You might also like

- SSP04 Goal Achievement ExercisesDocument26 pagesSSP04 Goal Achievement ExercisesMicaela Encinas100% (1)

- Reviewer ToaDocument25 pagesReviewer ToaFlorence CuansoNo ratings yet

- IFRS Guidebook - 2019 Edition (2018, AccountingTools, Inc.) Steven M. BraggDocument508 pagesIFRS Guidebook - 2019 Edition (2018, AccountingTools, Inc.) Steven M. Braggal chemiste100% (7)

- 2020-2021 Pre-Week Labor NotesDocument47 pages2020-2021 Pre-Week Labor NotesWinnieNo ratings yet

- Quiz 3 Finals Employee Benefits PDFDocument4 pagesQuiz 3 Finals Employee Benefits PDFIllion IllionNo ratings yet

- (Use The Below Problem To Answers The Succeeding Four (4) Questions.)Document3 pages(Use The Below Problem To Answers The Succeeding Four (4) Questions.)admiral spongebobNo ratings yet

- Toaz - Info Ia201 Intermediate Accounting 2 PRDocument203 pagesToaz - Info Ia201 Intermediate Accounting 2 PRZJ GarciaNo ratings yet

- Right of Use Asset AccountingDocument22 pagesRight of Use Asset AccountingQueen ValleNo ratings yet

- Solution and AnswerDocument4 pagesSolution and AnswerMicaela EncinasNo ratings yet

- Collective Labour Law Tutorial LetterDocument37 pagesCollective Labour Law Tutorial LetterDNo ratings yet

- Project Report On Performance ManagmentDocument5 pagesProject Report On Performance ManagmentClarissa AntaoNo ratings yet

- Resignation Letter SampleDocument9 pagesResignation Letter SampleifyjoslynNo ratings yet

- Business CommunicationDocument13 pagesBusiness CommunicationThomas ChowNo ratings yet

- NGC1 Flash Cards 1Document10 pagesNGC1 Flash Cards 1Kevin Josh BonalesNo ratings yet

- The University of Manila College of Business Administration and Accountacy Integrated CPA Review and Refresher Program Pre-Final Examination AE 16Document5 pagesThe University of Manila College of Business Administration and Accountacy Integrated CPA Review and Refresher Program Pre-Final Examination AE 16ana rosemarie enaoNo ratings yet

- Book Value Per Share and Earnings Per Share Book Value Per ShareDocument23 pagesBook Value Per Share and Earnings Per Share Book Value Per Share132345usdfghjNo ratings yet

- Reviewer For Mid Term ExamDocument12 pagesReviewer For Mid Term ExamJannelle SalacNo ratings yet

- Midterm Review QuestionsDocument19 pagesMidterm Review Questionschiji chzzzmeowNo ratings yet

- DocxDocument5 pagesDocxJohn Vincent CruzNo ratings yet

- Quiz 3Document3 pagesQuiz 3Mon RamNo ratings yet

- The Purpose of An Interperiod Income Tax Allocation Is ToDocument2 pagesThe Purpose of An Interperiod Income Tax Allocation Is ToAllen Kate100% (1)

- This Study Resource Was: Assessment Task 3Document5 pagesThis Study Resource Was: Assessment Task 3maria evangelistaNo ratings yet

- Premium & Warranty LiabilitiesDocument16 pagesPremium & Warranty LiabilitiesKring Zel0% (1)

- This Study Resource Was: Academic Council'S The LobbyDocument4 pagesThis Study Resource Was: Academic Council'S The LobbyMicaela EncinasNo ratings yet

- Pfrs 14: Regulatory Deferral AccountsDocument5 pagesPfrs 14: Regulatory Deferral AccountsLALALA LULULUNo ratings yet

- Provision, With Solved Tutorial Question and Briefly ConceptDocument17 pagesProvision, With Solved Tutorial Question and Briefly ConceptSamson KilatuNo ratings yet

- Property, Plant and Equipment DepreciationDocument13 pagesProperty, Plant and Equipment DepreciationJannelle SalacNo ratings yet

- Prelim Exam - Intermediate AccountingDocument4 pagesPrelim Exam - Intermediate AccountingLea Gabrielle Fariola0% (1)

- Leases ExamDocument12 pagesLeases ExamallyssajabsNo ratings yet

- TAX2 ReyesDocument9 pagesTAX2 ReyesClaire BarrettoNo ratings yet

- Discussion Problems With SolutionsDocument9 pagesDiscussion Problems With SolutionsRaveeda AnwarNo ratings yet

- Direct Financing Lease Bafacr4x OnlineglimpsenujpiaDocument4 pagesDirect Financing Lease Bafacr4x OnlineglimpsenujpiaAga Mathew MayugaNo ratings yet

- Gbermic 11-12Document13 pagesGbermic 11-12Paolo Niel ArenasNo ratings yet

- Employee Benefits ChapterDocument11 pagesEmployee Benefits ChapterJM Valonda Villena, CPA, MBANo ratings yet

- 9TH Bonds Payable Part IIDocument8 pages9TH Bonds Payable Part IIAnthony DyNo ratings yet

- CFASDocument4 pagesCFASBruce Devin Pabayos SolanoNo ratings yet

- Easy Problem Chapter 5Document5 pagesEasy Problem Chapter 5Natally LangfeldtNo ratings yet

- Notes For Civil Code Article 1177 and Article 1178Document5 pagesNotes For Civil Code Article 1177 and Article 1178Chasz CarandangNo ratings yet

- Pre-3 Mari HandoutsDocument10 pagesPre-3 Mari HandoutsEmerlyn Charlotte FonteNo ratings yet

- Simulates Midterm Exam. IntAcc1 PDFDocument11 pagesSimulates Midterm Exam. IntAcc1 PDFA NuelaNo ratings yet

- Compound Financial Instruments and Note PayableDocument4 pagesCompound Financial Instruments and Note PayablePaula Rodalyn MateoNo ratings yet

- Quiz-Review CfasDocument5 pagesQuiz-Review CfasMa Louise Ivy RosalesNo ratings yet

- Chapter 22--Budgeting FundamentalsDocument94 pagesChapter 22--Budgeting FundamentalsAngely May Jordan100% (1)

- P 1Document4 pagesP 1Kenneth Bryan Tegerero TegioNo ratings yet

- Bam 242 - P2 Examination - (Part 1) : I. Multiple Choice Questions. 1 Point EachDocument20 pagesBam 242 - P2 Examination - (Part 1) : I. Multiple Choice Questions. 1 Point EachRosemarie VillanuevaNo ratings yet

- Chapter 18 Government GrantsDocument6 pagesChapter 18 Government Grantsalexandra rausaNo ratings yet

- 8 Wasting Assets PDFDocument2 pages8 Wasting Assets PDFGayle LalloNo ratings yet

- Accounting Quiz with 31 Multiple Choice QuestionsDocument9 pagesAccounting Quiz with 31 Multiple Choice Questionsmarites yuNo ratings yet

- Leases Part 3 - Other Accounting IssuesDocument33 pagesLeases Part 3 - Other Accounting IssuesDanica RamosNo ratings yet

- Chapter 15,16, & 17 IA Valix Sales Type LeaseDocument15 pagesChapter 15,16, & 17 IA Valix Sales Type LeaseMiko ArniñoNo ratings yet

- CASESTUDYXWISKWDKDocument9 pagesCASESTUDYXWISKWDKShaira Mae E. PacisNo ratings yet

- Quiz in Shareholders' EquityDocument12 pagesQuiz in Shareholders' EquityYou're WelcomeNo ratings yet

- Corporate Governance Repsonsibilities and Accountabilities: Answer To QuestionsDocument2 pagesCorporate Governance Repsonsibilities and Accountabilities: Answer To QuestionsFaith MarasiganNo ratings yet

- AFAR06-01 Partnership AccountingDocument8 pagesAFAR06-01 Partnership AccountingEd MendozaNo ratings yet

- Our Lady of The Pillar College - CauayanDocument5 pagesOur Lady of The Pillar College - CauayanLu CioNo ratings yet

- Module 5 Note Payable and Debt RestructureDocument15 pagesModule 5 Note Payable and Debt Restructuremmh100% (1)

- Chapter 5-The Statement of Cash Flows: Multiple ChoiceDocument29 pagesChapter 5-The Statement of Cash Flows: Multiple ChoiceJoebin Corporal LopezNo ratings yet

- Cae05-Chapter 4 Notes Receivables & Payable Problem DiscussionDocument12 pagesCae05-Chapter 4 Notes Receivables & Payable Problem DiscussionSteffany RoqueNo ratings yet

- Quiz - Chapter 4 - Partnership Liquidation - 2021 EditionDocument7 pagesQuiz - Chapter 4 - Partnership Liquidation - 2021 EditionYam SondayNo ratings yet

- Contract of Sale Elements and StagesDocument8 pagesContract of Sale Elements and StagesJanaisa BugayongNo ratings yet

- Intacc 3 Leases FinalsDocument9 pagesIntacc 3 Leases FinalsDarryl AgustinNo ratings yet

- Requirement: Determine The Financial Liabilities To Be Disclosed in The NotesDocument4 pagesRequirement: Determine The Financial Liabilities To Be Disclosed in The NotesInvisible CionNo ratings yet

- STRATEGIC MANAGEMENT RESOURCE AUDITINGDocument10 pagesSTRATEGIC MANAGEMENT RESOURCE AUDITINGSteffany RoqueNo ratings yet

- Philippine Financial Reporting Standards 16 Leases (PFRS 16)Document3 pagesPhilippine Financial Reporting Standards 16 Leases (PFRS 16)Queen ValleNo ratings yet

- Valix 17 20 MCQ and Theory Emp Ben She PDFDocument48 pagesValix 17 20 MCQ and Theory Emp Ben She PDFMitchie FaustinoNo ratings yet

- EMPLOYEE BENEFITS THEORY EXPLAINEDDocument3 pagesEMPLOYEE BENEFITS THEORY EXPLAINEDTracy Ann Acedillo100% (1)

- PAS 19 - Employee Benefits & PAS 26 - Reporting and Accounting For Retirement Benefit PlanDocument6 pagesPAS 19 - Employee Benefits & PAS 26 - Reporting and Accounting For Retirement Benefit Pland.pagkatoytoyNo ratings yet

- EB Handouts 1Document4 pagesEB Handouts 1John Vicente BalanquitNo ratings yet

- Employee Benefits Quiz Module 4Document1 pageEmployee Benefits Quiz Module 4Ronnah Mae FloresNo ratings yet

- Final Term Synchronous Task: Multiple Choice QuestionsDocument8 pagesFinal Term Synchronous Task: Multiple Choice Questionsrachel banana hammockNo ratings yet

- This Study Resource Was: Academic Council'S The LobbyDocument4 pagesThis Study Resource Was: Academic Council'S The LobbyMicaela EncinasNo ratings yet

- Controlling Fuse Production Quality with SPCDocument22 pagesControlling Fuse Production Quality with SPCMicaela EncinasNo ratings yet

- Managerial Economics ECON 1Document26 pagesManagerial Economics ECON 1Micaela EncinasNo ratings yet

- Ge3 MathDocument111 pagesGe3 MathMicaela Encinas100% (1)

- Understanding the Philosophical Views of SelfDocument93 pagesUnderstanding the Philosophical Views of SelfMicaela EncinasNo ratings yet

- Formula:: Fair Value of Plan Assets, Beginning XXXDocument2 pagesFormula:: Fair Value of Plan Assets, Beginning XXXMicaela EncinasNo ratings yet

- ACCTG Employee-BenefitDocument2 pagesACCTG Employee-BenefitMicaela EncinasNo ratings yet

- Ada1930b PDFDocument131 pagesAda1930b PDFhambog kasiNo ratings yet

- Calculate simple interest rates, amounts, and time periodsDocument3 pagesCalculate simple interest rates, amounts, and time periodsMicaela EncinasNo ratings yet

- ENVSCI FUNDAMENTALSDocument79 pagesENVSCI FUNDAMENTALSMicaela EncinasNo ratings yet

- Understanding The Self..... PRELIM GE1Document112 pagesUnderstanding The Self..... PRELIM GE1Micaela Encinas100% (1)

- NSTP PrelimDocument57 pagesNSTP PrelimCrystal AlcantaraNo ratings yet

- Purposive Communication: Corazon F. RubioDocument46 pagesPurposive Communication: Corazon F. RubioMicaela EncinasNo ratings yet

- Evaluation Entrep Mod1Document1 pageEvaluation Entrep Mod1Micaela EncinasNo ratings yet

- Ge2 HistoryDocument64 pagesGe2 HistoryMicaela EncinasNo ratings yet

- Conceptual Framework and Accounting Standards: Marian G. Magcalas, CPA, MBADocument120 pagesConceptual Framework and Accounting Standards: Marian G. Magcalas, CPA, MBAMicaela Encinas100% (1)

- National Service Training Program Civic Welfare Training Service 1Document54 pagesNational Service Training Program Civic Welfare Training Service 1Micaela EncinasNo ratings yet

- Fitness: Marty R. ValeroDocument31 pagesFitness: Marty R. ValeroMicaela EncinasNo ratings yet

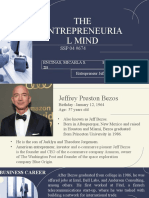

- THE Entrepreneuria L Mind: Encinas, Micaela S. Bsa-2B Entrepreneur Jeff BezosDocument13 pagesTHE Entrepreneuria L Mind: Encinas, Micaela S. Bsa-2B Entrepreneur Jeff BezosMicaela EncinasNo ratings yet

- Fin 2 PDFDocument48 pagesFin 2 PDFMicaela Encinas0% (1)

- Accounting 4 Premiums, Warranties and Deferred RevenuesDocument2 pagesAccounting 4 Premiums, Warranties and Deferred RevenuesMicaela EncinasNo ratings yet

- Accounting 4 Module 1 3Document3 pagesAccounting 4 Module 1 3Micaela EncinasNo ratings yet

- Basic Financial Accounting and Reporting: Ishmael Y. Reyes, CPADocument32 pagesBasic Financial Accounting and Reporting: Ishmael Y. Reyes, CPAMicaela EncinasNo ratings yet

- Accounting 4 Provisions and ContingenciesDocument4 pagesAccounting 4 Provisions and ContingenciesMicaela EncinasNo ratings yet

- Quantitative MethodsDocument19 pagesQuantitative MethodsSerena Van der WoodsenNo ratings yet

- Disciplinary and Grievance Procedures CodeDocument9 pagesDisciplinary and Grievance Procedures Codemuna1990No ratings yet

- Civilspedia: ...... Current Affairs Digital LibraryDocument21 pagesCivilspedia: ...... Current Affairs Digital LibraryShankar IASNo ratings yet

- HRM Week 2Document18 pagesHRM Week 2doll3kittenNo ratings yet

- Case Study NINJA VANDocument16 pagesCase Study NINJA VANLancequeen RhoseNo ratings yet

- July 2011 NLE Room Assignments (Davaol)Document215 pagesJuly 2011 NLE Room Assignments (Davaol)dericNo ratings yet

- Management Essays - Leadership and ManagementDocument4 pagesManagement Essays - Leadership and ManagementHND Assignment HelpNo ratings yet

- City of Jacksonville: Executive Order Employment ComplaintsDocument10 pagesCity of Jacksonville: Executive Order Employment ComplaintsActionNewsJaxNo ratings yet

- CAPSTONE2022Document170 pagesCAPSTONE2022Charisse Jean PelominoNo ratings yet

- Administrative Disciplinary Rules On Sexual Harassment Cases (CSC Resolution 01-0940)Document3 pagesAdministrative Disciplinary Rules On Sexual Harassment Cases (CSC Resolution 01-0940)Jerome AzarconNo ratings yet

- Final Barpeta NASand WSReport 30 JulyDocument118 pagesFinal Barpeta NASand WSReport 30 JulyC00LE0No ratings yet

- University Malaysia Kelantan (UMK) : Course NameDocument18 pagesUniversity Malaysia Kelantan (UMK) : Course NameshobuzfeniNo ratings yet

- 151 DyDir ESIC Intv Eng 19062023Document9 pages151 DyDir ESIC Intv Eng 19062023KashishNo ratings yet

- Nurising Assignment ConflictDocument10 pagesNurising Assignment ConflictLauren KalantaNo ratings yet

- Aligarh Muslim University: Sociology-III Topic-Concept of PovertyDocument10 pagesAligarh Muslim University: Sociology-III Topic-Concept of PovertyHarendra TeotiaNo ratings yet

- 100 Questions: Identifying Research Priorities For Poverty Prevention and ReductionDocument10 pages100 Questions: Identifying Research Priorities For Poverty Prevention and ReductionCarlandrieNo ratings yet

- Offline Data EntryDocument5 pagesOffline Data EntryKetkimdNo ratings yet

- 01 - Developing A Contracting StrategyDocument67 pages01 - Developing A Contracting Strategyali deveboynuNo ratings yet

- Making Apple I pod labor lawsuitDocument2 pagesMaking Apple I pod labor lawsuitmsafer222No ratings yet

- E-Recruitment and Profitability of Selected Food and Beverage Manufacturing Firms in Lagos State, Nigeria.Document11 pagesE-Recruitment and Profitability of Selected Food and Beverage Manufacturing Firms in Lagos State, Nigeria.International Journal of Business Marketing and ManagementNo ratings yet

- TW Job Search Report MyDocument4 pagesTW Job Search Report MyMarquez, Marianne E.No ratings yet

- Preparation To The World of Work EnglishDocument5 pagesPreparation To The World of Work EnglishShreetee5656565656No ratings yet

- Application For BCCLDocument2 pagesApplication For BCCLGlobal Law FirmNo ratings yet

- Characteristics of Teachers PerformanceDocument10 pagesCharacteristics of Teachers Performancembabit leslieNo ratings yet

- How To Write and Get Paid FinalDocument110 pagesHow To Write and Get Paid FinalSam100% (1)