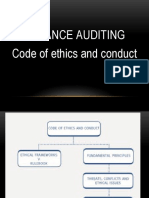

MOD007 Code of Ethics For Professional Accountants

MOD007 Code of Ethics For Professional Accountants

You might also like

- 533-Ethics QuizDocument8 pages533-Ethics Quizapi-562856559100% (1)

- Chapter Three: Professional Ethics and Legal Liability of AuditorsDocument35 pagesChapter Three: Professional Ethics and Legal Liability of Auditorseferem100% (1)

- Mas Practice Standards and Ethical ConsiderationsACDocument3 pagesMas Practice Standards and Ethical ConsiderationsACLorenz BaguioNo ratings yet

- Mas Practice Standards and EthicalconsiderationsDocument6 pagesMas Practice Standards and EthicalconsiderationsRolanElumbreNo ratings yet

- Code of Ethics: FOR Professional AccountantsDocument42 pagesCode of Ethics: FOR Professional AccountantsTracy Marsh RapanutNo ratings yet

- Code of Ethics For Professional AccountantsDocument17 pagesCode of Ethics For Professional AccountantsJay Mark AbellarNo ratings yet

- Advanced Auditing Chapter ThreeDocument49 pagesAdvanced Auditing Chapter ThreemirogNo ratings yet

- Code of Ethics Updated PDFDocument130 pagesCode of Ethics Updated PDFSalvador BrionesNo ratings yet

- Chapter 4 Audit f8 - 2.3Document43 pagesChapter 4 Audit f8 - 2.3JosephineMicheal17No ratings yet

- Code of EthicsDocument5 pagesCode of EthicsAira Shynne AsperaNo ratings yet

- 03.2 Handbook of The International Code of Ethics For Professional AccountantsDocument92 pages03.2 Handbook of The International Code of Ethics For Professional AccountantsnuggsNo ratings yet

- Code of Ethics For Ba II.Document25 pagesCode of Ethics For Ba II.beatricenyashiruNo ratings yet

- Code of EthicsDocument78 pagesCode of EthicsNeriza PonceNo ratings yet

- Code of Ethics - EditedDocument76 pagesCode of Ethics - EditedAaron Mañacap100% (1)

- Professional EthicsDocument4 pagesProfessional EthicsCameille SalmonNo ratings yet

- 2.0 Ethical Concerns For Accountants Mike MbayaDocument38 pages2.0 Ethical Concerns For Accountants Mike MbayaREJAY89No ratings yet

- Code of Ethics For Professional Accountants HandoutDocument25 pagesCode of Ethics For Professional Accountants Handoutsaidkhatib368No ratings yet

- AA - 2023 11 Professional EthicsDocument13 pagesAA - 2023 11 Professional EthicstahreemNo ratings yet

- AA - Spring 2021 11 Professional EthicsDocument13 pagesAA - Spring 2021 11 Professional EthicsSarim AhmadNo ratings yet

- Additional Ethics SlidesDocument5 pagesAdditional Ethics Slidesathirah jamaludinNo ratings yet

- Week 2 Professional ConductDocument31 pagesWeek 2 Professional Conductptnyagortey91No ratings yet

- 1) Code of Ethics For AuditorsDocument29 pages1) Code of Ethics For Auditorsrajes wari50% (2)

- Chapter 2Document21 pagesChapter 2Danish NabilNo ratings yet

- MAS 4 TOPIC 1 Threats and Safeguards in The Practice of Accountancy (Reviewer)Document18 pagesMAS 4 TOPIC 1 Threats and Safeguards in The Practice of Accountancy (Reviewer)vintmyoNo ratings yet

- Code of Professional EthicsDocument42 pagesCode of Professional EthicsMariella CatacutanNo ratings yet

- Slides - Lecture 2 - ST VersionDocument17 pagesSlides - Lecture 2 - ST VersionNguyễn Thu UyênNo ratings yet

- Topic 2 The Role of Professional AccountantDocument27 pagesTopic 2 The Role of Professional AccountantYanPing AngNo ratings yet

- Topic 2 MIA by LawDocument32 pagesTopic 2 MIA by LawNUR IMAN SHAHIDAH BINTI SHAHRUL RIZALNo ratings yet

- Professional Duty of AccountantDocument14 pagesProfessional Duty of AccountantTiya AmuNo ratings yet

- Audit 2: Puan Roslina Binti IdrisDocument12 pagesAudit 2: Puan Roslina Binti Idrishakim azmiNo ratings yet

- At.1304 - Code of EthicsDocument29 pagesAt.1304 - Code of EthicsSheila Mae PlanciaNo ratings yet

- Chapter 13 Codes of Professional EthicsDocument26 pagesChapter 13 Codes of Professional EthicslnghiilwamoNo ratings yet

- 08 JournalDocument6 pages08 Journalits me keiNo ratings yet

- 6-Professional EthicsDocument26 pages6-Professional EthicsQila HusinNo ratings yet

- Code of Ethics: Prof. Zeus A. Aboy, CPA MBA EDL (Candidate)Document75 pagesCode of Ethics: Prof. Zeus A. Aboy, CPA MBA EDL (Candidate)Io AyaNo ratings yet

- Code of EthicsDocument35 pagesCode of EthicsJamsankin PersianNo ratings yet

- UntitledDocument14 pagesUntitledEllieNo ratings yet

- Business Ethics Part 2Document23 pagesBusiness Ethics Part 2Gilner PomarNo ratings yet

- Audit I-Chapter TwoDocument11 pagesAudit I-Chapter Twothedalesh weldeNo ratings yet

- Code of Ethics of Professional AccountantsDocument3 pagesCode of Ethics of Professional AccountantsYamateNo ratings yet

- Auditors Independence Review - 1Document22 pagesAuditors Independence Review - 1Mohammad Abu Kawsar FcaNo ratings yet

- 02 - Code of Ethics of ProfessionalDocument22 pages02 - Code of Ethics of ProfessionalYamateNo ratings yet

- Code of Professional Ethics For CPAS in The PhilippinesDocument81 pagesCode of Professional Ethics For CPAS in The PhilippinesRicardo DalisayNo ratings yet

- Professional Ethics P2Document19 pagesProfessional Ethics P2chandrsenNo ratings yet

- GBERMIC - Code of Ethics For Professional Accountants Part ADocument5 pagesGBERMIC - Code of Ethics For Professional Accountants Part AReviewers KoNo ratings yet

- Auditing Ethics: Lecture # 2 Fundamental PrinciplesDocument3 pagesAuditing Ethics: Lecture # 2 Fundamental PrinciplessiddiqueicmaNo ratings yet

- Code of EthicsDocument24 pagesCode of EthicsEman SaeedNo ratings yet

- Dac 204 Lecture 2Document27 pagesDac 204 Lecture 2raina mattNo ratings yet

- Lecture Notes - Code of EthicsDocument5 pagesLecture Notes - Code of EthicsHalim Matuan MaamorNo ratings yet

- The Regulatory Framework, Ethics and Conceptual FrameworkDocument14 pagesThe Regulatory Framework, Ethics and Conceptual FrameworkMelvin AmohNo ratings yet

- Code of Ethics For AccountantsDocument49 pagesCode of Ethics For AccountantsAlly CapacioNo ratings yet

- Mas Practice Standards and Ethical Considerations MAS Practice Standards Personal CharacteristicsDocument4 pagesMas Practice Standards and Ethical Considerations MAS Practice Standards Personal CharacteristicsRoderick RonidelNo ratings yet

- Governance and Control FINAL VERSION 2Document261 pagesGovernance and Control FINAL VERSION 2jasminet.arendseNo ratings yet

- Code of Ethics For Professional AccountantDocument14 pagesCode of Ethics For Professional AccountantClarise Satentes AquinoNo ratings yet

- Lecture 5-Professional Ethics and Code of ConductDocument29 pagesLecture 5-Professional Ethics and Code of ConductNatalia NaveedNo ratings yet

- Auditing 1 L2 Professional EthicsDocument32 pagesAuditing 1 L2 Professional EthicsvictoriaNo ratings yet

- EthicsDocument7 pagesEthicsdominicNo ratings yet

- Chapter 4 Ethics and AcceptanceDocument10 pagesChapter 4 Ethics and Acceptancerishi kareliaNo ratings yet

- Certified Risk and Compliance ProfessionalFrom EverandCertified Risk and Compliance ProfessionalRating: 5 out of 5 stars5/5 (3)

- PSKCVL San-Gavino 6917021.decDocument6 pagesPSKCVL San-Gavino 6917021.decAngel Niño Pabalan LayugNo ratings yet

- Parang DecDocument63 pagesParang DecAngelika CalingasanNo ratings yet

- Professional Conduct CHAPTER IIETHICALSTANDARDDocument112 pagesProfessional Conduct CHAPTER IIETHICALSTANDARDjoshuabron100% (2)

- Aruna Ramchandra Shanbaug v. Union of India - Case AnalysisDocument9 pagesAruna Ramchandra Shanbaug v. Union of India - Case AnalysisShriya JainNo ratings yet

- Canon 15 Seares Vs AlzateDocument5 pagesCanon 15 Seares Vs AlzateLeomar Despi Ladonga100% (1)

- Malamig DecDocument46 pagesMalamig DecAngelika CalingasanNo ratings yet

- ISACA Certification IT Audit - Security - Governance and RiskDocument33 pagesISACA Certification IT Audit - Security - Governance and Riskakbisoi1No ratings yet

- TAWAGAN Dec PDFDocument32 pagesTAWAGAN Dec PDFAngelika CalingasanNo ratings yet

- Learning Episode 6.3Document7 pagesLearning Episode 6.3Rezia Rose PagdilaoNo ratings yet

- Couns Mod 6 - EthicsDocument7 pagesCouns Mod 6 - EthicsHarshita KapoorNo ratings yet

- 16,32,34 - Teacher Accountability Unit 1 Part BDocument19 pages16,32,34 - Teacher Accountability Unit 1 Part BPriya SinghNo ratings yet

- Professional EthicsDocument14 pagesProfessional EthicsAbhas Jaiswal100% (1)

- Engineers Registration Board: Code of Conduct AND Ethics For EngineersDocument10 pagesEngineers Registration Board: Code of Conduct AND Ethics For EngineersAraban SuleimanNo ratings yet

- DSM 5 Personality Disorder PDFDocument2 pagesDSM 5 Personality Disorder PDFRita HenriquesNo ratings yet

- (UTS) Etika PenelitianDocument65 pages(UTS) Etika PenelitianIntan wahyuNo ratings yet

- Teachers' Accountability: Key To Quality EducationDocument2 pagesTeachers' Accountability: Key To Quality EducationNegash Hebo100% (1)

- Disciplining The Lawyers - Law and Professional Ethics PDFDocument71 pagesDisciplining The Lawyers - Law and Professional Ethics PDFHarshid AgarwalNo ratings yet

- Behringer INuke NU3000 SCHDocument3 pagesBehringer INuke NU3000 SCHcassiusone50% (4)

- Professional EthicsDocument19 pagesProfessional EthicsVEENA NAMANo ratings yet

- Chapter Two Ethics and MoralityDocument53 pagesChapter Two Ethics and MoralityTesfaye Gemechu100% (1)

- ICCT Colleges Foundation, IncDocument2 pagesICCT Colleges Foundation, IncSheen CatayongNo ratings yet

- 02 Standards of Professional Conduct & Guidance Professionalism PDFDocument20 pages02 Standards of Professional Conduct & Guidance Professionalism PDFSardonna FongNo ratings yet

- Ge6075 MCQDocument29 pagesGe6075 MCQVishnu53% (15)

- Block-5 BLIS-01 Unit-14Document12 pagesBlock-5 BLIS-01 Unit-14HALLNo ratings yet

- International Council For Homeopathy - National Health Portal of IndiaDocument9 pagesInternational Council For Homeopathy - National Health Portal of IndiaDr. Kazy Habibur RahmanNo ratings yet

- Prahalad Saran Gupta Case StudyDocument20 pagesPrahalad Saran Gupta Case StudyKhokher AnchitNo ratings yet

- Ms. Naina JainDocument31 pagesMs. Naina JainRichard SebestianNo ratings yet

- PiecesDocument7 pagesPiecesDee MartyNo ratings yet

- ATP 105 Professional Ethics and Practice - Conflict of InterestDocument14 pagesATP 105 Professional Ethics and Practice - Conflict of InterestJames Otieno OgutuNo ratings yet

You might also like

- 533-Ethics QuizDocument8 pages533-Ethics Quizapi-562856559100% (1)

- Chapter Three: Professional Ethics and Legal Liability of AuditorsDocument35 pagesChapter Three: Professional Ethics and Legal Liability of Auditorseferem100% (1)

- Mas Practice Standards and Ethical ConsiderationsACDocument3 pagesMas Practice Standards and Ethical ConsiderationsACLorenz BaguioNo ratings yet

- Mas Practice Standards and EthicalconsiderationsDocument6 pagesMas Practice Standards and EthicalconsiderationsRolanElumbreNo ratings yet

- Code of Ethics: FOR Professional AccountantsDocument42 pagesCode of Ethics: FOR Professional AccountantsTracy Marsh RapanutNo ratings yet

- Code of Ethics For Professional AccountantsDocument17 pagesCode of Ethics For Professional AccountantsJay Mark AbellarNo ratings yet

- Advanced Auditing Chapter ThreeDocument49 pagesAdvanced Auditing Chapter ThreemirogNo ratings yet

- Code of Ethics Updated PDFDocument130 pagesCode of Ethics Updated PDFSalvador BrionesNo ratings yet

- Chapter 4 Audit f8 - 2.3Document43 pagesChapter 4 Audit f8 - 2.3JosephineMicheal17No ratings yet

- Code of EthicsDocument5 pagesCode of EthicsAira Shynne AsperaNo ratings yet

- 03.2 Handbook of The International Code of Ethics For Professional AccountantsDocument92 pages03.2 Handbook of The International Code of Ethics For Professional AccountantsnuggsNo ratings yet

- Code of Ethics For Ba II.Document25 pagesCode of Ethics For Ba II.beatricenyashiruNo ratings yet

- Code of EthicsDocument78 pagesCode of EthicsNeriza PonceNo ratings yet

- Code of Ethics - EditedDocument76 pagesCode of Ethics - EditedAaron Mañacap100% (1)

- Professional EthicsDocument4 pagesProfessional EthicsCameille SalmonNo ratings yet

- 2.0 Ethical Concerns For Accountants Mike MbayaDocument38 pages2.0 Ethical Concerns For Accountants Mike MbayaREJAY89No ratings yet

- Code of Ethics For Professional Accountants HandoutDocument25 pagesCode of Ethics For Professional Accountants Handoutsaidkhatib368No ratings yet

- AA - 2023 11 Professional EthicsDocument13 pagesAA - 2023 11 Professional EthicstahreemNo ratings yet

- AA - Spring 2021 11 Professional EthicsDocument13 pagesAA - Spring 2021 11 Professional EthicsSarim AhmadNo ratings yet

- Additional Ethics SlidesDocument5 pagesAdditional Ethics Slidesathirah jamaludinNo ratings yet

- Week 2 Professional ConductDocument31 pagesWeek 2 Professional Conductptnyagortey91No ratings yet

- 1) Code of Ethics For AuditorsDocument29 pages1) Code of Ethics For Auditorsrajes wari50% (2)

- Chapter 2Document21 pagesChapter 2Danish NabilNo ratings yet

- MAS 4 TOPIC 1 Threats and Safeguards in The Practice of Accountancy (Reviewer)Document18 pagesMAS 4 TOPIC 1 Threats and Safeguards in The Practice of Accountancy (Reviewer)vintmyoNo ratings yet

- Code of Professional EthicsDocument42 pagesCode of Professional EthicsMariella CatacutanNo ratings yet

- Slides - Lecture 2 - ST VersionDocument17 pagesSlides - Lecture 2 - ST VersionNguyễn Thu UyênNo ratings yet

- Topic 2 The Role of Professional AccountantDocument27 pagesTopic 2 The Role of Professional AccountantYanPing AngNo ratings yet

- Topic 2 MIA by LawDocument32 pagesTopic 2 MIA by LawNUR IMAN SHAHIDAH BINTI SHAHRUL RIZALNo ratings yet

- Professional Duty of AccountantDocument14 pagesProfessional Duty of AccountantTiya AmuNo ratings yet

- Audit 2: Puan Roslina Binti IdrisDocument12 pagesAudit 2: Puan Roslina Binti Idrishakim azmiNo ratings yet

- At.1304 - Code of EthicsDocument29 pagesAt.1304 - Code of EthicsSheila Mae PlanciaNo ratings yet

- Chapter 13 Codes of Professional EthicsDocument26 pagesChapter 13 Codes of Professional EthicslnghiilwamoNo ratings yet

- 08 JournalDocument6 pages08 Journalits me keiNo ratings yet

- 6-Professional EthicsDocument26 pages6-Professional EthicsQila HusinNo ratings yet

- Code of Ethics: Prof. Zeus A. Aboy, CPA MBA EDL (Candidate)Document75 pagesCode of Ethics: Prof. Zeus A. Aboy, CPA MBA EDL (Candidate)Io AyaNo ratings yet

- Code of EthicsDocument35 pagesCode of EthicsJamsankin PersianNo ratings yet

- UntitledDocument14 pagesUntitledEllieNo ratings yet

- Business Ethics Part 2Document23 pagesBusiness Ethics Part 2Gilner PomarNo ratings yet

- Audit I-Chapter TwoDocument11 pagesAudit I-Chapter Twothedalesh weldeNo ratings yet

- Code of Ethics of Professional AccountantsDocument3 pagesCode of Ethics of Professional AccountantsYamateNo ratings yet

- Auditors Independence Review - 1Document22 pagesAuditors Independence Review - 1Mohammad Abu Kawsar FcaNo ratings yet

- 02 - Code of Ethics of ProfessionalDocument22 pages02 - Code of Ethics of ProfessionalYamateNo ratings yet

- Code of Professional Ethics For CPAS in The PhilippinesDocument81 pagesCode of Professional Ethics For CPAS in The PhilippinesRicardo DalisayNo ratings yet

- Professional Ethics P2Document19 pagesProfessional Ethics P2chandrsenNo ratings yet

- GBERMIC - Code of Ethics For Professional Accountants Part ADocument5 pagesGBERMIC - Code of Ethics For Professional Accountants Part AReviewers KoNo ratings yet

- Auditing Ethics: Lecture # 2 Fundamental PrinciplesDocument3 pagesAuditing Ethics: Lecture # 2 Fundamental PrinciplessiddiqueicmaNo ratings yet

- Code of EthicsDocument24 pagesCode of EthicsEman SaeedNo ratings yet

- Dac 204 Lecture 2Document27 pagesDac 204 Lecture 2raina mattNo ratings yet

- Lecture Notes - Code of EthicsDocument5 pagesLecture Notes - Code of EthicsHalim Matuan MaamorNo ratings yet

- The Regulatory Framework, Ethics and Conceptual FrameworkDocument14 pagesThe Regulatory Framework, Ethics and Conceptual FrameworkMelvin AmohNo ratings yet

- Code of Ethics For AccountantsDocument49 pagesCode of Ethics For AccountantsAlly CapacioNo ratings yet

- Mas Practice Standards and Ethical Considerations MAS Practice Standards Personal CharacteristicsDocument4 pagesMas Practice Standards and Ethical Considerations MAS Practice Standards Personal CharacteristicsRoderick RonidelNo ratings yet

- Governance and Control FINAL VERSION 2Document261 pagesGovernance and Control FINAL VERSION 2jasminet.arendseNo ratings yet

- Code of Ethics For Professional AccountantDocument14 pagesCode of Ethics For Professional AccountantClarise Satentes AquinoNo ratings yet

- Lecture 5-Professional Ethics and Code of ConductDocument29 pagesLecture 5-Professional Ethics and Code of ConductNatalia NaveedNo ratings yet

- Auditing 1 L2 Professional EthicsDocument32 pagesAuditing 1 L2 Professional EthicsvictoriaNo ratings yet

- EthicsDocument7 pagesEthicsdominicNo ratings yet

- Chapter 4 Ethics and AcceptanceDocument10 pagesChapter 4 Ethics and Acceptancerishi kareliaNo ratings yet

- Certified Risk and Compliance ProfessionalFrom EverandCertified Risk and Compliance ProfessionalRating: 5 out of 5 stars5/5 (3)

- PSKCVL San-Gavino 6917021.decDocument6 pagesPSKCVL San-Gavino 6917021.decAngel Niño Pabalan LayugNo ratings yet

- Parang DecDocument63 pagesParang DecAngelika CalingasanNo ratings yet

- Professional Conduct CHAPTER IIETHICALSTANDARDDocument112 pagesProfessional Conduct CHAPTER IIETHICALSTANDARDjoshuabron100% (2)

- Aruna Ramchandra Shanbaug v. Union of India - Case AnalysisDocument9 pagesAruna Ramchandra Shanbaug v. Union of India - Case AnalysisShriya JainNo ratings yet

- Canon 15 Seares Vs AlzateDocument5 pagesCanon 15 Seares Vs AlzateLeomar Despi Ladonga100% (1)

- Malamig DecDocument46 pagesMalamig DecAngelika CalingasanNo ratings yet

- ISACA Certification IT Audit - Security - Governance and RiskDocument33 pagesISACA Certification IT Audit - Security - Governance and Riskakbisoi1No ratings yet

- TAWAGAN Dec PDFDocument32 pagesTAWAGAN Dec PDFAngelika CalingasanNo ratings yet

- Learning Episode 6.3Document7 pagesLearning Episode 6.3Rezia Rose PagdilaoNo ratings yet

- Couns Mod 6 - EthicsDocument7 pagesCouns Mod 6 - EthicsHarshita KapoorNo ratings yet

- 16,32,34 - Teacher Accountability Unit 1 Part BDocument19 pages16,32,34 - Teacher Accountability Unit 1 Part BPriya SinghNo ratings yet

- Professional EthicsDocument14 pagesProfessional EthicsAbhas Jaiswal100% (1)

- Engineers Registration Board: Code of Conduct AND Ethics For EngineersDocument10 pagesEngineers Registration Board: Code of Conduct AND Ethics For EngineersAraban SuleimanNo ratings yet

- DSM 5 Personality Disorder PDFDocument2 pagesDSM 5 Personality Disorder PDFRita HenriquesNo ratings yet

- (UTS) Etika PenelitianDocument65 pages(UTS) Etika PenelitianIntan wahyuNo ratings yet

- Teachers' Accountability: Key To Quality EducationDocument2 pagesTeachers' Accountability: Key To Quality EducationNegash Hebo100% (1)

- Disciplining The Lawyers - Law and Professional Ethics PDFDocument71 pagesDisciplining The Lawyers - Law and Professional Ethics PDFHarshid AgarwalNo ratings yet

- Behringer INuke NU3000 SCHDocument3 pagesBehringer INuke NU3000 SCHcassiusone50% (4)

- Professional EthicsDocument19 pagesProfessional EthicsVEENA NAMANo ratings yet

- Chapter Two Ethics and MoralityDocument53 pagesChapter Two Ethics and MoralityTesfaye Gemechu100% (1)

- ICCT Colleges Foundation, IncDocument2 pagesICCT Colleges Foundation, IncSheen CatayongNo ratings yet

- 02 Standards of Professional Conduct & Guidance Professionalism PDFDocument20 pages02 Standards of Professional Conduct & Guidance Professionalism PDFSardonna FongNo ratings yet

- Ge6075 MCQDocument29 pagesGe6075 MCQVishnu53% (15)

- Block-5 BLIS-01 Unit-14Document12 pagesBlock-5 BLIS-01 Unit-14HALLNo ratings yet

- International Council For Homeopathy - National Health Portal of IndiaDocument9 pagesInternational Council For Homeopathy - National Health Portal of IndiaDr. Kazy Habibur RahmanNo ratings yet

- Prahalad Saran Gupta Case StudyDocument20 pagesPrahalad Saran Gupta Case StudyKhokher AnchitNo ratings yet

- Ms. Naina JainDocument31 pagesMs. Naina JainRichard SebestianNo ratings yet

- PiecesDocument7 pagesPiecesDee MartyNo ratings yet

- ATP 105 Professional Ethics and Practice - Conflict of InterestDocument14 pagesATP 105 Professional Ethics and Practice - Conflict of InterestJames Otieno OgutuNo ratings yet