You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (843)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Travel Insurance Final Project Yash NaikDocument57 pagesTravel Insurance Final Project Yash NaikVedant Mahajan80% (5)

- Federal Urdu University of Arts, Science and Technology, IslamabadDocument5 pagesFederal Urdu University of Arts, Science and Technology, IslamabadQasim Jahangir WaraichNo ratings yet

- Republic Act No. 9182Document1 pageRepublic Act No. 9182Leogen TomultoNo ratings yet

- Accum. Depreciation, Fur. & Fixture Merchandise Inventory Furniture & FixtureDocument6 pagesAccum. Depreciation, Fur. & Fixture Merchandise Inventory Furniture & FixtureJoana TrinidadNo ratings yet

- COSO Framework BANKDocument15 pagesCOSO Framework BANKFahmi Nur AlfiyanNo ratings yet

- JK FD Form 2018 Final 20th May Final 30082018Document6 pagesJK FD Form 2018 Final 20th May Final 30082018Prabhat KumarNo ratings yet

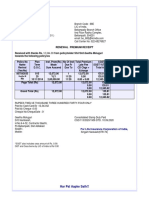

- Renewal Premium Receipt: Har Pal Aapke Sath!!Document1 pageRenewal Premium Receipt: Har Pal Aapke Sath!!krishna krishNo ratings yet

- Employee Benefits TheoryDocument8 pagesEmployee Benefits TheoryMicaela EncinasNo ratings yet

- Corporate Finance 2 SyllabusDocument11 pagesCorporate Finance 2 SyllabusMai NguyenNo ratings yet

- Merchant BankingDocument24 pagesMerchant BankingSweety PawarNo ratings yet

- Cir Pac1163Document4 pagesCir Pac1163NUR AISYAH BINTINISWADI (BG)No ratings yet

- Presentation On Government (Gilt Edged) SecuritiesDocument22 pagesPresentation On Government (Gilt Edged) Securitieshiteshnandwana100% (1)

- ISA 510 MindMapDocument1 pageISA 510 MindMapA R AdILNo ratings yet

- FINANCIAL RATIOS Isb535Document3 pagesFINANCIAL RATIOS Isb535NAJWA SUHA BINTI SELAMAT NAJWA SUHA BINTI SELAMATNo ratings yet

- Areza vs. Express Savings Bank DIVINAGRACIADocument1 pageAreza vs. Express Savings Bank DIVINAGRACIAAngelica Joyce Belen100% (1)

- EMI Calculator ExcelDocument20 pagesEMI Calculator ExcelSheru Shri100% (1)

- Opening Bank Accounts in The Name of MinorsDocument2 pagesOpening Bank Accounts in The Name of MinorsBiswajit DasNo ratings yet

- 830pm 50.epra Journals-5705Document7 pages830pm 50.epra Journals-5705DedipyaNo ratings yet

- International Financial Reporting Standards An Introduction 3rd Edition Needles Test BankDocument8 pagesInternational Financial Reporting Standards An Introduction 3rd Edition Needles Test BankJenniferThompsongoacm100% (15)

- Pliant Therapeutics: BEACON Lights The Way Forward While Initial PSC Data Comes Into View 2Q Takeaways & Model UpdateDocument10 pagesPliant Therapeutics: BEACON Lights The Way Forward While Initial PSC Data Comes Into View 2Q Takeaways & Model Updatemengfanqi1996No ratings yet

- Accounting Cycle of A Service Business: Mr. Jan CupangDocument30 pagesAccounting Cycle of A Service Business: Mr. Jan Cupangbanigx0xNo ratings yet

- Chapter 4 Investment Appraisal Methods 2Document62 pagesChapter 4 Investment Appraisal Methods 2JesterdanceNo ratings yet

- Application Form For Personal LoanDocument10 pagesApplication Form For Personal LoanAshok KumarNo ratings yet

- Engagementletter TPDocument3 pagesEngagementletter TPDonna Mae SingsonNo ratings yet

- Chapter 2 #20Document3 pagesChapter 2 #20spp50% (2)

- Absurd Monetary SystemDocument3 pagesAbsurd Monetary SystemMubashir HassanNo ratings yet

- TRƯƠNG THỊ QUỲNH NHƯ - ESSAY TEST - - ACC101 - IB17CDocument15 pagesTRƯƠNG THỊ QUỲNH NHƯ - ESSAY TEST - - ACC101 - IB17CTrương Thị Quỳnh NhưNo ratings yet

- Rates of Bonus Per 1000 Sum AssuredDocument3 pagesRates of Bonus Per 1000 Sum AssuredDeepansh TyagiNo ratings yet

- Comparative Study of Brokerage Plans of Religare Securities Ltd. With Various Brokerage Firms-1Document83 pagesComparative Study of Brokerage Plans of Religare Securities Ltd. With Various Brokerage Firms-1vibhatiwari31No ratings yet

- Principles of Accounting, Volume 1: Financial Accounting: Chapter 16 Statement of Cash FlowsDocument53 pagesPrinciples of Accounting, Volume 1: Financial Accounting: Chapter 16 Statement of Cash FlowsAdam Andrew OngNo ratings yet