You might also like

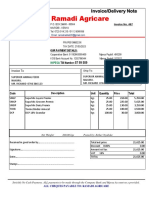

- Ramadi Agricare: Invoice/Delivery NoteDocument2 pagesRamadi Agricare: Invoice/Delivery NoteRamadi cyberNo ratings yet

- Family FoodDocument1 pageFamily FoodSajan Govindhan AcharyNo ratings yet

- Invoices - Cr. Sale - 0396 - VDPM - Lnd2WwHYILjFNlDocument1 pageInvoices - Cr. Sale - 0396 - VDPM - Lnd2WwHYILjFNlAcer UserNo ratings yet

- Aug 2022Document2 pagesAug 2022Nissar da biyaNo ratings yet

- BillDocument1 pageBillSharkya MendezNo ratings yet

- Sugar SolutionDocument54 pagesSugar SolutionAgah GunawanNo ratings yet

- A Unit of Karan Merchant PVT LTD: GSTIN No.: 19AACCK4953B2ZMDocument1 pageA Unit of Karan Merchant PVT LTD: GSTIN No.: 19AACCK4953B2ZMJyoti JainNo ratings yet

- APR NEW-march-april 2023 FinalDocument1 pageAPR NEW-march-april 2023 FinalChembie Mariquit LaderaNo ratings yet

- Fa Assi Sales InvoiceDocument1 pageFa Assi Sales InvoiceTAN YUN YUNNo ratings yet

- RRMMS13221Document2 pagesRRMMS13221mocrossan87No ratings yet

- Tax Invoice and Delivery Note - IN117839Document2 pagesTax Invoice and Delivery Note - IN117839Tatiana DeehNo ratings yet

- KN03Document2 pagesKN03Ramadi cyberNo ratings yet

- Abdullah BrothersDocument2 pagesAbdullah Brothersmycomputer5511No ratings yet

- Invoice Inv-0120Document2 pagesInvoice Inv-0120api-634290901No ratings yet

- Malik Brothers: EstimateDocument1 pageMalik Brothers: EstimateSyed Tasveer AbbasNo ratings yet

- KPM Super Market: Tax InvoiceDocument1 pageKPM Super Market: Tax InvoiceKpm SupermarketNo ratings yet

- KN04 PDFDocument2 pagesKN04 PDFRamadi cyberNo ratings yet

- Description Quantity Rate Value Exc - Stax Sale Tax Amount Value Including Stax UomDocument2 pagesDescription Quantity Rate Value Exc - Stax Sale Tax Amount Value Including Stax Uommati ur rehmanNo ratings yet

- Special Journals - Quiz 36Document8 pagesSpecial Journals - Quiz 36Joana TrinidadNo ratings yet

- 059-Ci Iut Ftpo 01-31 Dec-2022Document1 page059-Ci Iut Ftpo 01-31 Dec-2022sheikh aliNo ratings yet

- Hotel BillDocument1 pageHotel Billjithin shankarNo ratings yet

- Jo 1150Document2 pagesJo 1150Md MonirNo ratings yet

- Driver FinalDocument1 pageDriver Finalamit acharyaNo ratings yet

- Marketing ChecklistDocument3 pagesMarketing ChecklistphilkoyosNo ratings yet

- FoodiezDocument1 pageFoodiezMayank MishraNo ratings yet

- Special Journals - Kathy Concepcion #4 Page287Document9 pagesSpecial Journals - Kathy Concepcion #4 Page287Joana Trinidad100% (3)

- Sop Cleaning Service BaruDocument2 pagesSop Cleaning Service BaruRSUD AnugerahNo ratings yet

- Es 19 277700 PDFDocument1 pageEs 19 277700 PDFTatenda MusesengwaNo ratings yet

- Invoice: Patokan Ilham Mamben LaukDocument7 pagesInvoice: Patokan Ilham Mamben LaukPahkumah Alimah OceNo ratings yet

- APP2016 3rdsup ProvinceCompostelaValleyDocument114 pagesAPP2016 3rdsup ProvinceCompostelaValleyDede R KurniawanNo ratings yet

- JANUARI 2015: PT Maju Sarana Sport Cash Receipt JournalDocument39 pagesJANUARI 2015: PT Maju Sarana Sport Cash Receipt JournalAsna AzyyatiNo ratings yet

- Jawaban CV Roti Jaya Belajar 16 Februari 2023Document62 pagesJawaban CV Roti Jaya Belajar 16 Februari 2023Annisa fitri AnggrainiNo ratings yet

- Invoice Cum Delivery ChallanDocument2 pagesInvoice Cum Delivery Challansatyanarayana amruthamNo ratings yet

- Business ProjectionsDocument10 pagesBusiness ProjectionsNimrod MainaNo ratings yet

- BROILERSDocument2 pagesBROILERSthatolicious49No ratings yet

- Aoutul Trade International: Distribution Center Motalib Plaza, 1st Floor, Hatirpool, Dhaka-1205Document1 pageAoutul Trade International: Distribution Center Motalib Plaza, 1st Floor, Hatirpool, Dhaka-1205Muntasir Al MamunNo ratings yet

- Ramez International Trading: ApprovedDocument2 pagesRamez International Trading: ApprovedIzzathNo ratings yet

- Latihan MikroDocument12 pagesLatihan MikroSunny AimezahraNo ratings yet

- Tesz Esquillo TO47 PHP4450.00Document2 pagesTesz Esquillo TO47 PHP4450.00Elaisa OnerjajNo ratings yet

- Invoice 10120 Karet PDFDocument2 pagesInvoice 10120 Karet PDFM Naufal FawwazNo ratings yet

- Petty Cash-17-03Document2 pagesPetty Cash-17-03lbc.secNo ratings yet

- Sales QuotationDocument2 pagesSales Quotationjayeshgupta423No ratings yet

- Shemu PLC.: Edible Oil Manufacturing Sales ReportDocument9 pagesShemu PLC.: Edible Oil Manufacturing Sales ReportShemu PlcNo ratings yet

- Lembar Kerja Yuana UnsDocument68 pagesLembar Kerja Yuana UnsYuana Umi Nanda SasmitaNo ratings yet

- AR Invoice - Draft - 299040 - 20230724 - 102803Document1 pageAR Invoice - Draft - 299040 - 20230724 - 102803Lloyd JoromanNo ratings yet

- PAA - Special JournalsDocument3 pagesPAA - Special JournalsDanica Shane EscobidalNo ratings yet

- Brothers Store Statement of AccountDocument7 pagesBrothers Store Statement of AccountanwarNo ratings yet

- Rekap Bon Belanja SeptemberDocument6 pagesRekap Bon Belanja Septemberesty ameliaNo ratings yet

- Devis OulmesDocument1 pageDevis Oulmeschahidi.mouradNo ratings yet

- ESTOQUEDocument4 pagesESTOQUEAldair SilvaNo ratings yet

- GST No: 001685676032Document1 pageGST No: 001685676032Peen nam LIMNo ratings yet

- Reg CasaDocument5 pagesReg CasaCRISTIAN MARIAN MARTALOGNo ratings yet

- W5G8939759Document3 pagesW5G8939759gautamsh098100% (1)

- 059 CiDocument2 pages059 Cisheikh aliNo ratings yet

- Report PDFDocument1 pageReport PDFNadia Abu SamahNo ratings yet

- Billing StatementDocument1 pageBilling StatementFrengieBotoyNo ratings yet

- Kunci Jawab Sesi 1 - Bateeq CanteqDocument11 pagesKunci Jawab Sesi 1 - Bateeq CanteqSuara HatiKitaNo ratings yet

- Form 47Document2 pagesForm 47Madhan MohanNo ratings yet

- Case StudyDocument5 pagesCase StudynanthamkNo ratings yet

- Lesson 1 AP: Minimum Composition of The SFP and Some Audit NotesDocument14 pagesLesson 1 AP: Minimum Composition of The SFP and Some Audit NotesDebs FanogaNo ratings yet

- AFAR PreweekDocument8 pagesAFAR PreweekChristian Arthur VelascoNo ratings yet

- Instructions For A Cash Flows Statement Direct MethodDocument5 pagesInstructions For A Cash Flows Statement Direct MethodMary100% (8)

- Adjusting Journal EntriesDocument8 pagesAdjusting Journal EntriesChaaaNo ratings yet

- Posting, Adjusting Entries, Process of Doing A 10-Columnar Worksheets, Closing Entries For Service Type of BusinessDocument18 pagesPosting, Adjusting Entries, Process of Doing A 10-Columnar Worksheets, Closing Entries For Service Type of BusinessRalphjoseph Tuazon100% (1)

- Revenue Recognition Red Flags: Revenue After Cash CollectionDocument7 pagesRevenue Recognition Red Flags: Revenue After Cash CollectionCamilla JIANGNo ratings yet

- Chapter V Audit Prepaid ExpenseDocument4 pagesChapter V Audit Prepaid ExpenseHanju DanielNo ratings yet

- Examination Question and Answers, Set G (Problem Solving), Chapter 15 - Statement of Cash FlowDocument2 pagesExamination Question and Answers, Set G (Problem Solving), Chapter 15 - Statement of Cash Flowjohn carlos doringoNo ratings yet

- Accounting ProcessDocument3 pagesAccounting ProcessAngel RosalesNo ratings yet

- Customization Operations Cost Information Toperform Each of These Functions. Aparticular PurposeDocument4 pagesCustomization Operations Cost Information Toperform Each of These Functions. Aparticular PurposeNalynCasNo ratings yet

- Adjusting Accounts For Financial Statements: Wild and Shaw Fundamental Accounting Principles 24th EditionDocument61 pagesAdjusting Accounts For Financial Statements: Wild and Shaw Fundamental Accounting Principles 24th EditionAudrey BienNo ratings yet

- Northern Cpa Review: First Pre-Board ExaminationDocument13 pagesNorthern Cpa Review: First Pre-Board ExaminationKim Cristian MaañoNo ratings yet

- Balance Sheet StartUpDocument1 pageBalance Sheet StartUpHercule P OirotNo ratings yet

- FR Pipfa Paper CompleteDocument20 pagesFR Pipfa Paper CompleteGENIUS15070% (1)

- Report On Marvel's Restructuring Dilemma: Financial ManagementDocument19 pagesReport On Marvel's Restructuring Dilemma: Financial Managementebi ayatNo ratings yet

- Saskatchewan Roughriders Annual Report 2009-2010Document36 pagesSaskatchewan Roughriders Annual Report 2009-2010Mike SmithNo ratings yet

- Financial Statement Model For The Clorox Company: Company Name Latest Fiscal YearDocument10 pagesFinancial Statement Model For The Clorox Company: Company Name Latest Fiscal YearArslan HafeezNo ratings yet

- 4.2 Financial Statement Basics Exercises1Document24 pages4.2 Financial Statement Basics Exercises1Carlos Vincent OliverosNo ratings yet

- Financial Accounting & AnalysisDocument4 pagesFinancial Accounting & AnalysisAakash agrawalNo ratings yet

- Chapter 11 Adjusting EntriesDocument91 pagesChapter 11 Adjusting EntriesMelessa Pescador100% (1)

- Fundamentals of Accountancy, Business, and Management 1: Types of Major AccountsDocument4 pagesFundamentals of Accountancy, Business, and Management 1: Types of Major AccountsGraciously ElleNo ratings yet

- The Accounting Cycle: Accruals and DeferralsDocument68 pagesThe Accounting Cycle: Accruals and DeferralsLama KaedbeyNo ratings yet

- Statement of Cash FlowsDocument30 pagesStatement of Cash FlowsNocturnal Bee100% (1)

- Notes in Auditing Problems - Correction of ErrorsDocument3 pagesNotes in Auditing Problems - Correction of ErrorsNiño Jemerald TriaNo ratings yet

- ACCT1002 Assignment 3B 2nd S 2021-2022Document16 pagesACCT1002 Assignment 3B 2nd S 2021-2022Zenika PetersNo ratings yet

- Ncert Solution Class 11 Accountancy Chapter 10Document68 pagesNcert Solution Class 11 Accountancy Chapter 10Prakal 444No ratings yet

- India Business QuizDocument10 pagesIndia Business QuizDeep Patel100% (1)

- Soal Cash FlowDocument6 pagesSoal Cash FlowSantiNo ratings yet