You might also like

- Bankers HB On Credit MGMT (Iibf)Document839 pagesBankers HB On Credit MGMT (Iibf)Prafulla Raja NishadNo ratings yet

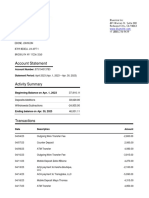

- Account Statement: Activity SummaryDocument2 pagesAccount Statement: Activity SummaryClyde ThomasNo ratings yet

- Straight Line EconomyDocument60 pagesStraight Line Economymayas40% (5)

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Caiib BFM Study Notes PDFDocument200 pagesCaiib BFM Study Notes PDFRahul Pandey100% (1)

- Caiib Questions Advanced Bank ManagementDocument3 pagesCaiib Questions Advanced Bank Managementpns988850% (2)

- Caiib Sample QuestionsDocument15 pagesCaiib Sample QuestionsVijay25% (4)

- CAIIB - Financial Management - ModuleDocument26 pagesCAIIB - Financial Management - ModuleSantosh100% (3)

- CAIIB ABM Sample Questions by Murugan PDFDocument82 pagesCAIIB ABM Sample Questions by Murugan PDFchatsak100% (7)

- Canpal Guide Caiib Series 03-17Document131 pagesCanpal Guide Caiib Series 03-17Pallab DasNo ratings yet

- Caiib Abm Case Studies - Iibf CertificationDocument244 pagesCaiib Abm Case Studies - Iibf Certificationafroz shaikNo ratings yet

- Canpal Guide Caiib Series 01-17 PDFDocument107 pagesCanpal Guide Caiib Series 01-17 PDFPallab DasNo ratings yet

- Path-Pradarshak 2023-24 EnglishDocument157 pagesPath-Pradarshak 2023-24 Englishnutandevi913585No ratings yet

- Abm CaiibDocument70 pagesAbm Caiibsubhasis123bbsrNo ratings yet

- Caiib DiscussionDocument13 pagesCaiib DiscussionRaviTuduNo ratings yet

- CreditDocument20 pagesCreditnibedita dashNo ratings yet

- CAIIB 2020 Resources EBook by K G KhullarDocument15 pagesCAIIB 2020 Resources EBook by K G KhullarArul ManikandanNo ratings yet

- Caiib Abm Case StudiesDocument241 pagesCaiib Abm Case Studieskov baghel100% (2)

- 5 6116164048049406051 PDFDocument239 pages5 6116164048049406051 PDFSreejith BhattathiriNo ratings yet

- RSKMGT Module II Credit Risk CH 1 - Introduction To Credit RiskDocument12 pagesRSKMGT Module II Credit Risk CH 1 - Introduction To Credit Riskimran khanNo ratings yet

- Iibf Caiib Elective It PDFDocument557 pagesIibf Caiib Elective It PDFPrabhat KrNo ratings yet

- JAIIB AFB Sample Questions by Murugan - For Nov 14 ExamsDocument186 pagesJAIIB AFB Sample Questions by Murugan - For Nov 14 Examsraushan_ratneshNo ratings yet

- Jaiib Made Simple Paper 1Document270 pagesJaiib Made Simple Paper 1Ashokkumar MadhaiyanNo ratings yet

- Retail Banking Sample Questions by Murugan-Dec 19 Exams PDFDocument193 pagesRetail Banking Sample Questions by Murugan-Dec 19 Exams PDFNANDHINIPRIYANo ratings yet

- Canpal Guide Caiib Series 04-17 PDFDocument185 pagesCanpal Guide Caiib Series 04-17 PDFkamalray75_188704880No ratings yet

- Memory BasedDocument12 pagesMemory BasedHari RajNo ratings yet

- BFM RecollectedDocument8 pagesBFM RecollectedGURPREET KAURNo ratings yet

- Caiib Rural Banking NotesDocument2 pagesCaiib Rural Banking NotesSatish O Manchodu100% (1)

- Iibf 1Document5 pagesIibf 1Shankar NenavathNo ratings yet

- Memorised CAIIB BFM Questions MAY 2013Document3 pagesMemorised CAIIB BFM Questions MAY 2013Pratheesh Tulsi33% (3)

- Caiib Made Simple Paper FirstDocument245 pagesCaiib Made Simple Paper FirstElse Feba PaulNo ratings yet

- CAIIB Question - TreasuryDocument12 pagesCAIIB Question - TreasuryDiwakar PasrichaNo ratings yet

- Caiib Rmmodb Nov08Document24 pagesCaiib Rmmodb Nov08Gaurav Singh100% (1)

- HDFC Bank: Housing FinanceDocument16 pagesHDFC Bank: Housing FinanceSatish VermaNo ratings yet

- Business Correspondant Model in FI-ProjectDocument51 pagesBusiness Correspondant Model in FI-ProjectcprabhashNo ratings yet

- Abm-Caiib MaterailDocument5 pagesAbm-Caiib MaterailArchanaHegdeNo ratings yet

- BFM Murugan McqsDocument34 pagesBFM Murugan McqsHanumantha Rao Turlapati100% (1)

- Caiib Paper 4 Banking Regulations and Business Laws Capsule AmbitiousDocument223 pagesCaiib Paper 4 Banking Regulations and Business Laws Capsule AmbitiouselliaCruzNo ratings yet

- Canara BankDocument18 pagesCanara BankKripa Mary JosephNo ratings yet

- Risk Management IDocument2 pagesRisk Management IMuralidhar GoliNo ratings yet

- Legal & Regulatory Aspects of BankingDocument31 pagesLegal & Regulatory Aspects of BankingKrishna HmNo ratings yet

- Jaiib - 1 Mcqs Nov 2017 MDocument108 pagesJaiib - 1 Mcqs Nov 2017 MPs PadhuNo ratings yet

- IIBFDocument8 pagesIIBFSonia ChauhanNo ratings yet

- ABM-numerical With Solutions by Neeraj AgnihotriDocument23 pagesABM-numerical With Solutions by Neeraj AgnihotriMuralidhar Goli100% (5)

- Caiib Made Simple Paper Second SKTDocument336 pagesCaiib Made Simple Paper Second SKTchdy_rahul100% (4)

- Abm Ns ToorDocument180 pagesAbm Ns Toorprashant gubrele100% (1)

- Indian Institute of Banking & Finance: Certificate Course in Digital BankingDocument6 pagesIndian Institute of Banking & Finance: Certificate Course in Digital BankingKay Aar Vee RajaNo ratings yet

- CAIIB Financial ManagementDocument40 pagesCAIIB Financial Managementmonirba48No ratings yet

- Corporate Finance: by Shubha GaneshDocument63 pagesCorporate Finance: by Shubha Ganeshdeepikachandru24No ratings yet

- Financial Management-Capital BudgetingDocument39 pagesFinancial Management-Capital BudgetingParamjit Sharma100% (53)

- Capital Budgeting Technique: Md. Nehal AhmedDocument25 pagesCapital Budgeting Technique: Md. Nehal AhmedZ Anderson Rajin0% (1)

- Incremental AnalysisDocument25 pagesIncremental AnalysisDejene HailuNo ratings yet

- Capital Budgeting and Cash FlowsDocument49 pagesCapital Budgeting and Cash FlowsArun S BharadwajNo ratings yet

- Capital BudgetingDocument33 pagesCapital BudgetingSangeetha K SNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisMobin NasimNo ratings yet

- Project AppraisalDocument62 pagesProject Appraisalsagarlakra100% (1)

- Chapter3 Project EvaluationDocument49 pagesChapter3 Project Evaluationxyz100% (1)

- Lecture 4Document43 pagesLecture 4decentdawoodNo ratings yet

- Capital Budgeting TechniquesDocument35 pagesCapital Budgeting TechniquesGaurav gusaiNo ratings yet

- Scope of Financial ManagementDocument41 pagesScope of Financial ManagementbmsoniNo ratings yet

- Capital Budgeting and Cost AnalysisDocument75 pagesCapital Budgeting and Cost AnalysisAkhil BatraNo ratings yet

- Financial Management: A Project On Capital BudgetingDocument20 pagesFinancial Management: A Project On Capital BudgetingHimanshi SethNo ratings yet

- Center List For Exam JAIIB CAIIB ElectiveDocument5 pagesCenter List For Exam JAIIB CAIIB ElectiveRahul GuptaNo ratings yet

- Bank Financial Management - CAIIB New SyllubusDocument23 pagesBank Financial Management - CAIIB New SyllubusAdi Swarup Patnaik82% (28)

- CAIIB Financial Module D MCQDocument7 pagesCAIIB Financial Module D MCQRahul GuptaNo ratings yet

- Rahul Gupta SapDocument2 pagesRahul Gupta SapRahul GuptaNo ratings yet

- Accounting & Finance Module: B: Ca R. C. JoshiDocument131 pagesAccounting & Finance Module: B: Ca R. C. JoshiRahul GuptaNo ratings yet

- Major Heads of Balance SheetDocument9 pagesMajor Heads of Balance SheetRahul GuptaNo ratings yet

- Performance Analysis of Indian Mutual Funds During PandemicDocument8 pagesPerformance Analysis of Indian Mutual Funds During PandemicEditor IJTSRDNo ratings yet

- Ratio Analysis 2Document15 pagesRatio Analysis 2Azmira RoslanNo ratings yet

- Programa Equity Portfolio ManagementDocument5 pagesPrograma Equity Portfolio ManagementJoaquin PedroNo ratings yet

- Company Valuation Based On Ev/ebitda and Ev/ebit Multiples: A Case Study of A Brazilian Mining CompanyDocument55 pagesCompany Valuation Based On Ev/ebitda and Ev/ebit Multiples: A Case Study of A Brazilian Mining CompanyRicardo AlvesNo ratings yet

- T Codes FicoDocument42 pagesT Codes FicoArjun WaniNo ratings yet

- Assignment - 1 (Capital Budgeting)Document3 pagesAssignment - 1 (Capital Budgeting)AnusreeNo ratings yet

- Accounting Theory and Analysis Chart 16 Test BankDocument14 pagesAccounting Theory and Analysis Chart 16 Test BankSonny MaciasNo ratings yet

- 616806cf0cf2b988fbcdbd97 OriginalDocument20 pages616806cf0cf2b988fbcdbd97 OriginalTM GamingNo ratings yet

- Ibs Shah Alam Main 1 31/03/22Document22 pagesIbs Shah Alam Main 1 31/03/22t52p5hdkqpNo ratings yet

- Investment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldDocument7 pagesInvestment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldMark Anthony SivaNo ratings yet

- Financial Modeling - M.chandra ShekarDocument15 pagesFinancial Modeling - M.chandra ShekarMOKSH SHREE THAKUR100% (1)

- PSO Sample Report Spring 2022Document1,002 pagesPSO Sample Report Spring 2022Mubeen AhmadNo ratings yet

- Class Work & Home Work Question of Final Account of Banking Conpany 22-23Document23 pagesClass Work & Home Work Question of Final Account of Banking Conpany 22-23DARK KING GamersNo ratings yet

- IT011A 73027326 15sep2022Document7 pagesIT011A 73027326 15sep2022Akash PraveshNo ratings yet

- Investment Analysis and Portfolio Management: G.Srianjaneyulu Rollno:18L31E0014 Mba-ADocument10 pagesInvestment Analysis and Portfolio Management: G.Srianjaneyulu Rollno:18L31E0014 Mba-Analla maheshNo ratings yet

- Develop A Clever Debt Consolidation Strategy Using These Tipssikdn PDFDocument3 pagesDevelop A Clever Debt Consolidation Strategy Using These Tipssikdn PDFbordersprout5No ratings yet

- Tutorial 3 PFPDocument6 pagesTutorial 3 PFPWinjie PangNo ratings yet

- International Financial Management: AnswerDocument18 pagesInternational Financial Management: AnswerNithyananda PatelNo ratings yet

- SYC Registration FormDocument1 pageSYC Registration Formasi_sy4christNo ratings yet

- Iron - Finance: Partial Collateralised Stablecoin On The BinancesmartchainDocument20 pagesIron - Finance: Partial Collateralised Stablecoin On The BinancesmartchainJoseNo ratings yet

- Cash Flow Statement Kotak Mahindra 2016Document80 pagesCash Flow Statement Kotak Mahindra 2016Nagireddy Kalluri100% (2)

- Sanction LetterDocument1 pageSanction LetterSanjay GuptaNo ratings yet

- Saadaoui - Moussa@Document1 pageSaadaoui - Moussa@omm berNo ratings yet

- Credit Insurance MarketDocument107 pagesCredit Insurance MarketManjunath Reddy100% (2)

- Fin 018 Problem SolvingDocument7 pagesFin 018 Problem SolvingVincenzo CassanoNo ratings yet

- Firm and Asset ValuationDocument7 pagesFirm and Asset ValuationVân TrườngNo ratings yet

- The Altman Z ScoreDocument2 pagesThe Altman Z ScoreNidhi PopliNo ratings yet