You might also like

- A B C D of E-BankingDocument75 pagesA B C D of E-Bankinglove tannaNo ratings yet

- Extras BancaDocument2 pagesExtras BancaAltomi AlexNo ratings yet

- Compensation in Banking SectorDocument18 pagesCompensation in Banking SectorShashank100% (9)

- Mobile Financial Services (MFS) : Agent Banking DepartmentDocument79 pagesMobile Financial Services (MFS) : Agent Banking DepartmentdawitNo ratings yet

- EIB Working Papers 2019/01 - Blockchain, FinTechs: and their relevance for international financial institutionsFrom EverandEIB Working Papers 2019/01 - Blockchain, FinTechs: and their relevance for international financial institutionsNo ratings yet

- Core BankingDocument37 pagesCore Bankingnwani25No ratings yet

- A Strategic Analysis On Digital Banking With Reference To HDFC BankDocument63 pagesA Strategic Analysis On Digital Banking With Reference To HDFC Bankjoju felixNo ratings yet

- Fintech 400 PDFDocument410 pagesFintech 400 PDFHarshil MehtaNo ratings yet

- Design and Implementation of Mobile Banking SystemDocument25 pagesDesign and Implementation of Mobile Banking SystemAyoola OladojaNo ratings yet

- 3 - Mobile Banking Case StudyDocument7 pages3 - Mobile Banking Case StudyDevspringNo ratings yet

- Bringing Smart Policies To Life The Basics: Mobile Phone Financial ServicesDocument15 pagesBringing Smart Policies To Life The Basics: Mobile Phone Financial ServicesRaja KarthikNo ratings yet

- Xavier Institute of Management, Bhubaneswar: M-Banking: Does It Have Potential?Document27 pagesXavier Institute of Management, Bhubaneswar: M-Banking: Does It Have Potential?Neetesh SinghNo ratings yet

- Electronic and Mobile BankingDocument19 pagesElectronic and Mobile BankingBilal Malick100% (1)

- Drivers and Technology - MOBDocument4 pagesDrivers and Technology - MOBSehgal AnkitNo ratings yet

- Fintech Services For Banks in KP - in Order of PriorityDocument3 pagesFintech Services For Banks in KP - in Order of PriorityHassan Sarfraz AliNo ratings yet

- 1.TNASDC DBF Paper IV Module A Unit 1,2 and 3Document18 pages1.TNASDC DBF Paper IV Module A Unit 1,2 and 3dhanushtrack3No ratings yet

- Importance of Branchless Banking & Moblle Banking in PakistanDocument24 pagesImportance of Branchless Banking & Moblle Banking in PakistanDaniyal NasirNo ratings yet

- Mobile Banking and Customer SatisfactionDocument8 pagesMobile Banking and Customer SatisfactionVDC CommerceNo ratings yet

- Indian Financial SystemDocument25 pagesIndian Financial SystemgadreanuragNo ratings yet

- Banking in Technological ParadigmDocument20 pagesBanking in Technological ParadigmAtish ShrivastavaNo ratings yet

- Wells Fargo BankDocument10 pagesWells Fargo BankVandana RellanNo ratings yet

- Bnkingc CaseDocument5 pagesBnkingc CaseDishant PatelNo ratings yet

- MIS PresentationDocument14 pagesMIS Presentationgebarap913No ratings yet

- Current Scenario in IndiaDocument24 pagesCurrent Scenario in IndiaMeenuNo ratings yet

- Alternate Banking Channels For Customer ConvenienceDocument2 pagesAlternate Banking Channels For Customer ConvenienceSharon ThomasNo ratings yet

- A Study On Virtual FinanceDocument5 pagesA Study On Virtual FinanceThe Rookie GuitaristNo ratings yet

- Branchless BankingDocument45 pagesBranchless BankingZab JaanNo ratings yet

- 12 Chapter2Document36 pages12 Chapter2lucasNo ratings yet

- E BbankingDocument10 pagesE Bbankingraqa1441No ratings yet

- PPB Module 4Document38 pagesPPB Module 4RAJNo ratings yet

- Kirti Um8803 Akshita Um8103 Nisha Um8109 Shivani Um8808Document47 pagesKirti Um8803 Akshita Um8103 Nisha Um8109 Shivani Um8808Siddhant SingalNo ratings yet

- Customer Preference and Satisfaction Towards Information Technology Based Products and Services in Banking IndustryDocument45 pagesCustomer Preference and Satisfaction Towards Information Technology Based Products and Services in Banking IndustryPreethi GopalanNo ratings yet

- Increase-The Government's Encouragement To Use Electronic Wallets Has Contributed Much ToDocument3 pagesIncrease-The Government's Encouragement To Use Electronic Wallets Has Contributed Much ToMahima SharmaNo ratings yet

- Challeneges and Issues in Digital BankingDocument4 pagesChalleneges and Issues in Digital BankingHarshikaNo ratings yet

- Fin Tech 1 To 30Document428 pagesFin Tech 1 To 30Harshil MehtaNo ratings yet

- Online BankingDocument16 pagesOnline BankingParul Tyagi0% (1)

- Digital Service Provided by Banks.: Benefits of Digital BankingDocument5 pagesDigital Service Provided by Banks.: Benefits of Digital BankingAnonymous ozR9djsTSkNo ratings yet

- Retail Banking: Challenges Ahead in Distribution Channels in Urban/Rural IndiaDocument3 pagesRetail Banking: Challenges Ahead in Distribution Channels in Urban/Rural IndiaAbhay AaryanNo ratings yet

- IT in Banking SectorDocument21 pagesIT in Banking SectorShivesh AggarwalNo ratings yet

- Mobile BankingDocument61 pagesMobile Bankingvinitagupta100% (2)

- Online BankingDocument38 pagesOnline BankingROSHNI AZAMNo ratings yet

- Ibm MicrofinanceDocument12 pagesIbm MicrofinanceRumba Guaguancò100% (1)

- Mobile BankingDocument80 pagesMobile BankingadilsyedNo ratings yet

- Banking Law Project Sakshi DagurDocument16 pagesBanking Law Project Sakshi DagurBharat Joshi100% (1)

- AbhayDocument30 pagesAbhayAbhay MalikNo ratings yet

- Types of Retail BankingDocument2 pagesTypes of Retail Bankingbeena antuNo ratings yet

- What Is 'Payments Banks'Document3 pagesWhat Is 'Payments Banks'Antas KumarNo ratings yet

- Mobile Banking: To Meet Wikipedia's - PleaseDocument11 pagesMobile Banking: To Meet Wikipedia's - PleaseVinayak RajanNo ratings yet

- CHAPTER ONE - FiveDocument21 pagesCHAPTER ONE - FiveFira ManNo ratings yet

- Mobile Banking PolicyDocument12 pagesMobile Banking PolicySuraj GCNo ratings yet

- Banking Products and Operations: Session 6Document30 pagesBanking Products and Operations: Session 6Vaidyanathan RavichandranNo ratings yet

- Mobile Banking Products and Rural India: An Evaluation: Peter JohnDocument5 pagesMobile Banking Products and Rural India: An Evaluation: Peter JohnkarthickNo ratings yet

- BM Notes (Modern Banking)Document28 pagesBM Notes (Modern Banking)Ranvir SinghNo ratings yet

- Open & Neo BankingDocument17 pagesOpen & Neo BankingSHUBHAM DIXITNo ratings yet

- Mobile BankingDocument45 pagesMobile BankingTamal MukherjeeNo ratings yet

- Convergence of Mobile Banking, Financial Inclusion and Consumer Protection-TrendDocument3 pagesConvergence of Mobile Banking, Financial Inclusion and Consumer Protection-TrendCiocoiu Vlad AndreiNo ratings yet

- Fin TechDocument32 pagesFin Techkritigupta.may1999No ratings yet

- Executive Summary: Mobile BankingDocument48 pagesExecutive Summary: Mobile Bankingzillurr_11No ratings yet

- Unleashing E-commerce Potential : Harnessing the Power of Digital MarketingFrom EverandUnleashing E-commerce Potential : Harnessing the Power of Digital MarketingNo ratings yet

- Dhanya ProjectDocument41 pagesDhanya ProjectVenki GajaNo ratings yet

- E Proforma - 2022-09-19T104945.433-16Document2 pagesE Proforma - 2022-09-19T104945.433-16vinay.nimmala2000No ratings yet

- Case of ICICI and Bank of Madura MergerDocument6 pagesCase of ICICI and Bank of Madura MergerAkash SinghNo ratings yet

- Accounting For Banking InstitutionsDocument45 pagesAccounting For Banking InstitutionsNchendeh ChristianNo ratings yet

- 549 The Revised Rules of The Ethiopia Commodity ExchangeDocument107 pages549 The Revised Rules of The Ethiopia Commodity ExchangeKumera HaileyesusNo ratings yet

- Maharashtra State Electricity Distribution Co. LTD.: Bill of Supply For The Month of Jun 2021Document3 pagesMaharashtra State Electricity Distribution Co. LTD.: Bill of Supply For The Month of Jun 2021Gayatri AtishNo ratings yet

- Au Digital Savings AccountDocument5 pagesAu Digital Savings AccountQuaint ZoneNo ratings yet

- Economics Upsc 2021Document18 pagesEconomics Upsc 2021Pulkit MalikNo ratings yet

- Swiss Banking Confidentiality: Perceptions vs. RealityDocument20 pagesSwiss Banking Confidentiality: Perceptions vs. RealityApiez ZiepaNo ratings yet

- NRIHOMELOAN - Application FormDocument9 pagesNRIHOMELOAN - Application FormgrgcharyNo ratings yet

- Swift MT940 DocDocument27 pagesSwift MT940 DocGNV Engg ServicesNo ratings yet

- GW 2013 Arab World Sample PagesDocument9 pagesGW 2013 Arab World Sample PagesAlaaNo ratings yet

- RTI AccountingManual PDFDocument459 pagesRTI AccountingManual PDFVanita ValluvanNo ratings yet

- Brochure For Symbiosis College of Arts and Commerce - PuneDocument72 pagesBrochure For Symbiosis College of Arts and Commerce - Puneglorubaby2007No ratings yet

- Profile S.Banerjee FDocument4 pagesProfile S.Banerjee FabhishekatupesNo ratings yet

- Know About Swiss Bank AccountDocument3 pagesKnow About Swiss Bank AccountJain DanendraNo ratings yet

- Zaid Hamid: Famous Economic Terrorism Book !!! (English)Document200 pagesZaid Hamid: Famous Economic Terrorism Book !!! (English)Sabeqoon Wal Awaloon90% (10)

- Ung Systems Corp: A Customized Summary of Your Visit April 15, 2021Document2 pagesUng Systems Corp: A Customized Summary of Your Visit April 15, 2021lionel mazzottaNo ratings yet

- Actuary India April 2015Document28 pagesActuary India April 2015rahulrajeshanandNo ratings yet

- Full Download Financial Accounting 4th Edition Kemp Test BankDocument14 pagesFull Download Financial Accounting 4th Edition Kemp Test Bankelizabethrotner100% (23)

- Cover Letter Example For Bank JobDocument8 pagesCover Letter Example For Bank Jobafiwhwlwx100% (2)

- The Rise and Fall of Banco FilipinoDocument7 pagesThe Rise and Fall of Banco FilipinoJaypee JavierNo ratings yet

- Conwi vs. Court of Tax Appeals, 213 SCRA 83, August 31, 1992Document14 pagesConwi vs. Court of Tax Appeals, 213 SCRA 83, August 31, 1992Jane BandojaNo ratings yet

- Prospect and Challenges of E-Banking (In Case of Dashen Bank Halaba Branch)Document57 pagesProspect and Challenges of E-Banking (In Case of Dashen Bank Halaba Branch)Fikru Tesefaye100% (1)

- Trevor Blevin Case ScenarioDocument4 pagesTrevor Blevin Case ScenarioJeffrey Quan NgoNo ratings yet

- Dissertation On Internet Banking in IndiaDocument8 pagesDissertation On Internet Banking in IndiaOrderAPaperBillings100% (1)

- Application - Form - Car LoanDocument6 pagesApplication - Form - Car LoanSanjay SolankiNo ratings yet

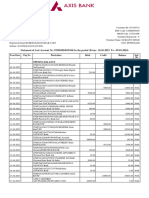

- Account STMT XX5184 09012024Document7 pagesAccount STMT XX5184 09012024Praveen SainiNo ratings yet