You might also like

- Sustainability - Do Small Steps Really Go A Long WayDocument27 pagesSustainability - Do Small Steps Really Go A Long WayAyush AgrawalNo ratings yet

- CFC, FSC and Tax HavensDocument14 pagesCFC, FSC and Tax Havensdigvijay bansalNo ratings yet

- Future of Developed CountriesDocument5 pagesFuture of Developed CountriesManoj TholupunuriNo ratings yet

- (Malaysia) COUNTRY REPORT Present PDFDocument35 pages(Malaysia) COUNTRY REPORT Present PDFAzaim AnaqiNo ratings yet

- Free Trade AgreementDocument34 pagesFree Trade AgreementadarshNo ratings yet

- Assignment 102Document15 pagesAssignment 102princessdaniaNo ratings yet

- How Globalization Can Become More Pro-PoorDocument18 pagesHow Globalization Can Become More Pro-PoorfrmchnnNo ratings yet

- Webinar Seksyen 44Document4 pagesWebinar Seksyen 44Zou 11100% (1)

- OSH Reporting by Newspapers in MalaysiaDocument45 pagesOSH Reporting by Newspapers in Malaysiaahmadnaimzaid100% (3)

- Leaders Talk About Executing Strategy: By: Dr. Theresa M. WelbourneDocument8 pagesLeaders Talk About Executing Strategy: By: Dr. Theresa M. WelbourneazrulfadjriNo ratings yet

- TAX INCENTIVES FOR HOTEL & TOURISM INDUSTRIESDocument20 pagesTAX INCENTIVES FOR HOTEL & TOURISM INDUSTRIESmeera yusufNo ratings yet

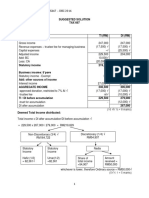

- Universiti Teknologi Mara Common Test 1 Suggested Solution: Confidential AC/APR2019/FAR320Document5 pagesUniversiti Teknologi Mara Common Test 1 Suggested Solution: Confidential AC/APR2019/FAR320iqbalhakim123100% (1)

- TAX 467 Topic 4 Capital Allowance - AgricultureDocument11 pagesTAX 467 Topic 4 Capital Allowance - AgricultureAnis RoslanNo ratings yet

- Celebrity Endorsement & Brand BuildingDocument17 pagesCelebrity Endorsement & Brand BuildingJasmine JunglaNo ratings yet

- Interest Rate FutureDocument19 pagesInterest Rate FutureDivyesh GandhiNo ratings yet

- Answer Scheme Module Waves 2019Document8 pagesAnswer Scheme Module Waves 2019Cart KartikaNo ratings yet

- Question 4 JULY2020 MAF251Document5 pagesQuestion 4 JULY2020 MAF251Tengku Ed Tengku ANo ratings yet

- A Tutorial On How To Run A Simple Linear Regression in ExcelDocument19 pagesA Tutorial On How To Run A Simple Linear Regression in ExcelNaturalEvanNo ratings yet

- Tutorial 11 PDFDocument9 pagesTutorial 11 PDFtan keng qi100% (4)

- AP Macroeconomics: Interest Rates & Investment DemandDocument10 pagesAP Macroeconomics: Interest Rates & Investment DemandAmanda BrownNo ratings yet

- Elc501 Test QP April 2018Document11 pagesElc501 Test QP April 2018Azmeer Tajei100% (1)

- Closing Case Chapter 2Document8 pagesClosing Case Chapter 2Anita Dwi Wahyuni0% (1)

- Faculty of Business and Management Transport Diploma in Business Studies Transport Ba117Document15 pagesFaculty of Business and Management Transport Diploma in Business Studies Transport Ba117Mizan SezwanNo ratings yet

- Solution Maf653 - Dec 2019 - StudentDocument7 pagesSolution Maf653 - Dec 2019 - Studentdini ffNo ratings yet

- Solution Dec 2014Document8 pagesSolution Dec 2014anis izzatiNo ratings yet

- Solution Tax667 - Dec 2018Document8 pagesSolution Tax667 - Dec 2018Zahiratul Qamarina100% (1)

- Universiti Teknologi Mara Common Test 1 Answer Scheme: Confidential AC/OCT2018/FAR320Document5 pagesUniversiti Teknologi Mara Common Test 1 Answer Scheme: Confidential AC/OCT2018/FAR320iqbalhakim123No ratings yet

- Solution Far560 - Jun 2015 (S)Document7 pagesSolution Far560 - Jun 2015 (S)MUHAMAD MUKHAIRI MUHAMAD HANIFAHNo ratings yet

- Far210 Topic 2 Malaysian Conceptual FrameworkDocument79 pagesFar210 Topic 2 Malaysian Conceptual FrameworkSamurai Hut100% (1)

- Modern Power SystemsDocument8 pagesModern Power Systemserkumar_ranjanNo ratings yet

- Solution Far410 Jun 2019Document9 pagesSolution Far410 Jun 2019Nabilah NorddinNo ratings yet

- BKAR 1013 FINANCIAL ACCOUNTING AND REPORTING IDocument4 pagesBKAR 1013 FINANCIAL ACCOUNTING AND REPORTING Idini sofiaNo ratings yet

- D9.1 Project Management PlanDocument18 pagesD9.1 Project Management PlangkoutNo ratings yet

- Topic 1 - MGT 153Document28 pagesTopic 1 - MGT 153Amri Gaban100% (4)

- MAF503 June 2015 Suggested SolutionDocument8 pagesMAF503 June 2015 Suggested Solutionanis izzatiNo ratings yet

- Solution Tax667 - Dec 2016Document7 pagesSolution Tax667 - Dec 2016Zahiratul QamarinaNo ratings yet

- Taxation (Malaysia) Answers and Marking SchemeDocument8 pagesTaxation (Malaysia) Answers and Marking SchemeHar San LeeNo ratings yet

- Assignment 2:: Islamic Finance (PFS 2253) Semester: August 2021Document9 pagesAssignment 2:: Islamic Finance (PFS 2253) Semester: August 2021anis farehaNo ratings yet

- Corporate AjinamotoDocument23 pagesCorporate Ajinamotoprincess_anabella_1No ratings yet

- Chapter 2 Corporate TaxDocument50 pagesChapter 2 Corporate TaxNgNo ratings yet

- CT SS For Student Oct2018Document5 pagesCT SS For Student Oct2018Nabila RosmizaNo ratings yet

- Solution Tax667 - Jun 2016-1Document8 pagesSolution Tax667 - Jun 2016-1Zahiratul QamarinaNo ratings yet

- Multinational Companies PPTTTDocument26 pagesMultinational Companies PPTTTAnmolNo ratings yet

- Meaning of Multinational CompaniesDocument3 pagesMeaning of Multinational CompaniesPrem Abish PokhrelNo ratings yet

- Penang Realty Case Against IRBDocument15 pagesPenang Realty Case Against IRBsimson singawahNo ratings yet

- Taxation I Tutorial: Tax ReliefDocument2 pagesTaxation I Tutorial: Tax Reliefathirah jamaludinNo ratings yet

- Unifast ActDocument17 pagesUnifast ActQuel Limbo100% (2)

- Operational Management Chapter 1Document30 pagesOperational Management Chapter 1Aqsa AliNo ratings yet

- Group Assignment (Problem Based Learning - Set F) : Pma1113 Introducting To Cost & Management AccountingDocument7 pagesGroup Assignment (Problem Based Learning - Set F) : Pma1113 Introducting To Cost & Management AccountingSyamala 29No ratings yet

- Pre-Bid Project Planning GuideDocument21 pagesPre-Bid Project Planning GuideKashi Nath SharmaNo ratings yet

- Modul P&P - FAR320 Nov 2014-Yusnaliza Vs NorlianaDocument21 pagesModul P&P - FAR320 Nov 2014-Yusnaliza Vs NorlianaAiman Abdul BaserNo ratings yet

- Past Year Far460 - Dec 2014Document7 pagesPast Year Far460 - Dec 2014Alief Zazman100% (1)

- Resolving Industrial DisputesDocument12 pagesResolving Industrial DisputesAmrezaa IskandarNo ratings yet

- Maf 451 - Suggested Solutions: (A) Statement of Equivalent UnitsDocument7 pagesMaf 451 - Suggested Solutions: (A) Statement of Equivalent Unitsanis izzatiNo ratings yet

- Week 5 Lecture Handout - LecturerDocument5 pagesWeek 5 Lecture Handout - LecturerRavinesh PrasadNo ratings yet

- TAX Treatment For TAX267 and TAX317 Budget 2019Document5 pagesTAX Treatment For TAX267 and TAX317 Budget 2019nonameNo ratings yet

- F6mys 2009 Dec QDocument10 pagesF6mys 2009 Dec QDave Loh Chong HowNo ratings yet

- F6mys 2008 Jun QDocument9 pagesF6mys 2008 Jun QNik NasuhaNo ratings yet

- Taxation (Malaysia) : Specimen Exam Applicable From December 2015Document22 pagesTaxation (Malaysia) : Specimen Exam Applicable From December 2015cytan828No ratings yet

- Foundations in Taxation (Malaysia)Document20 pagesFoundations in Taxation (Malaysia)ShazwanieSazaliNo ratings yet

- Application Letter - 2Document1 pageApplication Letter - 2Saayesha RamNo ratings yet

- Motivated Accounts Officer Seeks New ChallengeDocument1 pageMotivated Accounts Officer Seeks New ChallengeSaayesha RamNo ratings yet

- P 3Document20 pagesP 3billyryan1No ratings yet

- Application Form: Mauritius Oceanography InstituteDocument7 pagesApplication Form: Mauritius Oceanography InstituteSaayesha RamNo ratings yet

- Timesheet For EmployeesDocument2 pagesTimesheet For EmployeesSaayesha RamNo ratings yet

- IWS ClientDocument40 pagesIWS ClientSaayesha RamNo ratings yet

- Brocure CreamDocument6 pagesBrocure CreamSaayesha RamNo ratings yet

- IWS ClientDocument40 pagesIWS ClientSaayesha RamNo ratings yet

- Brochure 2014 - JelleweriesDocument11 pagesBrochure 2014 - JelleweriesSaayesha RamNo ratings yet

- 1) Stud GF Earrings) Traditional GF EarringsDocument10 pages1) Stud GF Earrings) Traditional GF EarringsSaayesha RamNo ratings yet

- Moisture Rich Shower Cream LAVENDER & ORCHID& Olive Oil & Honey & Obliphicha Oil780mlDocument20 pagesMoisture Rich Shower Cream LAVENDER & ORCHID& Olive Oil & Honey & Obliphicha Oil780mlSaayesha RamNo ratings yet

- 1) Stud GF Earrings) Traditional GF EarringsDocument10 pages1) Stud GF Earrings) Traditional GF EarringsSaayesha RamNo ratings yet

- June 2011 QDocument9 pagesJune 2011 Qlucyo123No ratings yet

- f9 2008 Dec QDocument8 pagesf9 2008 Dec QreshmadrbNo ratings yet

- F6uk Jun 2011 AnsDocument11 pagesF6uk Jun 2011 AnsSaayesha RamNo ratings yet

- Taxation (Malaysia) : Monday 7 June 2010Document10 pagesTaxation (Malaysia) : Monday 7 June 2010Saayesha RamNo ratings yet