You might also like

- Cosmopolitan Singapore - July 2013 PDFDocument164 pagesCosmopolitan Singapore - July 2013 PDFdrolfxil100% (2)

- Finance Overview:: Financial Accounting (Fi)Document38 pagesFinance Overview:: Financial Accounting (Fi)Suraj MohapatraNo ratings yet

- Simulated Midterm Exam. Far1 PDFDocument11 pagesSimulated Midterm Exam. Far1 PDFDyosang BomiNo ratings yet

- The Social Security LawDocument7 pagesThe Social Security LawOtep Belciña LumabasNo ratings yet

- Appendix 3 PWC CDC Finance 16.17 - Final PDFDocument32 pagesAppendix 3 PWC CDC Finance 16.17 - Final PDFMaureen del RosarioNo ratings yet

- Finacial LiterncyDocument48 pagesFinacial LiterncyKiranNo ratings yet

- Progress ClaimsDocument43 pagesProgress ClaimsupamyNo ratings yet

- Project Report On Financial Inclusion: ContentDocument52 pagesProject Report On Financial Inclusion: ContentpawansukhijaNo ratings yet

- This Report Is To Analysis Credit Risk Management of Eastern Bank LimitedDocument30 pagesThis Report Is To Analysis Credit Risk Management of Eastern Bank Limitedশফিকুল ইসলাম লিপুNo ratings yet

- Completion of Development HLURBDocument37 pagesCompletion of Development HLURBJecky Delos ReyesNo ratings yet

- Ucp 600Document12 pagesUcp 600Usman Rajput100% (1)

- IIBF Sample BookletDocument39 pagesIIBF Sample BookletMeghalaya CSCNo ratings yet

- Financial Inclusion in India: An Analysis: Dr. Anurag B. Singh, Priyanka TandonDocument14 pagesFinancial Inclusion in India: An Analysis: Dr. Anurag B. Singh, Priyanka TandonVidhi BansalNo ratings yet

- Business Correspondent Model For Financial Inclusion-20Document47 pagesBusiness Correspondent Model For Financial Inclusion-20Naga LingamNo ratings yet

- Financial InclusionDocument75 pagesFinancial InclusionRaj KumarNo ratings yet

- Need For Financial Inclusion and Challenges Ahead - An Indian PerspectiveDocument4 pagesNeed For Financial Inclusion and Challenges Ahead - An Indian PerspectiveInternational Organization of Scientific Research (IOSR)No ratings yet

- TCS Government Whitepaper Financial Inclusion 09 2010Document26 pagesTCS Government Whitepaper Financial Inclusion 09 2010ankitrathod87No ratings yet

- Financial Inclusion: Issues and Challenges: December 2013Document7 pagesFinancial Inclusion: Issues and Challenges: December 2013Rjendra LamsalNo ratings yet

- Financial Inclusion - Issues in Measurement and Analysis: M.ShahulhameeduDocument9 pagesFinancial Inclusion - Issues in Measurement and Analysis: M.ShahulhameeduKkkkNo ratings yet

- The Role of SHGS in Financial Inclusion. A Case Study: Uma .H.R, Rupa.K.NDocument5 pagesThe Role of SHGS in Financial Inclusion. A Case Study: Uma .H.R, Rupa.K.NDevikaNo ratings yet

- 201302d Financial Inclusion India MFIsDocument15 pages201302d Financial Inclusion India MFIsCarlos105No ratings yet

- Financial Inclusion Through Microfinance Vineeta Agrawal: Applied Sciences Department, KIIT College of EngineeringDocument8 pagesFinancial Inclusion Through Microfinance Vineeta Agrawal: Applied Sciences Department, KIIT College of EngineeringVineeta AgrawalNo ratings yet

- Complete ProjectDocument72 pagesComplete ProjectKevin JacobNo ratings yet

- Micro Finance ProjectDocument38 pagesMicro Finance ProjectmanojrengarNo ratings yet

- SwabhimaanDocument30 pagesSwabhimaanswati kartikayNo ratings yet

- Evaluating Effectiveness of Channels of Financial Inclusion:-A Study On Rural OdishaDocument4 pagesEvaluating Effectiveness of Channels of Financial Inclusion:-A Study On Rural OdishaAbhishek MohantyNo ratings yet

- Financial Inclusion From BIMSDocument14 pagesFinancial Inclusion From BIMSDeepu T MathewNo ratings yet

- Financial Inclusion and Exclusion: Presented by - Group 1Document20 pagesFinancial Inclusion and Exclusion: Presented by - Group 1Amit Halder 2020-22No ratings yet

- Financial Inclusion and Exclusion: Presented by - Group 1Document20 pagesFinancial Inclusion and Exclusion: Presented by - Group 1Amit Halder 2020-22No ratings yet

- Financial Inclusion Introduction andDocument32 pagesFinancial Inclusion Introduction andAstik TripathiNo ratings yet

- Financial InclusionDocument90 pagesFinancial InclusionRohan Mehra0% (1)

- On Financial Inclusion A Must For Growth of Indian Economy: Summer Training ReportDocument44 pagesOn Financial Inclusion A Must For Growth of Indian Economy: Summer Training ReportMahey HarishNo ratings yet

- Franklin D. RooseveltDocument17 pagesFranklin D. RooseveltRupali RamtekeNo ratings yet

- Financial Inclusion. 1Document8 pagesFinancial Inclusion. 1sbbhujbalNo ratings yet

- Variation and Determinants of Financial Inclusion and Their - 2019 - IIMB ManagDocument14 pagesVariation and Determinants of Financial Inclusion and Their - 2019 - IIMB ManagWerdhi AriniNo ratings yet

- Report PHD MicrofinanceDocument201 pagesReport PHD MicrofinanceShashi Bhushan Sonbhadra100% (1)

- This Content Downloaded From 103.86.109.83 On Tue, 31 May 2022 02:29:19 UTCDocument7 pagesThis Content Downloaded From 103.86.109.83 On Tue, 31 May 2022 02:29:19 UTCsoniasharmin.pu2023octNo ratings yet

- Kalunda2 Aduda 2012 PDFDocument26 pagesKalunda2 Aduda 2012 PDFKinda AugustinNo ratings yet

- Role of Microfinance Institution in Financial InclusionDocument15 pagesRole of Microfinance Institution in Financial Inclusionswati_agarwal67No ratings yet

- Concept of Financial InclusionDocument12 pagesConcept of Financial InclusionMohitAhujaNo ratings yet

- Project Brief - Financial IncDocument37 pagesProject Brief - Financial IncLokesh BhoiNo ratings yet

- 09 - Chapter 1Document24 pages09 - Chapter 1shantishree04No ratings yet

- AEC507 Financial InclusionDocument41 pagesAEC507 Financial InclusionSarvesh JP NambiarNo ratings yet

- Financial InclusionIssues-2006Document5 pagesFinancial InclusionIssues-2006Ayush SrivastavaNo ratings yet

- FinancialInclusion RecentInitiativesandAssessmentDocument39 pagesFinancialInclusion RecentInitiativesandAssessmentShaneel AnijwalNo ratings yet

- SH As TriDocument5 pagesSH As TriRaqueem KhanNo ratings yet

- (2013 - IJMSSR) Dangi&Kumar - Current Situation of Financial Incl. in India PDFDocument12 pages(2013 - IJMSSR) Dangi&Kumar - Current Situation of Financial Incl. in India PDFMarkus WidodoNo ratings yet

- Research Paper On Financial InclusionDocument57 pagesResearch Paper On Financial InclusionChilaka Pappala0% (1)

- Financial Inclusion African Finance Journal 14102010Document22 pagesFinancial Inclusion African Finance Journal 14102010Mallikarjun DNo ratings yet

- Financial Inclusion in Burundi - The Determinants of Loan Taking Motivation in Semi Rural AreasDocument15 pagesFinancial Inclusion in Burundi - The Determinants of Loan Taking Motivation in Semi Rural AreasRjendra LamsalNo ratings yet

- Half The World Is Unbanked: Financial Access InitiativeDocument18 pagesHalf The World Is Unbanked: Financial Access Initiativeapi-26850228No ratings yet

- International Journal of Islamic Economics and Finance StudiesDocument22 pagesInternational Journal of Islamic Economics and Finance StudiesVictoria MaciasNo ratings yet

- Revised ProposalDocument12 pagesRevised ProposalSumanNo ratings yet

- Project 2Document5 pagesProject 2Shivaram NayakNo ratings yet

- India's Efforts in Financial Inclusion: CKG Nair, Ministry of Finance, IndiaDocument1 pageIndia's Efforts in Financial Inclusion: CKG Nair, Ministry of Finance, IndiamallmanmohanNo ratings yet

- Financial Inclusion - RBI - S InitiativesDocument12 pagesFinancial Inclusion - RBI - S Initiativessahil_saini298No ratings yet

- Financial Inclusion The Indian ExperienceDocument8 pagesFinancial Inclusion The Indian ExperienceSaad NiaziNo ratings yet

- Need For MF Gap DD and SSDocument2 pagesNeed For MF Gap DD and SSalviarpitaNo ratings yet

- Vinishchandra 2315124 PPTDocument11 pagesVinishchandra 2315124 PPTVinish ChandraNo ratings yet

- BlueprintDocument32 pagesBlueprintnisar0007No ratings yet

- Emerging Trends in Banking Sector - A Comparative Study From Financial Inclusion PerspectiveDocument13 pagesEmerging Trends in Banking Sector - A Comparative Study From Financial Inclusion PerspectiveIAEME PublicationNo ratings yet

- Role of Microfinance Institutions in Rural Development B.V.S.S. Subba Rao AbstractDocument13 pagesRole of Microfinance Institutions in Rural Development B.V.S.S. Subba Rao AbstractIndu GuptaNo ratings yet

- Research Paper On CONTRIBUTION OF MICROFINANCE TOWARD INCLUSIVE GROWTHDocument23 pagesResearch Paper On CONTRIBUTION OF MICROFINANCE TOWARD INCLUSIVE GROWTHRAM MAURYANo ratings yet

- Financial Inclusion: Opportunities, Issues and Challenges: George Varghese, Lakshmi ViswanathanDocument8 pagesFinancial Inclusion: Opportunities, Issues and Challenges: George Varghese, Lakshmi ViswanathanNitesh KumarNo ratings yet

- Financial InclusionDocument26 pagesFinancial InclusionErick McdonaldNo ratings yet

- College Magazine Latest KrishnanDocument6 pagesCollege Magazine Latest KrishnanChalil KrishnanNo ratings yet

- Supporting Inclusive GrowthFrom EverandSupporting Inclusive GrowthNo ratings yet

- 3 QTD MCO and Cumulative Outflow AnalysisDocument1 page3 QTD MCO and Cumulative Outflow AnalysisAlberto EstanesNo ratings yet

- Capital Investment and Financial DecisionsDocument306 pagesCapital Investment and Financial DecisionsUjjalSahuNo ratings yet

- Commercial Dispatch Eedition 7-31-19Document16 pagesCommercial Dispatch Eedition 7-31-19The DispatchNo ratings yet

- Bismarck Vs BeveridgeDocument31 pagesBismarck Vs BeveridgeHugo Couto100% (1)

- By SUMEET DOLHE - THE IMPACT OF GLOBAL RECESSION ON INFORMATION TECHNOLOGY SECTOR IN INDIADocument48 pagesBy SUMEET DOLHE - THE IMPACT OF GLOBAL RECESSION ON INFORMATION TECHNOLOGY SECTOR IN INDIASumeet DolheNo ratings yet

- Working Capital Management in HCL Infosystems Limited DeepakDocument74 pagesWorking Capital Management in HCL Infosystems Limited DeepakDeepak BhatiaNo ratings yet

- Tally Test: Kishan Lal SharmaDocument4 pagesTally Test: Kishan Lal SharmaSanjiv GautamNo ratings yet

- 2012-13 Proposed Budget DocumentDocument397 pages2012-13 Proposed Budget DocumentStatesman JournalNo ratings yet

- Unconventional Policies and Their Effects On Financial Markets PDFDocument36 pagesUnconventional Policies and Their Effects On Financial Markets PDFSoberLookNo ratings yet

- Admit Ibmba 6203210 23523 2017-01-24 924Document4 pagesAdmit Ibmba 6203210 23523 2017-01-24 924api-383567653100% (1)

- Updated Key Fact SatementDocument4 pagesUpdated Key Fact SatementYashodhan RajwadeNo ratings yet

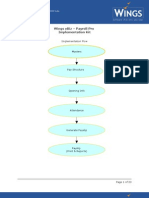

- Wings Ebiz - Payroll ProDocument23 pagesWings Ebiz - Payroll ProRoshan naiduNo ratings yet

- Study of Mutual Fund of Axis BankDocument85 pagesStudy of Mutual Fund of Axis BankNirbhay Kumar50% (6)

- REALOGY CORP 10-K (Annual Reports) 2009-02-25Document394 pagesREALOGY CORP 10-K (Annual Reports) 2009-02-25http://secwatch.comNo ratings yet

- Grow Africa - Annual Report 2014Document180 pagesGrow Africa - Annual Report 2014growafricaforum0% (1)

- Case StudyDocument10 pagesCase StudykarthinathanNo ratings yet

- Exide Life New Fulfilling LifeDocument11 pagesExide Life New Fulfilling LifeJagadish JDNo ratings yet

- Contoh Soal AKMDocument3 pagesContoh Soal AKMNada AlfiyahNo ratings yet

- Certificate Course in International Payment SystemsDocument4 pagesCertificate Course in International Payment SystemsMakarand LonkarNo ratings yet

- UCM - 54 Income Tax Law and Practice I PDFDocument90 pagesUCM - 54 Income Tax Law and Practice I PDFBrindha Babu100% (1)

- Loan Amortization ScheduleDocument37 pagesLoan Amortization ScheduleZeeshan HaiderNo ratings yet