You might also like

- Steel Industry Update #252Document8 pagesSteel Industry Update #252Michael LockerNo ratings yet

- JSPL Balance Sheet Analysis 2009Document16 pagesJSPL Balance Sheet Analysis 2009Kaustubh TiwaryNo ratings yet

- Ica 2024Document107 pagesIca 2024Tushar MircheNo ratings yet

- Steel Update July 2020Document4 pagesSteel Update July 2020DarshanNo ratings yet

- Earning Release 2Q22 Hyosung Heavy Industries (Eng.)Document14 pagesEarning Release 2Q22 Hyosung Heavy Industries (Eng.)Scriptlance 2012No ratings yet

- Steelmaking Raw Materials: DSTI/SU/SC (2011) 2 70 Steel Committee Meeting Paris 12-13 May 2011Document10 pagesSteelmaking Raw Materials: DSTI/SU/SC (2011) 2 70 Steel Committee Meeting Paris 12-13 May 2011Ari SudrajatNo ratings yet

- MRM 05 2022Document85 pagesMRM 05 2022Tapas PadhiNo ratings yet

- Steel Industry Update #255Document7 pagesSteel Industry Update #255Michael LockerNo ratings yet

- Toromocho Jan2017 Competent Persons ReportDocument147 pagesToromocho Jan2017 Competent Persons Reportmaría joséNo ratings yet

- Report On Cement IndustryDocument33 pagesReport On Cement Industrykanu vij67% (9)

- Forecast Month - June 2010 Table Beginning Year - 2006 Table Beginning Quarter - 200601Document38 pagesForecast Month - June 2010 Table Beginning Year - 2006 Table Beginning Quarter - 200601younesselkandoussiNo ratings yet

- SAIL JO Manual 2022 - Industry & Company AwarnessDocument102 pagesSAIL JO Manual 2022 - Industry & Company AwarnessT V KANNANNo ratings yet

- Cement Stablied Updated FileDocument11 pagesCement Stablied Updated FileRitesh ChauhanNo ratings yet

- Profile of Steel IndustryDocument17 pagesProfile of Steel IndustrylankasaikiranNo ratings yet

- Assignment 2&3 - Liza DsouzaDocument67 pagesAssignment 2&3 - Liza DsouzaLiza DsouzaNo ratings yet

- JSW Steel Equity Research ReportDocument16 pagesJSW Steel Equity Research ReportHarsha SharmaNo ratings yet

- Challenges in Growth OF Indian Steel Industry: Monnet Ispat & Energy LTDDocument22 pagesChallenges in Growth OF Indian Steel Industry: Monnet Ispat & Energy LTDshwetali23No ratings yet

- Engineering Properties of Laterite Stone Scrap Blocks: S.K. Jain, P.G. Patil, N.J. ThakorDocument11 pagesEngineering Properties of Laterite Stone Scrap Blocks: S.K. Jain, P.G. Patil, N.J. ThakorchethanNo ratings yet

- Steel Industry in Indi1Document24 pagesSteel Industry in Indi1Vatsal JainNo ratings yet

- Camel Back StripDocument18 pagesCamel Back StripTilahun GemedaNo ratings yet

- KBSL - IIP October UpdateDocument4 pagesKBSL - IIP October UpdateRahulNo ratings yet

- Together We Build A Better FutureDocument29 pagesTogether We Build A Better FutureShintia AndrianiNo ratings yet

- Requirements of Raw Materials For Steel Industry Reflections On MMDR Bill 2011Document17 pagesRequirements of Raw Materials For Steel Industry Reflections On MMDR Bill 2011donhan91No ratings yet

- Maithan AlloysDocument5 pagesMaithan AlloysslohariNo ratings yet

- Anand Ratpital Goods Q2FY22 Result PreviewDocument13 pagesAnand Ratpital Goods Q2FY22 Result PreviewRaktim BiswasNo ratings yet

- Steel SectorDocument38 pagesSteel SectorKamta Prasad SahuNo ratings yet

- Ezz Steel Strategic Management ProjectDocument53 pagesEzz Steel Strategic Management ProjectAbdulrhman Tantawy75% (4)

- 200308steel IndustryDocument8 pages200308steel IndustrySylvia GraceNo ratings yet

- Kotak Consolidated Earnings EstimatesDocument50 pagesKotak Consolidated Earnings EstimatesAnkit JainNo ratings yet

- Glass Recycling in Cement Production AnDocument7 pagesGlass Recycling in Cement Production AnKiran KiranaNo ratings yet

- Geopolymer An OverviewDocument16 pagesGeopolymer An OverviewmayaNo ratings yet

- 2023 12 21 Monthly Press ReleaseDocument2 pages2023 12 21 Monthly Press ReleasechaxaimNo ratings yet

- Astm A615m PDFDocument12 pagesAstm A615m PDFAnonymous q8HhQ4w50% (2)

- Q 3 Nov 2006Document6 pagesQ 3 Nov 2006payalmittal1919No ratings yet

- Gainful Utilization of Sugarcane Bagasse Ash (Paper 5-Paper 8)Document19 pagesGainful Utilization of Sugarcane Bagasse Ash (Paper 5-Paper 8)nishu mangalNo ratings yet

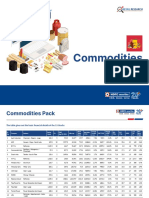

- HSL - Commodities Pack Report - 2021-202108182348310059173Document16 pagesHSL - Commodities Pack Report - 2021-202108182348310059173SHAIK AHMEDNo ratings yet

- Gainful Utilization of Sugarcane Bagasse Ash (Paper 5-Paper 8)Document19 pagesGainful Utilization of Sugarcane Bagasse Ash (Paper 5-Paper 8)nishu mangalNo ratings yet

- Gainful Utilization of Sugarcane Bagasse Ash (Paper 5-Paper 8)Document19 pagesGainful Utilization of Sugarcane Bagasse Ash (Paper 5-Paper 8)nishu mangalNo ratings yet

- Financial Year 2006 07Document46 pagesFinancial Year 2006 07Prabal SenNo ratings yet

- Steel Industry Update #249Document8 pagesSteel Industry Update #249Michael LockerNo ratings yet

- Norsok U 001Document15 pagesNorsok U 001Zadeh NormanNo ratings yet

- Market Structure Indian Steel SectorDocument6 pagesMarket Structure Indian Steel SectorSachin SinghNo ratings yet

- MBA PROJECT Report On BSRMDocument75 pagesMBA PROJECT Report On BSRMNamhin ShironamNo ratings yet

- Business Studies: Exports and ImportsDocument3 pagesBusiness Studies: Exports and ImportsDimple VaishnavNo ratings yet

- Discounted Cash Flow Analysis - Steel Dynamics Inc. (Unlevered DCF)Document4 pagesDiscounted Cash Flow Analysis - Steel Dynamics Inc. (Unlevered DCF)Moni DahalNo ratings yet

- Release of ICSG 2012 Statistical YearbookDocument1 pageRelease of ICSG 2012 Statistical YearbookashleyNo ratings yet

- Appendix 2 GMU PVC Decarb 2050Document18 pagesAppendix 2 GMU PVC Decarb 2050Abby LaingNo ratings yet

- Project Report 1Document22 pagesProject Report 1chanderNo ratings yet

- Catalog Posco InoxDocument4 pagesCatalog Posco InoxNam TranNo ratings yet

- Sector Briefing - Steel Industry Overview: Fig.2 Major Steel-Producing CountriesDocument2 pagesSector Briefing - Steel Industry Overview: Fig.2 Major Steel-Producing CountriesHimadri SNo ratings yet

- 49189151Document10 pages49189151Chirag FulwaniNo ratings yet

- Vale's 3Q23 Production and Sales ReportDocument7 pagesVale's 3Q23 Production and Sales ReportSoniwell SoniwellNo ratings yet

- Kalyani Steel LimitedDocument26 pagesKalyani Steel LimitedSHREEYA BHATNo ratings yet

- Urban Transport and Automobile Air Pollution in Mysuru, IndiaDocument20 pagesUrban Transport and Automobile Air Pollution in Mysuru, IndiaAzis Kemal FauzieNo ratings yet

- Draft Policy For Steel Cluster - vf15Document40 pagesDraft Policy For Steel Cluster - vf15Abhijeet SinghNo ratings yet

- Tata Corus AcquazitionDocument30 pagesTata Corus AcquazitionAnkushNo ratings yet

- RKC Guidelines CH 6Document52 pagesRKC Guidelines CH 6Fajar SudrajatNo ratings yet

- The Nickel Market: I. Historical PricesDocument4 pagesThe Nickel Market: I. Historical PricesTuan AnhNo ratings yet

- 489-Article Text-1315-1-10-20200402Document15 pages489-Article Text-1315-1-10-20200402Alex PelaezNo ratings yet

- Class 12 Chapter 4 PlanningDocument7 pagesClass 12 Chapter 4 Planningdeepanshu kumarNo ratings yet

- AgarbattiDocument42 pagesAgarbattiDhwani Thakkar50% (2)

- BAHRE 311 - Week 1 2 - ULO BDocument6 pagesBAHRE 311 - Week 1 2 - ULO BMarlyn TugapNo ratings yet

- SCM AgreementDocument6 pagesSCM AgreementankitaprakashsinghNo ratings yet

- India's Economy and Society: Sunil Mani Chidambaran G. Iyer EditorsDocument439 pagesIndia's Economy and Society: Sunil Mani Chidambaran G. Iyer EditorsАнастасия ТукноваNo ratings yet

- Clow Imc8 Inppt 08Document46 pagesClow Imc8 Inppt 08Manar AmrNo ratings yet

- Retail Turnover Rent Model: Units of Projection 1,000Document26 pagesRetail Turnover Rent Model: Units of Projection 1,000tudormunteanNo ratings yet

- Philippines National Bank vs. Erlando T. RodriguezDocument2 pagesPhilippines National Bank vs. Erlando T. RodriguezKen MarcaidaNo ratings yet

- Workshop 4 Maths: Ingrid Nathalia Díaz BonillaDocument7 pagesWorkshop 4 Maths: Ingrid Nathalia Díaz BonillaNathalia BonillaNo ratings yet

- 1 Women's Entrepreneurship and Economic Empowerment (Sample Proposal)Document3 pages1 Women's Entrepreneurship and Economic Empowerment (Sample Proposal)ernextohoNo ratings yet

- Punjab Spatial Planning StrategyDocument12 pagesPunjab Spatial Planning Strategybaloch47No ratings yet

- Bibliography Financial CrisisDocument41 pagesBibliography Financial CrisisaflagsonNo ratings yet

- VP Director HR Talent Management in San Francisco Bay CA Resume Shirley BraunDocument3 pagesVP Director HR Talent Management in San Francisco Bay CA Resume Shirley BraunShirleyBraunNo ratings yet

- Fedex Label - PL2303002 S&S MartechDocument6 pagesFedex Label - PL2303002 S&S MartechAnh HuynhNo ratings yet

- Income and Substitution EffectsDocument1 pageIncome and Substitution EffectspenelopegerhardNo ratings yet

- Mergers and Acquisition and Treatments To IPR Project (8th Semester)Document15 pagesMergers and Acquisition and Treatments To IPR Project (8th Semester)raj vardhan agarwalNo ratings yet

- MBM 207 QB - DistanceDocument2 pagesMBM 207 QB - Distancemunish2030No ratings yet

- Deposit Slip ID: 192765 Deposit Slip ID: 192765: Fee Deposit Slip-Candidate Copy Fee Deposit Slip-BankDocument1 pageDeposit Slip ID: 192765 Deposit Slip ID: 192765: Fee Deposit Slip-Candidate Copy Fee Deposit Slip-BankAsim HussainNo ratings yet

- Definitions of Globalization - A Comprehensive Overview and A Proposed DefinitionDocument21 pagesDefinitions of Globalization - A Comprehensive Overview and A Proposed Definitionnagendrar_2No ratings yet

- Tiffin ServiceDocument17 pagesTiffin Servicehardik patel0% (1)

- Costing TheoryDocument26 pagesCosting TheoryShweta MadhuNo ratings yet

- Challenges and Opportunities Facing Brand Management - An IntroducDocument12 pagesChallenges and Opportunities Facing Brand Management - An IntroducLeyds GalvezNo ratings yet

- Architect / Contract Administrator's Instruction: Estimated Revised Contract PriceDocument6 pagesArchitect / Contract Administrator's Instruction: Estimated Revised Contract PriceAfiya PatersonNo ratings yet

- Big Picture A in Focus: Uloa.: Let'S CheckDocument6 pagesBig Picture A in Focus: Uloa.: Let'S CheckNatsu PolsjaNo ratings yet

- Agriculture Procurement Buffer Stock FCI Reforms and PDS PDFDocument10 pagesAgriculture Procurement Buffer Stock FCI Reforms and PDS PDFAshutosh JhaNo ratings yet

- Group 4 Amazon 45k01.1Document73 pagesGroup 4 Amazon 45k01.1Đỗ Hiếu ThuậnNo ratings yet

- Labour Economics: Albrecht GlitzDocument44 pagesLabour Economics: Albrecht GlitzmarNo ratings yet

- The Journal Jan-Mar 2018Document100 pagesThe Journal Jan-Mar 2018Paul BanerjeeNo ratings yet

- Content/Elements of Business Plan: Mary Mildred P. de Jesus SHS TeacherDocument28 pagesContent/Elements of Business Plan: Mary Mildred P. de Jesus SHS TeacherMary De JesusNo ratings yet

- Value Added TaxDocument46 pagesValue Added TaxBoss NikNo ratings yet