Profit PlanLinh Chi Trịnh T.No ratings yet

- Product Portfolio Analysis BCG Matrix: Julian Grail Jgrail2@glos - Ac.ukDocument11 pagesProduct Portfolio Analysis BCG Matrix: Julian Grail Jgrail2@glos - Ac.ukIshrat JafriNo ratings yet

- A Study On Investor Behaviour Towards Investment Decision With Special Reference To Myfino Payment World (P) LTDDocument31 pagesA Study On Investor Behaviour Towards Investment Decision With Special Reference To Myfino Payment World (P) LTDParameshwari ParamsNo ratings yet

- Work With Financial Planners 1. Enumerate The Three Basic Choices and Managing Your Money and Explain It's Description in Your Own WordDocument2 pagesWork With Financial Planners 1. Enumerate The Three Basic Choices and Managing Your Money and Explain It's Description in Your Own WordRhia shin PasuquinNo ratings yet

- Samsung5 6Document2 pagesSamsung5 6rongrong417No ratings yet

- Introducing The Adaptive Regime Compass: Measuring Equity Market Similarities With ML AlgorithmsDocument18 pagesIntroducing The Adaptive Regime Compass: Measuring Equity Market Similarities With ML AlgorithmsSak GANo ratings yet

- Quiz Valuation Prelim: C. Statement 1 Is False, Statement 2 Is TrueDocument2 pagesQuiz Valuation Prelim: C. Statement 1 Is False, Statement 2 Is TrueUNKNOWNN50% (2)

- 05 Iipm Nota EntrepreneurshipDocument127 pages05 Iipm Nota EntrepreneurshipAMIR HARITH HILMI BIN MOHAMAD HIZAM -No ratings yet

- Ii. Functions: Trust?Document6 pagesIi. Functions: Trust?Jeffrey Garcia IlaganNo ratings yet

- ADVANCED CORPORATE FINANCE Repaper 3rd TermDocument6 pagesADVANCED CORPORATE FINANCE Repaper 3rd TermdixitBhavak DixitNo ratings yet

- Cost Benefit AnalysisDocument22 pagesCost Benefit Analysisricha123456789100% (2)

- Hedge Funds StrategiesDocument13 pagesHedge Funds StrategiesJoel FernandesNo ratings yet

- Pricing of Industrial ProductsDocument8 pagesPricing of Industrial Productsarrowphoto10943438andrewNo ratings yet

- Effect of Basel III On Indian BanksDocument52 pagesEffect of Basel III On Indian BanksSargam Mehta50% (2)

- Corporate Reputation: Image and IdentityDocument15 pagesCorporate Reputation: Image and IdentityInês PereiraNo ratings yet