You might also like

- Financial Management Chapter 2Document28 pagesFinancial Management Chapter 2beyonce0% (1)

- Chanakyaniti OdiaDocument33 pagesChanakyaniti OdiaKrushna Mishra81% (21)

- Dosha & RemedyDocument28 pagesDosha & RemedyKrushna Mishra100% (3)

- Accounting Standards.: Made By: Mba (HR I Sem) - Under The Guidance of Ma'am Vasudha KumarDocument38 pagesAccounting Standards.: Made By: Mba (HR I Sem) - Under The Guidance of Ma'am Vasudha KumarAshu SimsNo ratings yet

- FAR2 NotesDocument132 pagesFAR2 NotesCarlito DiamononNo ratings yet

- Accounting StandardsDocument45 pagesAccounting Standardsjitesh_kumar_275% (4)

- Financial ReportingDocument12 pagesFinancial ReportingAmira NajjarNo ratings yet

- Ding of Accounting Standards 1-15Document25 pagesDing of Accounting Standards 1-15Moeen MakNo ratings yet

- Presented By-:: Jai Raj Dubey A7001910099Document35 pagesPresented By-:: Jai Raj Dubey A7001910099sanjaya890No ratings yet

- FAR Notes-DoneDocument122 pagesFAR Notes-DoneJovylyn Balbines LictagNo ratings yet

- Government Accounting SummaryDocument9 pagesGovernment Accounting SummaryKenVictorino50% (2)

- Faculty Name - Sandeep Bhatiya: Financial Accounting FundamentalDocument34 pagesFaculty Name - Sandeep Bhatiya: Financial Accounting FundamentalNamrata PrasadNo ratings yet

- Questions by ILO. AccountingDocument8 pagesQuestions by ILO. AccountingIda PekkalaNo ratings yet

- Presentation ON: Understanding of Accounting Standards By:-Pritam Agarwal Abhishek AnandDocument39 pagesPresentation ON: Understanding of Accounting Standards By:-Pritam Agarwal Abhishek AnandPrakash_Tandon_583No ratings yet

- Company Law and Allied RulesDocument11 pagesCompany Law and Allied RulesFaisalNo ratings yet

- Accounting StandardsDocument44 pagesAccounting StandardsMadhu BalaNo ratings yet

- Fsa Part-3Document26 pagesFsa Part-3lakshya jainNo ratings yet

- Ale Aubrey Bsma 3 1.lguDocument6 pagesAle Aubrey Bsma 3 1.lguAstrid XiNo ratings yet

- 3accountingstandards 120704142603 Phpapp02Document37 pages3accountingstandards 120704142603 Phpapp02MehtaMilanNo ratings yet

- 3-6int 2002 Dec QDocument9 pages3-6int 2002 Dec Qadrianlee0107No ratings yet

- Arl Internship ReportDocument19 pagesArl Internship ReportChaudhry RashidNo ratings yet

- Presented By-:: Hitesh Khanna Gagandeep Kaur Gaurav Sharma Atul KoccharDocument39 pagesPresented By-:: Hitesh Khanna Gagandeep Kaur Gaurav Sharma Atul KoccharsethigaganNo ratings yet

- Simsr MMS (2010-12) Financial Management: Accounting StandardsDocument36 pagesSimsr MMS (2010-12) Financial Management: Accounting StandardsRahul GiddeNo ratings yet

- Case 2 - Acco 420Document7 pagesCase 2 - Acco 420Wasif SethNo ratings yet

- Final AccountsDocument43 pagesFinal AccountsJincy Geevarghese100% (1)

- MELC2016 NotesDocument12 pagesMELC2016 NotesChris WongNo ratings yet

- How To Elaborate A Financial StatementDocument4 pagesHow To Elaborate A Financial StatementPeligriNo ratings yet

- Account CodeDocument35 pagesAccount CodeIsha SethiNo ratings yet

- About Financial Statements: Prepared By: Mohammad Shahidul Islam MBA, ACADocument31 pagesAbout Financial Statements: Prepared By: Mohammad Shahidul Islam MBA, ACAShahid MahmudNo ratings yet

- 10 - MM - FI IntegrationDocument44 pages10 - MM - FI IntegrationAbhishek Agrawal100% (7)

- Accounting@Shortnotes (Printed)Document31 pagesAccounting@Shortnotes (Printed)IQBALNo ratings yet

- Tamam FS - 2020 - EnglishDocument27 pagesTamam FS - 2020 - EnglishDhanviper NavidadNo ratings yet

- 2009 R-3 Class Notes PDFDocument5 pages2009 R-3 Class Notes PDFAgayatak Sa ManenNo ratings yet

- Afm Research AssignmentDocument13 pagesAfm Research AssignmentNISHANo ratings yet

- Presentation ON: Understanding of Accounting StandardsDocument38 pagesPresentation ON: Understanding of Accounting StandardsaggarwalgauravNo ratings yet

- Revenue Ifrs 15Document24 pagesRevenue Ifrs 15kimuli FreddieNo ratings yet

- Purchases + Carriage Inwards + Other Expenses Incurred On Purchase of Materials - Closing Inventory of MaterialsDocument4 pagesPurchases + Carriage Inwards + Other Expenses Incurred On Purchase of Materials - Closing Inventory of MaterialsSiva SankariNo ratings yet

- Adamay International Co., Inc.: Note 1 - General InformationDocument36 pagesAdamay International Co., Inc.: Note 1 - General Informationgrecelyn bianesNo ratings yet

- NFP Assignment SolutionDocument2 pagesNFP Assignment SolutionHabte DebeleNo ratings yet

- Accounting StandardsDocument50 pagesAccounting StandardsMadhurima MitraNo ratings yet

- Comprehensive IncomeDocument20 pagesComprehensive IncomeXyzNo ratings yet

- Presentation ON: Understanding of Accounting Standards By:-Pritam Agarwal Abhishek AnandDocument38 pagesPresentation ON: Understanding of Accounting Standards By:-Pritam Agarwal Abhishek AnandAnkit GuptaNo ratings yet

- Unit 2: Finance in The Hospitality IndustryDocument4 pagesUnit 2: Finance in The Hospitality Industrychandni0810No ratings yet

- ImpairmentDocument5 pagesImpairmentRashleen AroraNo ratings yet

- Ca IfrsDocument7 pagesCa IfrsyogeshNo ratings yet

- Past Exam QuestionDocument95 pagesPast Exam Questionabsankey770No ratings yet

- Airlines Financial Reporting Implications of Covid 19Document15 pagesAirlines Financial Reporting Implications of Covid 19Rama KediaNo ratings yet

- CINDocument74 pagesCINJanki RawatNo ratings yet

- ACCT604 Week 6 Lecture SlidesDocument26 pagesACCT604 Week 6 Lecture SlidesBuddika PrasannaNo ratings yet

- Revised Schedule ViDocument8 pagesRevised Schedule ViSridharquestNo ratings yet

- Summary ValuationDocument25 pagesSummary ValuationsMNo ratings yet

- Disclaimer: © The Institute of Chartered Accountants of IndiaDocument35 pagesDisclaimer: © The Institute of Chartered Accountants of IndiajaimaakalikaNo ratings yet

- Accounting Standards (Satyanath Mohapatra)Document39 pagesAccounting Standards (Satyanath Mohapatra)smrutiranjan swain100% (1)

- As Quick PDFDocument23 pagesAs Quick PDFChandreshNo ratings yet

- Accounts Interveiw Question & AnswersDocument4 pagesAccounts Interveiw Question & Answerslitu84No ratings yet

- ACCT 4440 Class NotesDocument18 pagesACCT 4440 Class NotesadammorettoNo ratings yet

- Baf Sem 5Document8 pagesBaf Sem 5api-292680897No ratings yet

- CPA Financial Accounting and Reporting: Second EditionFrom EverandCPA Financial Accounting and Reporting: Second EditionNo ratings yet

- J.K. Lasser's Small Business Taxes 2024: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2024: Your Complete Guide to a Better Bottom LineNo ratings yet

- JK Lasser's Small Business Taxes 2010: Your Complete Guide to a Better Bottom LineFrom EverandJK Lasser's Small Business Taxes 2010: Your Complete Guide to a Better Bottom LineNo ratings yet

- Rawmaterials Inward ProcessDocument12 pagesRawmaterials Inward ProcessKrushna MishraNo ratings yet

- Workplace Conduct Policy (Discrimination, Sexual Harassment and Workplace Bullying)Document16 pagesWorkplace Conduct Policy (Discrimination, Sexual Harassment and Workplace Bullying)Krushna MishraNo ratings yet

- Candle Manufacturing Unit Budget Sl. No. Items Amounts A. TrainingDocument3 pagesCandle Manufacturing Unit Budget Sl. No. Items Amounts A. TrainingKrushna MishraNo ratings yet

- Astro DirectionDocument3 pagesAstro DirectionKrushna MishraNo ratings yet

- Health, Safety and Environment Policy: RIIL Is Committed ToDocument3 pagesHealth, Safety and Environment Policy: RIIL Is Committed ToKrushna MishraNo ratings yet

- Memorandum of AssociationDocument2 pagesMemorandum of AssociationKrushna MishraNo ratings yet

- Chapter-Ix Liabity in Special CasesDocument1 pageChapter-Ix Liabity in Special CasesKrushna MishraNo ratings yet

- Jagannatha Astakam OdiDocument2 pagesJagannatha Astakam OdiKrushna Mishra100% (3)

- Chapter-X Liability To Produce Accounts and Supply InformationDocument18 pagesChapter-X Liability To Produce Accounts and Supply InformationKrushna MishraNo ratings yet

- Odisha Entry Tax Act Schedule: Part - IIIDocument1 pageOdisha Entry Tax Act Schedule: Part - IIIKrushna MishraNo ratings yet

- VRCHP 8Document6 pagesVRCHP 8Krushna MishraNo ratings yet

- Chapter-Vii RefundDocument5 pagesChapter-Vii RefundKrushna MishraNo ratings yet

- Bedroom VastuDocument1 pageBedroom VastuKrushna MishraNo ratings yet

- Registration of Dealers, Cancellation and Amendment of Registration CertificateDocument8 pagesRegistration of Dealers, Cancellation and Amendment of Registration CertificateKrushna MishraNo ratings yet

- Jharkhand VAT Rules 2006Document53 pagesJharkhand VAT Rules 2006Krushna MishraNo ratings yet

- Vat ActDocument81 pagesVat ActKrushna MishraNo ratings yet

- Schedule B: List of Goods Subject To Value Added Tax On Turnover of Sales or PurchasesDocument29 pagesSchedule B: List of Goods Subject To Value Added Tax On Turnover of Sales or PurchasesKrushna MishraNo ratings yet

- Schedule A: (See Section 17)Document10 pagesSchedule A: (See Section 17)Krushna MishraNo ratings yet

- GanaDocument15 pagesGanaKrushna Mishra100% (1)

- Bhavani Astakam SanskritDocument1 pageBhavani Astakam SanskritKrushna MishraNo ratings yet

- Vastu For StaircaseDocument7 pagesVastu For StaircaseKrushna MishraNo ratings yet

- Rare Old Books Write by Utkalmani Gopabandhu DashDocument42 pagesRare Old Books Write by Utkalmani Gopabandhu DashKrushna MishraNo ratings yet

- On Separation and DivorceDocument13 pagesOn Separation and DivorceKrushna MishraNo ratings yet

- All Applicable YogaDocument14 pagesAll Applicable YogaKrushna MishraNo ratings yet

- Mantra For Sreegrha (Fast) Marriages and To Avoid Delays in MarriageDocument1 pageMantra For Sreegrha (Fast) Marriages and To Avoid Delays in MarriageKrushna MishraNo ratings yet

- How To Find The Direction of Your Future Spouse?Document2 pagesHow To Find The Direction of Your Future Spouse?Krushna MishraNo ratings yet

- Meena Nadi Part 1 PDFDocument67 pagesMeena Nadi Part 1 PDFvaranasilkoNo ratings yet

- Balance Sheet As at 31st March 2003Document9 pagesBalance Sheet As at 31st March 2003mpdharmadhikariNo ratings yet

- RMIT FR Week 2 Solutions PDFDocument173 pagesRMIT FR Week 2 Solutions PDFKiabu ParindaliNo ratings yet

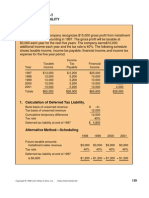

- Topic 5 - Deferred Tax A231Document57 pagesTopic 5 - Deferred Tax A231ZulhafiziNo ratings yet

- AAFR Mock Q. Paper Final (S-20)Document6 pagesAAFR Mock Q. Paper Final (S-20)Ummar FarooqNo ratings yet

- Eicher Motors 2014Document130 pagesEicher Motors 2014siva5256No ratings yet

- Financial Accounting and Reporting-IIDocument5 pagesFinancial Accounting and Reporting-IIRamzan AliNo ratings yet

- Cma Fina Group4 All MCQDocument205 pagesCma Fina Group4 All MCQtusharjaipur7No ratings yet

- SEMI-FINAL EXAM QUESTIONNAIRE (Edited)Document17 pagesSEMI-FINAL EXAM QUESTIONNAIRE (Edited)Pia De LaraNo ratings yet

- Financial Accounting and Reporting Final ExaminationDocument13 pagesFinancial Accounting and Reporting Final ExaminationBernardino PacificAce100% (1)

- Chapter 2Document90 pagesChapter 2Sky walkingNo ratings yet

- Module 4 Preparing The Financial Statements: Statement of Financial PositionDocument20 pagesModule 4 Preparing The Financial Statements: Statement of Financial PositionErine Contrano100% (3)

- CFA Level I Revision Day IIDocument138 pagesCFA Level I Revision Day IIAspanwz SpanwzNo ratings yet

- Deferred Tax IllustrationDocument8 pagesDeferred Tax IllustrationFaseeh IqbalNo ratings yet

- Reading 24 Income TaxesDocument27 pagesReading 24 Income TaxesARPIT ARYANo ratings yet

- 16 - IND AS 108 - Operating Segment Final (R)Document18 pages16 - IND AS 108 - Operating Segment Final (R)S Bharhath kumarNo ratings yet

- Cfas StodocuDocument31 pagesCfas StodocuRosemarie Cruz100% (1)

- Week 3 Tutorial Solutions - Fiancial AcountingDocument13 pagesWeek 3 Tutorial Solutions - Fiancial AcountingMi ThaiNo ratings yet

- Accounting For Income Taxes: June 6, 2020Document18 pagesAccounting For Income Taxes: June 6, 2020Andrea Marie CalmaNo ratings yet

- BMW AG Financial Statements 2022 enDocument60 pagesBMW AG Financial Statements 2022 enNitesh SinghNo ratings yet

- ITC Notes PDFDocument44 pagesITC Notes PDFAvinash KumarNo ratings yet

- C.R. Plastics - Final Proposal AssignmentDocument10 pagesC.R. Plastics - Final Proposal AssignmentShreshtha ShahNo ratings yet

- Vci 10KDocument40 pagesVci 10KpalenhoyaNo ratings yet

- Technical Interview Questions Prepared by Fahad Irfan - PDF Version 1Document4 pagesTechnical Interview Questions Prepared by Fahad Irfan - PDF Version 1Muhammad Khizzar KhanNo ratings yet

- Module 11 Current Liabilities Provisions and ContingenciesDocument14 pagesModule 11 Current Liabilities Provisions and ContingenciesZyril RamosNo ratings yet

- General Guidelines For Spreading Financial StatementsDocument8 pagesGeneral Guidelines For Spreading Financial StatementsChandan Kumar ShawNo ratings yet

- Mother of Perpetual Hel Funeral Homes: Notes To Financial StatementDocument9 pagesMother of Perpetual Hel Funeral Homes: Notes To Financial StatementSally SiaotongNo ratings yet

- Analysis of Financial StatementsDocument46 pagesAnalysis of Financial StatementsSwaroop Ranjan Baghar25% (4)

- Lecture 1Document23 pagesLecture 1John TomNo ratings yet

- Merger & Acquisitions On Tata Steel Ltd. & CorusDocument28 pagesMerger & Acquisitions On Tata Steel Ltd. & CorusFarhan100% (2)

- Exam 3Document22 pagesExam 3Darynn F. Linggon100% (2)