You might also like

- Doing Business in Canada GuideDocument104 pagesDoing Business in Canada Guidejorge rodriguezNo ratings yet

- MCQS of Business Law and TaxationDocument17 pagesMCQS of Business Law and Taxationpashadahri78680% (15)

- Medical Marijuana Business TemplatesDocument167 pagesMedical Marijuana Business TemplatesDouglas Slain100% (6)

- X-000009-1603383942652-50963-BBE - Assignment 01Document66 pagesX-000009-1603383942652-50963-BBE - Assignment 01PeuJp75% (4)

- Islamic Banking and Conventional BankingDocument4 pagesIslamic Banking and Conventional BankingSajjad AliNo ratings yet

- DocxDocument11 pagesDocxClyden Jaile RamirezNo ratings yet

- Islamic BK CH 3 PDFDocument27 pagesIslamic BK CH 3 PDFAA BB MMNo ratings yet

- First Philippine International Bank Vs CADocument29 pagesFirst Philippine International Bank Vs CABashia L. Daen-GoyenaNo ratings yet

- Diminishing Musharakah ConceptDocument26 pagesDiminishing Musharakah ConceptHasan Irfan SiddiquiNo ratings yet

- Catalan vs. Gatchalian 105 Phil. 1270Document2 pagesCatalan vs. Gatchalian 105 Phil. 1270jhammy100% (1)

- Islamic Modes of Finance: Theory and Key Shariah PrinciplesDocument5 pagesIslamic Modes of Finance: Theory and Key Shariah PrinciplesAmmar HashmiNo ratings yet

- Islamic Financing in PracticeDocument85 pagesIslamic Financing in PracticeAishiterru Gurl'sNo ratings yet

- Chap 06 - Musharaka PartnershipDocument26 pagesChap 06 - Musharaka Partnershipomair.jawaid60No ratings yet

- Musharaka Mode of Islamic BankingDocument25 pagesMusharaka Mode of Islamic BankingNaveed SaeedNo ratings yet

- Islamic Banking: Presented by Lakshmi and ShameemDocument21 pagesIslamic Banking: Presented by Lakshmi and ShameemvidyaposhakNo ratings yet

- T3 - Salient Features and ContractsDocument49 pagesT3 - Salient Features and Contractsmichael musillaNo ratings yet

- Week 6 Islamic Financing InstrumentDocument30 pagesWeek 6 Islamic Financing Instrument2 Ashlih Al TsabatNo ratings yet

- New Microsoft Word DocumentDocument7 pagesNew Microsoft Word DocumentShakikNo ratings yet

- Diminishing Musharakah Presentation 02-06-08Document32 pagesDiminishing Musharakah Presentation 02-06-08AlHuda Centre of Islamic Banking & Economics (CIBE)No ratings yet

- Problems and Their Solution in MudarabahDocument43 pagesProblems and Their Solution in Mudarabahatiqa tanveerNo ratings yet

- Shariah Compliance Framework (SCF) : Islamic BankingDocument29 pagesShariah Compliance Framework (SCF) : Islamic BankingAlHuda Centre of Islamic Banking & Economics (CIBE)No ratings yet

- Classification of Musharakahf 1 Shirkat-Ul-Milk (Partnership by Joint OwnershipDocument4 pagesClassification of Musharakahf 1 Shirkat-Ul-Milk (Partnership by Joint Ownershipmajid aliNo ratings yet

- Modes of Inv Comparative StudyDocument41 pagesModes of Inv Comparative Studyfarjana taslimNo ratings yet

- Accounting For InvestmentDocument29 pagesAccounting For InvestmentSyahrul AmirulNo ratings yet

- 19th Lecture of M.Com 4thDocument14 pages19th Lecture of M.Com 4thMuhammad BasitNo ratings yet

- Introduction To Islamic Finance: The Main Principles of Islamic Finance Are ThatDocument5 pagesIntroduction To Islamic Finance: The Main Principles of Islamic Finance Are ThatMariam NzNo ratings yet

- Islamic BankingDocument3 pagesIslamic BankingsallyNo ratings yet

- Islamic Financial ProductDocument13 pagesIslamic Financial ProductKelvin Lim Wei QuanNo ratings yet

- MusharakaDocument34 pagesMusharakaAbdul HafeezNo ratings yet

- Islamic FinanceDocument15 pagesIslamic FinanceHassaan ButtNo ratings yet

- Diminishing Musharakah MBLDocument17 pagesDiminishing Musharakah MBLUbaid ArifNo ratings yet

- Islamic Banking AssignmentDocument6 pagesIslamic Banking Assignmentomair.jawaid60No ratings yet

- ISBF NotesDocument13 pagesISBF Notesmuneebmateen01No ratings yet

- Diminishing Musharakah: Mahmood ShafqatDocument32 pagesDiminishing Musharakah: Mahmood ShafqatAli KhanNo ratings yet

- Meezan Bank PresentationDocument17 pagesMeezan Bank PresentationHussnain RazaNo ratings yet

- Strategic FinanceDocument15 pagesStrategic FinanceSawaira QureshiNo ratings yet

- 6-DPD20032 Chapter 6 Partnership Based ContractDocument26 pages6-DPD20032 Chapter 6 Partnership Based ContractFikri Azman123No ratings yet

- Bank Al Habib Car FinanceDocument9 pagesBank Al Habib Car Financefatima rahimNo ratings yet

- Difference Between Conventional and Islamic Products AssetDocument9 pagesDifference Between Conventional and Islamic Products AssetTahir DestaNo ratings yet

- Islamic Banking Lecture 5 & 6Document33 pagesIslamic Banking Lecture 5 & 6Soban MamoonNo ratings yet

- Diminishing Musharakah - MBL - PpsDocument17 pagesDiminishing Musharakah - MBL - Ppsgul_e_sabaNo ratings yet

- The Concept of MusharakahDocument41 pagesThe Concept of MusharakahShakil KhanNo ratings yet

- Islamic Finance - Iqra UniversityDocument20 pagesIslamic Finance - Iqra UniversityalavihabibNo ratings yet

- Financial RequirementsDocument14 pagesFinancial RequirementsFiromsa DineNo ratings yet

- Ent 6Document26 pagesEnt 6workinehamanuNo ratings yet

- Sources of FinanceDocument10 pagesSources of FinanceammanagiNo ratings yet

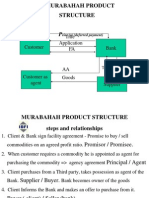

- Murabahah Product Structure: Title Application FADocument26 pagesMurabahah Product Structure: Title Application FAUmair UddinNo ratings yet

- Name: Sharmila Devi A/P Suppiah MATRIC NO: 824090 Topic 8: Islamic Capital Market Date of Submission: 29 June 2019Document32 pagesName: Sharmila Devi A/P Suppiah MATRIC NO: 824090 Topic 8: Islamic Capital Market Date of Submission: 29 June 2019Sharmila DeviNo ratings yet

- FINA 615 Islamic Financial Contracts - Mudarabah & MusharakahDocument37 pagesFINA 615 Islamic Financial Contracts - Mudarabah & MusharakahFBusinessNo ratings yet

- Diminishing Musharaka IjarahBasedDocument22 pagesDiminishing Musharaka IjarahBasedArsalan AqeeqNo ratings yet

- Lecture 6 Musharakah MutanaqisahDocument2 pagesLecture 6 Musharakah MutanaqisahGAN YU LINNo ratings yet

- Islamic Business Transaction: November 2020Document17 pagesIslamic Business Transaction: November 2020TurkuazkitchenNo ratings yet

- Basic Differences Between Conventional and Islamic BankingDocument7 pagesBasic Differences Between Conventional and Islamic BankingkaleemNo ratings yet

- Ctu ReportDocument10 pagesCtu ReportZULKIFLI BIN ELIAS MoeNo ratings yet

- Islamic Financial Products and Processes: Ameenullah SheikhDocument18 pagesIslamic Financial Products and Processes: Ameenullah SheikhhamzaNo ratings yet

- CH-6 Business FinancingDocument27 pagesCH-6 Business FinancingNatiphotography01No ratings yet

- Islamic BankingDocument17 pagesIslamic Bankingzayans84No ratings yet

- Lecture6 FinancingPart2Document29 pagesLecture6 FinancingPart2Ry NielNo ratings yet

- New Islamic Modes of Finance1Document69 pagesNew Islamic Modes of Finance1Abdul MaroofNo ratings yet

- Ch-5 Working Capital Financing of Islamic BankingDocument5 pagesCh-5 Working Capital Financing of Islamic BankingMd AzizNo ratings yet

- Investment Mode Under IB UpdatedDocument19 pagesInvestment Mode Under IB UpdatedAAM26No ratings yet

- Lec 06 - Trade Based Financing-MurabahahDocument42 pagesLec 06 - Trade Based Financing-MurabahahOmayr QureshiNo ratings yet

- Contract MuamalatDocument16 pagesContract MuamalatHarizul RafiqNo ratings yet

- Islamic Banking AssignmentDocument7 pagesIslamic Banking AssignmentFarjad AliNo ratings yet

- Islamic FinanceDocument5 pagesIslamic Financeahsand123No ratings yet

- Mahtab Sir Pres.Document30 pagesMahtab Sir Pres.afsanajahan6758No ratings yet

- Revisedon11 4th2015CIIGL&KRYLONJointVentureDocument22 pagesRevisedon11 4th2015CIIGL&KRYLONJointVenturenakarodrNo ratings yet

- Indian Partnership Act-1932Document26 pagesIndian Partnership Act-1932harrygauravNo ratings yet

- Legal Requirments of Business ManagementDocument42 pagesLegal Requirments of Business ManagementAasi RaoNo ratings yet

- 145 - Aguila JR V CADocument2 pages145 - Aguila JR V CAJai HoNo ratings yet

- Advanced Financial Accounting 1Document12 pagesAdvanced Financial Accounting 1Gemine Ailna Panganiban NuevoNo ratings yet

- ObliCon CasesDocument115 pagesObliCon CasesfuckvinaahhhNo ratings yet

- Home Assignment 1: Kathmandu University School of Management Balkumari, LalitpurDocument3 pagesHome Assignment 1: Kathmandu University School of Management Balkumari, LalitpurSulakshana DhungelNo ratings yet

- Hedge FundsDocument87 pagesHedge FundsTayebe RostamzadeNo ratings yet

- Partnership Jack and Karen Past Paper 2008Document1 pagePartnership Jack and Karen Past Paper 2008Jeremy AlexanderNo ratings yet

- BANDULA General Overview of The Law On PartnershipDocument3 pagesBANDULA General Overview of The Law On PartnershipCharena BandulaNo ratings yet

- Australia Mining Business PlamDocument23 pagesAustralia Mining Business Plamsarthak shuklaNo ratings yet

- Corporation Joint AccountsDocument6 pagesCorporation Joint AccountsNineteen AùgùstNo ratings yet

- Table Tennis Club HandbookDocument53 pagesTable Tennis Club HandbookmorvuhsNo ratings yet

- Topic 3 BUSINESS ORGANIZATIONDocument21 pagesTopic 3 BUSINESS ORGANIZATIONlolipopzeeNo ratings yet

- Granite Inn Business Plan PresentationDocument44 pagesGranite Inn Business Plan PresentationalemeNo ratings yet

- Charges Upon The CPGDocument10 pagesCharges Upon The CPGMark Anthony Javellana SicadNo ratings yet

- Bad Faith or W/ Just CauseDocument5 pagesBad Faith or W/ Just CauseGem BaguinonNo ratings yet

- Profit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership FirmDocument10 pagesProfit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership Firmd-fbuser-65596417No ratings yet

- Partnership Full CaseDocument60 pagesPartnership Full CaseNica09_forever0% (1)

- Grade 11 BSTD p2 Nov MG 2023Document34 pagesGrade 11 BSTD p2 Nov MG 2023nhlesekaneneNo ratings yet

- Choosing Business StructureDocument2 pagesChoosing Business StructurejustNo ratings yet

- Sample Project - CNET 229 Term Project Part1Document7 pagesSample Project - CNET 229 Term Project Part1Nehal GuptaNo ratings yet

- Start Here. Go Anywher E.: KPMG LawDocument21 pagesStart Here. Go Anywher E.: KPMG LawSyeda Nida AliNo ratings yet