You might also like

- Chapter 2 - ManufacturingDocument10 pagesChapter 2 - ManufacturingSyed Zohaib WarisNo ratings yet

- Accounts for Manufacturing FirmsDocument17 pagesAccounts for Manufacturing FirmsZegera Mgendi100% (2)

- Pengelompokan BiayaDocument17 pagesPengelompokan BiayaMaya BangunNo ratings yet

- Assignment2 CostACC VanessaDocument7 pagesAssignment2 CostACC VanessaVanessa vnssNo ratings yet

- Illustration Questions 7Document3 pagesIllustration Questions 7mohammedahalys100% (1)

- Cost accounting introductionDocument5 pagesCost accounting introductionDaniel Jackson100% (1)

- ACC104 - Job Order Costing - For PostingDocument22 pagesACC104 - Job Order Costing - For PostingYesha SibayanNo ratings yet

- Manufacturing Accounts 2020-2 PDFDocument15 pagesManufacturing Accounts 2020-2 PDFAlvin K. JohnsonNo ratings yet

- ACCY112 Tut1 WIN 2022Document20 pagesACCY112 Tut1 WIN 2022Laiba RazaNo ratings yet

- CH - 3 Cost AccountingDocument23 pagesCH - 3 Cost AccountingKhushali OzaNo ratings yet

- Week 5 NotesDocument9 pagesWeek 5 NotescalebNo ratings yet

- Chapter 2: Cost Management Concepts: Jayadevm@iimb - Ernet.inDocument20 pagesChapter 2: Cost Management Concepts: Jayadevm@iimb - Ernet.inPratyush GoelNo ratings yet

- TUTORIAL Manufacturing With SolutionDocument10 pagesTUTORIAL Manufacturing With SolutionmaiNo ratings yet

- P1 Question Bank - CH 1 and 2Document29 pagesP1 Question Bank - CH 1 and 2prudencemaake120No ratings yet

- Unit Costing and Cost SheetDocument15 pagesUnit Costing and Cost SheetAyush100% (1)

- MANAGEMENT ACCOUNTING ASSIGNMENTDocument7 pagesMANAGEMENT ACCOUNTING ASSIGNMENTmuhammad Ammar Shamshad100% (2)

- Chapter 02 Review QuestionsDocument4 pagesChapter 02 Review QuestionsjosemanuelNo ratings yet

- Group AssignmentDocument7 pagesGroup Assignmentsaidkhatib368No ratings yet

- Product CostDocument10 pagesProduct CostApple BaldemoroNo ratings yet

- Hassan Exame 21 AugustrDocument4 pagesHassan Exame 21 Augustrsardar hussainNo ratings yet

- ACT202 - Assignment 2 - 18204001 - Mohammed RashedDocument6 pagesACT202 - Assignment 2 - 18204001 - Mohammed RashedAnkur SahaNo ratings yet

- ManAc Quiz 1Document12 pagesManAc Quiz 1random122No ratings yet

- Problem Set 1 PDFDocument3 pagesProblem Set 1 PDFrenjith0% (2)

- Manufacturing Account (With Answers) : Advanced LevelDocument15 pagesManufacturing Account (With Answers) : Advanced LevelMomoh Kebiru0% (1)

- San Ysidro Company Financial Statements for Year Ending December 31Document10 pagesSan Ysidro Company Financial Statements for Year Ending December 31Natanael SiraitNo ratings yet

- ACMA Unit 7 Problems - Cost Sheet PDFDocument3 pagesACMA Unit 7 Problems - Cost Sheet PDFPrabhat SinghNo ratings yet

- Chapter 20Document13 pagesChapter 20Nguyên BảoNo ratings yet

- Manufacturing A LevelDocument21 pagesManufacturing A LevelSheraz AhmadNo ratings yet

- Handout No. 2Document4 pagesHandout No. 2Gertim CondezNo ratings yet

- Manufacturing AccountDocument5 pagesManufacturing Account27h4fbvsy8No ratings yet

- AccountsDocument14 pagesAccountsgokulamaromal2001No ratings yet

- Excel Task 1 - MoriarityDocument3 pagesExcel Task 1 - MoriarityMihnea SerbanoiuNo ratings yet

- Cost Sheet For The Month of January: TotalDocument9 pagesCost Sheet For The Month of January: TotalgauravpalgarimapalNo ratings yet

- Manufacturing AccountsDocument12 pagesManufacturing AccountsAdrian RamsundarNo ratings yet

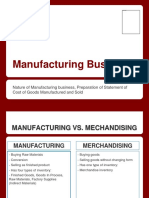

- Manufacturing BusinessDocument18 pagesManufacturing BusinessJeon JeonNo ratings yet

- Cost Sheet BAFDocument16 pagesCost Sheet BAFShaji KuttyNo ratings yet

- Throughput Accounting: Prepared by Gwizu KDocument26 pagesThroughput Accounting: Prepared by Gwizu KTapiwa Tbone Madamombe100% (1)

- 2a. Job Order Costing CRDocument17 pages2a. Job Order Costing CRAnaly Omandac PelayoNo ratings yet

- Chapter 1 - Manufacturing Account (I)Document16 pagesChapter 1 - Manufacturing Account (I)NG JIA LUNGNo ratings yet

- Management Accounting Cost Sheet AnalysisDocument3 pagesManagement Accounting Cost Sheet AnalysisRachit SrivastavaNo ratings yet

- Assignment 3Document5 pagesAssignment 3AIENNA GABRIELLE FABRONo ratings yet

- Managerial Accounting Practice ProblemsDocument20 pagesManagerial Accounting Practice ProblemsAyrton BenavidesNo ratings yet

- Cost Sheet: Dr. Shubhendu VimalDocument9 pagesCost Sheet: Dr. Shubhendu VimalSnehil KrNo ratings yet

- Revision Week 1. Questions. Question 1. Cost of Goods Manufactured, Cost of Goods Sold, Income Statement. (A)Document5 pagesRevision Week 1. Questions. Question 1. Cost of Goods Manufactured, Cost of Goods Sold, Income Statement. (A)Sujib BarmanNo ratings yet

- CH-1 Cost SheetDocument6 pagesCH-1 Cost SheetIftekhar Uddin M.D EisaNo ratings yet

- Cost Sheet ProblemsDocument11 pagesCost Sheet ProblemsPrem RajNo ratings yet

- Normal Costing ProblemsDocument3 pagesNormal Costing Problemsrose llar67% (3)

- Cost of Good Manufactured and Sold StatementDocument8 pagesCost of Good Manufactured and Sold StatementAyesha JavedNo ratings yet

- COST ACCOUNTING ASSIGNMENTDocument6 pagesCOST ACCOUNTING ASSIGNMENTSugata SNo ratings yet

- Manufacturing Account NotesDocument7 pagesManufacturing Account Notesdayna davisNo ratings yet

- MGT Accounting, Intermideiate-SolutionsDocument31 pagesMGT Accounting, Intermideiate-SolutionsRONALD SSEKYANZINo ratings yet

- Add Beginning Work-In-Process Inventory, January 1, 2014 Deduct Ending Work-In-Process Inventory, December31,2014Document1 pageAdd Beginning Work-In-Process Inventory, January 1, 2014 Deduct Ending Work-In-Process Inventory, December31,201415Nety UtamiNo ratings yet

- Chapter 2 - 1 - IllustrationDocument6 pagesChapter 2 - 1 - IllustrationYonas BamlakuNo ratings yet

- Cost Accounting MidDocument7 pagesCost Accounting MidHuma NadeemNo ratings yet

- Varnish Company Cost AnalysisDocument4 pagesVarnish Company Cost AnalysisAmiee Laa PulokNo ratings yet

- Introduction to Manufacturing Costs and Financial StatementsDocument4 pagesIntroduction to Manufacturing Costs and Financial StatementsAshitero YoNo ratings yet

- Commercial & Service Industry Machinery, Miscellaneous World Summary: Market Values & Financials by CountryFrom EverandCommercial & Service Industry Machinery, Miscellaneous World Summary: Market Values & Financials by CountryNo ratings yet

- Engineering Service Revenues World Summary: Market Values & Financials by CountryFrom EverandEngineering Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Computer Integrated Manufacturing: A Total Company Competitive StrategyFrom EverandComputer Integrated Manufacturing: A Total Company Competitive StrategyRating: 2 out of 5 stars2/5 (1)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- SITARAM JINDAL FOUNDATION DONATION APPLICATIONDocument2 pagesSITARAM JINDAL FOUNDATION DONATION APPLICATIONRs WsNo ratings yet

- Shreya Acc MCQDocument34 pagesShreya Acc MCQSHREYA S 200526No ratings yet

- Internship Report SampleDocument53 pagesInternship Report SampleKamruzzaman FahimNo ratings yet

- Darkside of The Pools ReportDocument41 pagesDarkside of The Pools ReportdatasetNo ratings yet

- Workshop 1. Bill of LadingDocument10 pagesWorkshop 1. Bill of LadingAbraham PerezNo ratings yet

- Building Trust in the WorkplaceDocument4 pagesBuilding Trust in the WorkplaceCrinaNo ratings yet

- Investments in Debt and Equity Securities Chapter Multiple Choice QuestionsDocument41 pagesInvestments in Debt and Equity Securities Chapter Multiple Choice QuestionsMonica Monica0% (1)

- SRI5307 st20213548Document36 pagesSRI5307 st20213548Sandani NilekaNo ratings yet

- Human Resource Management Research Paper PDFDocument5 pagesHuman Resource Management Research Paper PDFqqcxbtbndNo ratings yet

- Inventory VoucherDocument2 pagesInventory VoucherPAWAN KUMARNo ratings yet

- 537-2 DiffDocument43 pages537-2 DiffMohammad HassanNo ratings yet

- Simple bookkeeping for beauty parlor businessDocument9 pagesSimple bookkeeping for beauty parlor businessKaye Ann AbinalNo ratings yet

- 0005 - 007 SAFETY RECOGNITION AND INCENTIVE PROGRAMS (SRIPs)Document5 pages0005 - 007 SAFETY RECOGNITION AND INCENTIVE PROGRAMS (SRIPs)baseet gazaliNo ratings yet

- Applications Invited For Stratup Agri-Business IncubationDocument11 pagesApplications Invited For Stratup Agri-Business IncubationAjey Kulkarni100% (1)

- Internship ReportDocument42 pagesInternship ReportAnanya BehlNo ratings yet

- How Much Do Professionals Earn InfographicDocument4 pagesHow Much Do Professionals Earn InfographicAneeqahNo ratings yet

- Makalah B.inggrisDocument15 pagesMakalah B.inggrisMuhammadnur AzizNo ratings yet

- E CommersDocument37 pagesE CommersB GANESH RaoNo ratings yet

- Chapter 1 WPS OfficeDocument7 pagesChapter 1 WPS OfficeOmelkhair YahyaNo ratings yet

- Salary Tax - Sonali SecuritiesDocument19 pagesSalary Tax - Sonali Securitieslimon islamNo ratings yet

- CII IGBC Dossier On 5 Billion SQ - FT of Green Building Footprint PDFDocument52 pagesCII IGBC Dossier On 5 Billion SQ - FT of Green Building Footprint PDFRamaiah KumarNo ratings yet

- Expo Marketing.Document10 pagesExpo Marketing.Kent ForceNo ratings yet

- Types of Price DiscountsDocument53 pagesTypes of Price DiscountsAmit RajNo ratings yet

- Tax Planning and ManagementDocument12 pagesTax Planning and ManagementPalash BairagiNo ratings yet

- Chapter 7: Introduction To Regular Income Tax: 1. General in CoverageDocument19 pagesChapter 7: Introduction To Regular Income Tax: 1. General in CoverageJulie Mae Caling Malit33% (3)

- Financial Analysis and Business Valuation of Viet-Y SteelDocument6 pagesFinancial Analysis and Business Valuation of Viet-Y SteelsenNo ratings yet

- Danh Sách 252 Giám Đốc C: Họ Và Tên Địa Chỉ EmailDocument25 pagesDanh Sách 252 Giám Đốc C: Họ Và Tên Địa Chỉ EmailĐược NguyễnNo ratings yet

- The New B2B Marketing Playbook: Executive SummaryDocument11 pagesThe New B2B Marketing Playbook: Executive Summaryaggold616No ratings yet

- Nabin SharmaDocument4 pagesNabin SharmaAfsar AbdulNo ratings yet

- Harbeck Responds To Letter From Cong. GarrettDocument28 pagesHarbeck Responds To Letter From Cong. GarrettIlene KentNo ratings yet