You might also like

- Variable Absorption CostingDocument26 pagesVariable Absorption CostingSarahAdriano100% (1)

- Practical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsFrom EverandPractical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsRating: 3.5 out of 5 stars3.5/5 (3)

- Breakeven Analysis 0Document35 pagesBreakeven Analysis 0Nistha Bisht100% (1)

- Support Department Cost AllocationDocument44 pagesSupport Department Cost AllocationAwan Wibowo100% (1)

- Accounting Problems and SolutionsDocument3 pagesAccounting Problems and SolutionsKavitha Ragupathy100% (1)

- Virginia Tech ACIS Study GuideDocument10 pagesVirginia Tech ACIS Study Guidebilly bobNo ratings yet

- Chapter7 Problems MySolutionsDocument12 pagesChapter7 Problems MySolutionssindhuja21100% (1)

- Group 6 PPT CaseDocument33 pagesGroup 6 PPT CaseRavNeet KaUr100% (1)

- Akuntansi Manajaemen Chapter 15Document15 pagesAkuntansi Manajaemen Chapter 15lullasangadNo ratings yet

- CH 11 SolDocument6 pagesCH 11 SolEdson EdwardNo ratings yet

- AccountingDocument14 pagesAccountingHelpline100% (1)

- LMUmicroDocument17 pagesLMUmicroSunil CoelhoNo ratings yet

- 202E12Document16 pages202E12Ashish BhallaNo ratings yet

- Investment and BEP AnalysisDocument31 pagesInvestment and BEP AnalysisSuhadahafiza ShafieeNo ratings yet

- Short Term Decision Making: Vincent Joseph D. Disu, CPPS, MbaDocument22 pagesShort Term Decision Making: Vincent Joseph D. Disu, CPPS, MbaMaria Maganda MalditaNo ratings yet

- CH 011 AIA 5e PDFDocument7 pagesCH 011 AIA 5e PDFfaizthemeNo ratings yet

- Measurement ConceptsDocument46 pagesMeasurement ConceptsPrabal Pratap Singh TomarNo ratings yet

- SCM Sol 05 14Document14 pagesSCM Sol 05 14bloomshing0% (1)

- Activity Based CostingDocument8 pagesActivity Based CostingSaumyaNo ratings yet

- Eng Econ - Inv An N BEP - L9Document31 pagesEng Econ - Inv An N BEP - L9Ayesha RalliyaNo ratings yet

- Process Costing: This Is On The Other Side of The Continuum From Job CostingDocument28 pagesProcess Costing: This Is On The Other Side of The Continuum From Job CostingRajeev NairNo ratings yet

- WilkersonDocument4 pagesWilkersonVarun Gogia67% (3)

- Unit - 3 Cost Output RelationshipDocument11 pagesUnit - 3 Cost Output RelationshipKshitiz BhardwajNo ratings yet

- MB 112 Cost OutputDocument12 pagesMB 112 Cost OutputVeniNo ratings yet

- Lecture 9 ABC, CVP PDFDocument58 pagesLecture 9 ABC, CVP PDFShweta SridharNo ratings yet

- Solutions - Chapter 5Document12 pagesSolutions - Chapter 5Parul AbrolNo ratings yet

- CHAPTER 2 Cost Terms and PurposeDocument31 pagesCHAPTER 2 Cost Terms and PurposeRose McMahonNo ratings yet

- P10 CMA RTP Dec2013 Syl2012Document44 pagesP10 CMA RTP Dec2013 Syl2012MsKhan0078No ratings yet

- Decision Regarding Alternative ChoicesDocument29 pagesDecision Regarding Alternative ChoicesrhldxmNo ratings yet

- Lec#5 Week#5 ECODocument33 pagesLec#5 Week#5 ECOZoha MughalNo ratings yet

- ACT3110 - Introduction To CVP Analysis (S)Document30 pagesACT3110 - Introduction To CVP Analysis (S)Adani MustaffaNo ratings yet

- Lecture 6 - Full CostingDocument36 pagesLecture 6 - Full Costingmohammedakbar88No ratings yet

- Cost-Volume-Profit Analysis and Relevant CostingDocument39 pagesCost-Volume-Profit Analysis and Relevant CostingJai AceNo ratings yet

- PDFDocument3 pagesPDFTrisna KusumayantiNo ratings yet

- Chapter Five: Activity-Based Costing and Customer Profitability AnalysisDocument48 pagesChapter Five: Activity-Based Costing and Customer Profitability AnalysisSupergiant EternalsNo ratings yet

- HorngrenIMA14eSM ch13Document73 pagesHorngrenIMA14eSM ch13Piyal Hossain100% (1)

- Costs Terms, Concepts and ClassificationsDocument32 pagesCosts Terms, Concepts and Classificationsjeela1No ratings yet

- Managerial AccountingMid Term Examination (1) - CONSULTADocument7 pagesManagerial AccountingMid Term Examination (1) - CONSULTAMay Ramos100% (1)

- Benefit To Compensation Ratio CalculationsDocument6 pagesBenefit To Compensation Ratio CalculationsRamkishor PandeyNo ratings yet

- Bcom MADocument21 pagesBcom MAAbl SasankNo ratings yet

- MasDocument14 pagesMasgnim1520100% (1)

- Chapter 13 Costs Production MankiwDocument54 pagesChapter 13 Costs Production MankiwKenneth Sanchez100% (1)

- ABC-sample ProblemDocument5 pagesABC-sample ProblemLee Jap OyNo ratings yet

- Theory of Production and Costs - 5Document14 pagesTheory of Production and Costs - 5Atiqul IslamNo ratings yet

- Chapter 2 - Cost Concepts and Design EconomicsDocument54 pagesChapter 2 - Cost Concepts and Design EconomicsShayne Aira Anggong75% (4)

- Absorption & Variable CostingDocument40 pagesAbsorption & Variable CostingKaren Villafuerte100% (1)

- MAHM6e Ch04.Ab - AzDocument49 pagesMAHM6e Ch04.Ab - Azlita2703No ratings yet

- HM ch15 Variable Costing Dan Full CostingDocument20 pagesHM ch15 Variable Costing Dan Full CostingSekarNo ratings yet

- Decision Making - Relevant Costs & BenefitsDocument19 pagesDecision Making - Relevant Costs & BenefitsSujit Kumar PandaNo ratings yet

- Practice - Sensitivity and ScenarioDocument10 pagesPractice - Sensitivity and ScenariorthedthbdethNo ratings yet

- Cost of ProductionDocument79 pagesCost of ProductionMeena IyerNo ratings yet

- Managerial Accounting Sample QuestionsDocument5 pagesManagerial Accounting Sample QuestionsScholarsjunction.comNo ratings yet

- Activity Based CostingDocument10 pagesActivity Based CostingEdi Kristanta PelawiNo ratings yet

- Activity Based CostingDocument33 pagesActivity Based CostingJeetesh Kumar SinghNo ratings yet

- Business Metrics and Tools; Reference for Professionals and StudentsFrom EverandBusiness Metrics and Tools; Reference for Professionals and StudentsNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Making Your Home More Energy Efficient: A Practical Guide to Saving Your Money and Our PlanetFrom EverandMaking Your Home More Energy Efficient: A Practical Guide to Saving Your Money and Our PlanetNo ratings yet

- Distinguish Between The Following: Industry Demand and Firm (Company) Demand, AnsDocument2 pagesDistinguish Between The Following: Industry Demand and Firm (Company) Demand, AnsManish PatelNo ratings yet

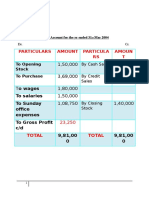

- 1,50,000 61,000 3,69,000 7,80,000 To Wages 1,80,000 1,50,000 1,08,750 1,40,000Document5 pages1,50,000 61,000 3,69,000 7,80,000 To Wages 1,80,000 1,50,000 1,08,750 1,40,000Manish PatelNo ratings yet

- Assignment ADocument1 pageAssignment AManish PatelNo ratings yet

- Solution 6Document1 pageSolution 6Manish PatelNo ratings yet

- Case Study Ans-2Document1 pageCase Study Ans-2Manish PatelNo ratings yet