You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- TCQT-1Document8 pagesTCQT-1uyên vươngNo ratings yet

- Leveraging Technology for Property Tax Management in Asia and the Pacific–Guidance NoteFrom EverandLeveraging Technology for Property Tax Management in Asia and the Pacific–Guidance NoteNo ratings yet

- Risk ManagementDocument7 pagesRisk ManagementKhalid Mishczsuski Limu100% (1)

- Strategic Management & Business Policy Ch 8 Strategy FormulationDocument6 pagesStrategic Management & Business Policy Ch 8 Strategy FormulationAbigail LeronNo ratings yet

- Wiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)No ratings yet

- Analyzing Management Services and Cost-Volume-Profit AnalysisDocument16 pagesAnalyzing Management Services and Cost-Volume-Profit AnalysisChristian Clyde Zacal ChingNo ratings yet

- Final MockboardDocument16 pagesFinal MockboardChristian Clyde Zacal ChingNo ratings yet

- Compre ExamDocument11 pagesCompre Examena20_paderangaNo ratings yet

- The Comprehensive Guide for Minority Tech Startups Securing Lucrative Government Contracts, Harnessing Business Opportunities, and Achieving Long-Term SuccessFrom EverandThe Comprehensive Guide for Minority Tech Startups Securing Lucrative Government Contracts, Harnessing Business Opportunities, and Achieving Long-Term SuccessNo ratings yet

- Dwnload Full Cost Management A Strategic Emphasis 8th Edition Blocher Test Bank PDFDocument35 pagesDwnload Full Cost Management A Strategic Emphasis 8th Edition Blocher Test Bank PDFlauritastadts2900100% (15)

- BSA 3102 Management Accounting PRELIMS PDFDocument20 pagesBSA 3102 Management Accounting PRELIMS PDFRyzel BorjaNo ratings yet

- Finman Test Bank2Document11 pagesFinman Test Bank2ATHALIAH LUNA MERCADEJAS100% (1)

- Chapter 1 Homework Assignment Fall 2018Document8 pagesChapter 1 Homework Assignment Fall 2018Marouf AlhndiNo ratings yet

- BusFin ExamDocument16 pagesBusFin ExamBlessel Rose PaquinganNo ratings yet

- Income Statement Format and PresentationDocument52 pagesIncome Statement Format and PresentationIvern BautistaNo ratings yet

- Accounts Exam Self Study Questions Chap1Document11 pagesAccounts Exam Self Study Questions Chap1pratik kcNo ratings yet

- Introduction to Financial ManagementDocument7 pagesIntroduction to Financial ManagementMicah ErguizaNo ratings yet

- Mastery in Management Advisory ServicesDocument12 pagesMastery in Management Advisory ServicesPrincess Claris Araucto0% (1)

- Multiple Choices 1Document2 pagesMultiple Choices 1ssg2No ratings yet

- Test Bank For International Corporate Finance 0073530662 Full DownloadDocument29 pagesTest Bank For International Corporate Finance 0073530662 Full Downloadnataliewallyfcgxdbeaq100% (39)

- Exam Questions Fina4810Document9 pagesExam Questions Fina4810Bartholomew Szold75% (4)

- Chap 4Document52 pagesChap 4Ella Mae LayarNo ratings yet

- 10 28 QuestionsDocument5 pages10 28 QuestionstikaNo ratings yet

- Financial Statement AnalysisDocument11 pagesFinancial Statement AnalysisJhuneth DominguezNo ratings yet

- Chapter 1 StudentsDocument7 pagesChapter 1 StudentsArah Opalec0% (1)

- Income Statement and Related Information: Chapter Learning ObjectivesDocument53 pagesIncome Statement and Related Information: Chapter Learning Objectivesheyhey100% (1)

- Financial Institutions Instruments and Markets 7th Edition Viney Test BankDocument48 pagesFinancial Institutions Instruments and Markets 7th Edition Viney Test Bankbunkerlulleruc3s100% (29)

- GbsDocument8 pagesGbsPavan DeshpandeNo ratings yet

- Multiple Choice QuestionshDocument5 pagesMultiple Choice QuestionshHischa Ubri De JesusNo ratings yet

- FINMAN QUIZ 1 SOLUTIONSDocument5 pagesFINMAN QUIZ 1 SOLUTIONSMicah ErguizaNo ratings yet

- Ch2 Multiple Choice QuestionsDocument9 pagesCh2 Multiple Choice QuestionsAfsana ParveenNo ratings yet

- Accounting TheoryDocument5 pagesAccounting TheoryMichelle ANo ratings yet

- Intermediate Accounting Testbank 2Document419 pagesIntermediate Accounting Testbank 2SOPHIA97% (30)

- Financial Institutions Instruments and Markets 7Th Edition Viney Test Bank Full Chapter PDFDocument68 pagesFinancial Institutions Instruments and Markets 7Th Edition Viney Test Bank Full Chapter PDFhieudermotjm7w100% (10)

- Test Bank For International Corporate Finance 0073530662Document30 pagesTest Bank For International Corporate Finance 0073530662arianluufjs100% (17)

- DBC FinquizDocument6 pagesDBC FinquizAshutosh SatapathyNo ratings yet

- FIN622 Online Quiz - PdfaDocument531 pagesFIN622 Online Quiz - Pdfazahidwahla1100% (3)

- Multiple Choice. Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionsDocument8 pagesMultiple Choice. Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionsRandy ManzanoNo ratings yet

- AnswersDocument11 pagesAnswershoney arguellesNo ratings yet

- MCQ TestDocument10 pagesMCQ TestcalliemozartNo ratings yet

- PROBLEMSDocument8 pagesPROBLEMSSaeym SegoviaNo ratings yet

- Chapter 1 3Document17 pagesChapter 1 3Hieu Duong Trong100% (3)

- FIN1S Prelim ExamDocument7 pagesFIN1S Prelim ExamYu BabylanNo ratings yet

- Baba2 Fin MidtermDocument8 pagesBaba2 Fin MidtermYu BabylanNo ratings yet

- International Corporate Finance 1St Edition Robin Test Bank Full Chapter PDFDocument50 pagesInternational Corporate Finance 1St Edition Robin Test Bank Full Chapter PDFlyeliassh5100% (9)

- International Corporate Finance 1st Edition Robin Test BankDocument29 pagesInternational Corporate Finance 1st Edition Robin Test Bankchristabeldienj30da100% (24)

- Introduction To Financial Management Quiz 1 - CompressDocument3 pagesIntroduction To Financial Management Quiz 1 - CompressLenson NatividadNo ratings yet

- File Tổng Hợp Quizz Ktqt 1: File này mấy bạn muốn sao chép, chia sẻ, hay đi phô tô thì thoải mái nhaDocument38 pagesFile Tổng Hợp Quizz Ktqt 1: File này mấy bạn muốn sao chép, chia sẻ, hay đi phô tô thì thoải mái nhaDANH LÊ VĂNNo ratings yet

- 1st PB-TADocument12 pages1st PB-TAGlenn Patrick de LeonNo ratings yet

- FINA201 Main Exam paper June 2023 (3)Document13 pagesFINA201 Main Exam paper June 2023 (3)AyandaNo ratings yet

- Management Advisory ServicesDocument5 pagesManagement Advisory ServicesJL Favorito YambaoNo ratings yet

- MGT3580: Global Enterprise Management (Simulation Questions)Document3 pagesMGT3580: Global Enterprise Management (Simulation Questions)Chan JohnNo ratings yet

- Managerial Accounting IntroductionDocument24 pagesManagerial Accounting IntroductionCharla SuanNo ratings yet

- Answer The Following QuestionsDocument8 pagesAnswer The Following QuestionsTaha Wael QandeelNo ratings yet

- Possible Test1Document32 pagesPossible Test1Azim Jivani100% (3)

- International AccountingDocument26 pagesInternational AccountingOwen ZhangNo ratings yet

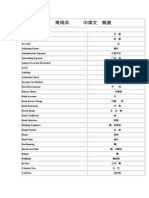

- 常用会计词汇中英文对照表Document8 pages常用会计词汇中英文对照表Owen ZhangNo ratings yet

- AuditingDocument2 pagesAuditingOwen ZhangNo ratings yet

- 508 HW1Document1 page508 HW1Owen ZhangNo ratings yet

- New Microsoft PowerPoint 演示文稿Document1 pageNew Microsoft PowerPoint 演示文稿Owen ZhangNo ratings yet

- AuditingDocument1 pageAuditingOwen ZhangNo ratings yet

- Tax2 HWDocument1 pageTax2 HWOwen ZhangNo ratings yet

- Hello WorldDocument1 pageHello WorldOwen ZhangNo ratings yet

- Hello WorldDocument1 pageHello WorldOwen ZhangNo ratings yet

- Summary of Zero to One: Notes on Startups, or How to Build the FutureFrom EverandSummary of Zero to One: Notes on Startups, or How to Build the FutureRating: 4.5 out of 5 stars4.5/5 (100)

- Summary: Who Not How: The Formula to Achieve Bigger Goals Through Accelerating Teamwork by Dan Sullivan & Dr. Benjamin Hardy:From EverandSummary: Who Not How: The Formula to Achieve Bigger Goals Through Accelerating Teamwork by Dan Sullivan & Dr. Benjamin Hardy:Rating: 5 out of 5 stars5/5 (2)

- SYSTEMology: Create time, reduce errors and scale your profits with proven business systemsFrom EverandSYSTEMology: Create time, reduce errors and scale your profits with proven business systemsRating: 5 out of 5 stars5/5 (48)

- To Pixar and Beyond: My Unlikely Journey with Steve Jobs to Make Entertainment HistoryFrom EverandTo Pixar and Beyond: My Unlikely Journey with Steve Jobs to Make Entertainment HistoryRating: 4 out of 5 stars4/5 (26)

- 12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurFrom Everand12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurRating: 4 out of 5 stars4/5 (2)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeFrom EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeRating: 4.5 out of 5 stars4.5/5 (88)

- ChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveFrom EverandChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveNo ratings yet

- What Self-Made Millionaires Do That Most People Don't: 52 Ways to Create Your Own SuccessFrom EverandWhat Self-Made Millionaires Do That Most People Don't: 52 Ways to Create Your Own SuccessRating: 4.5 out of 5 stars4.5/5 (24)

- The Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeFrom EverandThe Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeRating: 4.5 out of 5 stars4.5/5 (58)

- Don't Start a Side Hustle!: Work Less, Earn More, and Live FreeFrom EverandDon't Start a Side Hustle!: Work Less, Earn More, and Live FreeRating: 4.5 out of 5 stars4.5/5 (30)

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4 out of 5 stars4/5 (1)

- The Master Key System: 28 Parts, Questions and AnswersFrom EverandThe Master Key System: 28 Parts, Questions and AnswersRating: 5 out of 5 stars5/5 (62)

- Your Next Five Moves: Master the Art of Business StrategyFrom EverandYour Next Five Moves: Master the Art of Business StrategyRating: 5 out of 5 stars5/5 (799)

- 24 Assets: Create a digital, scalable, valuable and fun business that will thrive in a fast changing worldFrom Everand24 Assets: Create a digital, scalable, valuable and fun business that will thrive in a fast changing worldRating: 5 out of 5 stars5/5 (20)

- The Science of Positive Focus: Live Seminar: Master Keys for Reaching Your Next LevelFrom EverandThe Science of Positive Focus: Live Seminar: Master Keys for Reaching Your Next LevelRating: 5 out of 5 stars5/5 (51)

- Faith Driven Entrepreneur: What It Takes to Step Into Your Purpose and Pursue Your God-Given Call to CreateFrom EverandFaith Driven Entrepreneur: What It Takes to Step Into Your Purpose and Pursue Your God-Given Call to CreateRating: 5 out of 5 stars5/5 (33)

- Summary of The 33 Strategies of War by Robert GreeneFrom EverandSummary of The 33 Strategies of War by Robert GreeneRating: 3.5 out of 5 stars3.5/5 (20)

- Startup: How To Create A Successful, Scalable, High-Growth Business From ScratchFrom EverandStartup: How To Create A Successful, Scalable, High-Growth Business From ScratchRating: 4 out of 5 stars4/5 (114)

- Creating Competitive Advantage: How to be Strategically Ahead in Changing MarketsFrom EverandCreating Competitive Advantage: How to be Strategically Ahead in Changing MarketsRating: 5 out of 5 stars5/5 (2)

- Level Up: How to Get Focused, Stop Procrastinating, and Upgrade Your LifeFrom EverandLevel Up: How to Get Focused, Stop Procrastinating, and Upgrade Your LifeRating: 5 out of 5 stars5/5 (22)

- Anything You Want: 40 lessons for a new kind of entrepreneurFrom EverandAnything You Want: 40 lessons for a new kind of entrepreneurRating: 5 out of 5 stars5/5 (46)

- Without a Doubt: How to Go from Underrated to UnbeatableFrom EverandWithout a Doubt: How to Go from Underrated to UnbeatableRating: 4 out of 5 stars4/5 (23)

- Summary of The Four Agreements: A Practical Guide to Personal Freedom (A Toltec Wisdom Book) by Don Miguel RuizFrom EverandSummary of The Four Agreements: A Practical Guide to Personal Freedom (A Toltec Wisdom Book) by Don Miguel RuizRating: 4.5 out of 5 stars4.5/5 (112)

- Enough: The Simple Path to Everything You Want -- A Field Guide for Perpetually Exhausted EntrepreneursFrom EverandEnough: The Simple Path to Everything You Want -- A Field Guide for Perpetually Exhausted EntrepreneursRating: 5 out of 5 stars5/5 (24)