You might also like

- An Introduction to Holistic Enterprise Architecture: Fourth EditionFrom EverandAn Introduction to Holistic Enterprise Architecture: Fourth EditionNo ratings yet

- Dwnload Full Database Systems Design Implementation and Management 13th Edition Coronel Solutions Manual PDFDocument36 pagesDwnload Full Database Systems Design Implementation and Management 13th Edition Coronel Solutions Manual PDFtabetha363100% (14)

- Database Systems Design Implementation and Management 13th Edition Coronel Solutions ManualDocument25 pagesDatabase Systems Design Implementation and Management 13th Edition Coronel Solutions ManualAnthonyWilsonodwp100% (51)

- 2021 Book DynamicsInLogisticsDocument322 pages2021 Book DynamicsInLogisticsandres segovia100% (1)

- Final Project - Ecommerce ENEBDocument10 pagesFinal Project - Ecommerce ENEBYarey Sánchez Aponte100% (1)

- Construction Companies ListDocument5 pagesConstruction Companies ListCH'NG SHU YI STUDENTNo ratings yet

- BMM: A Business Modeling Method For Information Systems DevelopmentDocument19 pagesBMM: A Business Modeling Method For Information Systems DevelopmentVladimir Jose Mata PerezNo ratings yet

- Homesake: Homerun in Home DecorDocument3 pagesHomesake: Homerun in Home DecorPARUL SINGH MBA 2019-21 (Delhi)100% (1)

- Što Su Poslovna PravilaDocument77 pagesŠto Su Poslovna PravilapitupskripteNo ratings yet

- Whitepaper Integration of Business Decision Modeling in Organization DesignDocument16 pagesWhitepaper Integration of Business Decision Modeling in Organization DesignSiddhartha BrahmaNo ratings yet

- Chapter 4. Describing What Businesses Do and How They Do It: Robert J. Glushko and Tim McgrathDocument52 pagesChapter 4. Describing What Businesses Do and How They Do It: Robert J. Glushko and Tim McgrathAnonymous GDOULL9No ratings yet

- Business Rules in EgovDocument10 pagesBusiness Rules in Egovinaksis2No ratings yet

- A Decision Making Methodology in Support of The Business Rules Lifecycle - IEEE.1997-Institute of Electrical & Electronics EngineeDocument11 pagesA Decision Making Methodology in Support of The Business Rules Lifecycle - IEEE.1997-Institute of Electrical & Electronics EngineeMilan KolarevicNo ratings yet

- %Xvlqhvv5Xohv $Ssurdfkwrwkh0Rghoolqj'Hvljqdqg, Psohphqwdwlrqri$Jhqw2Ulhqwhg, Qirupdwlrq6/VwhpvDocument17 pages%Xvlqhvv5Xohv $Ssurdfkwrwkh0Rghoolqj'Hvljqdqg, Psohphqwdwlrqri$Jhqw2Ulhqwhg, Qirupdwlrq6/VwhpvzhaozilongNo ratings yet

- Actor Perception in Business Use Case Modeling: Sergio - Decesare@Brunel - Ac.UkDocument33 pagesActor Perception in Business Use Case Modeling: Sergio - Decesare@Brunel - Ac.UkAmy LimNo ratings yet

- Full Download Database Systems Design Implementation and Management 11th Edition Coronel Solutions ManualDocument36 pagesFull Download Database Systems Design Implementation and Management 11th Edition Coronel Solutions Manualjaydejakabfx100% (28)

- Formal Modelling of Business Rules: What Kind of Tool To Use?Document15 pagesFormal Modelling of Business Rules: What Kind of Tool To Use?Giomaira MedinaNo ratings yet

- ReMoLa Responsibility Model Language To Align Access Rights With Business Process RequirementsDocument6 pagesReMoLa Responsibility Model Language To Align Access Rights With Business Process Requirementschristophe feltusNo ratings yet

- Case StudyDocument26 pagesCase Studysubhash221103100% (1)

- Administrative Context - VsDocument16 pagesAdministrative Context - VsGeet SiteshNo ratings yet

- A Generic Constraints-Based Framework For Business Modeling: (Minli, CJH) @doc - Ic.ac - UkDocument15 pagesA Generic Constraints-Based Framework For Business Modeling: (Minli, CJH) @doc - Ic.ac - UkhasandalalNo ratings yet

- Enterprise Architecting: Critical ProblemsDocument10 pagesEnterprise Architecting: Critical ProblemsNavyaNo ratings yet

- Business Rule: Jump To Navigation Jump To SearchDocument3 pagesBusiness Rule: Jump To Navigation Jump To SearchLaeh SaclagNo ratings yet

- Organzational Structure of All TimeDocument4 pagesOrganzational Structure of All TimeMaxNo ratings yet

- A Comparison of The Top Four Enterprise ArchDocument39 pagesA Comparison of The Top Four Enterprise ArchAsiya FaizyNo ratings yet

- Operating Models: The Theory and The PracticeDocument43 pagesOperating Models: The Theory and The Practiceaim researchNo ratings yet

- System Analysis & Design & Software Engineering: Assignment: MBA-IT-2Document16 pagesSystem Analysis & Design & Software Engineering: Assignment: MBA-IT-2Biswaranjan TripathyNo ratings yet

- CH 3Document7 pagesCH 3geo023No ratings yet

- Logical Database Design Using Entity-Relationship Modeling: Normalization To Avoid RedundancyDocument12 pagesLogical Database Design Using Entity-Relationship Modeling: Normalization To Avoid RedundancyCy Patrick KweeNo ratings yet

- Types of Organizational StructureDocument8 pagesTypes of Organizational StructureKanushiNo ratings yet

- Programacion Orientada A AgentesDocument8 pagesProgramacion Orientada A Agentessaito8989No ratings yet

- BusinessLogic (Lesson5 6)Document4 pagesBusinessLogic (Lesson5 6)Micca CalingaNo ratings yet

- The Include and Extend Relationships in Use Case Models: 43EBBED6-2DD6-289D74Document9 pagesThe Include and Extend Relationships in Use Case Models: 43EBBED6-2DD6-289D74Syahreza Benny PutraNo ratings yet

- Building A Formal Enterprise Architecture ModelDocument13 pagesBuilding A Formal Enterprise Architecture ModelRamesh RajagopalanNo ratings yet

- Use Cases Are More Than System OperationsDocument15 pagesUse Cases Are More Than System OperationsHumayun WarraichNo ratings yet

- 3.4 Defining Enterprise ArchitectureDocument9 pages3.4 Defining Enterprise ArchitecturewordworthNo ratings yet

- A Comparison of The Top Four Enterprise-Architecture MethodologiesDocument40 pagesA Comparison of The Top Four Enterprise-Architecture MethodologiesSDNo ratings yet

- iIT REPORTDocument5 pagesiIT REPORTMonica CudalNo ratings yet

- Chap 6Document48 pagesChap 6SGNo ratings yet

- Top Four Enterprise-Architecture Methodologies PDFDocument19 pagesTop Four Enterprise-Architecture Methodologies PDFswapnil_bankarNo ratings yet

- Top Four Enterprise-Architecture MethodologiesDocument19 pagesTop Four Enterprise-Architecture Methodologiesswapnil_bankarNo ratings yet

- Kurtyka A Systems Theory of Bi-1Document5 pagesKurtyka A Systems Theory of Bi-1Camara Alseny BassenguéNo ratings yet

- How To Document SystemDocument9 pagesHow To Document SystemHemalatha KarthikeyanNo ratings yet

- What Is Business Analysis?Document5 pagesWhat Is Business Analysis?madhujayarajNo ratings yet

- Determining Suitability of Database Functionality and Scalability UC - 7Document10 pagesDetermining Suitability of Database Functionality and Scalability UC - 7Aliyan AmanNo ratings yet

- Seminar On System Analysis and DesignDocument42 pagesSeminar On System Analysis and DesignOzioma Teddy UkwuomaNo ratings yet

- Enterprise Architecture and Knowledge Perspectives On Continuous Requirements EngineeringDocument8 pagesEnterprise Architecture and Knowledge Perspectives On Continuous Requirements Engineeringswapnil_bankarNo ratings yet

- Managing ERP Systems and Enterprise Strategy: A Dynamic Enterprise Reference GridDocument23 pagesManaging ERP Systems and Enterprise Strategy: A Dynamic Enterprise Reference GridShah Maqsumul Masrur TanviNo ratings yet

- Homework 2 - DatabaseDocument20 pagesHomework 2 - DatabaseMerlie ChingNo ratings yet

- Business Modeling With UML: The Light at The End of The TunnelDocument9 pagesBusiness Modeling With UML: The Light at The End of The TunnelMario SolarteNo ratings yet

- Dwnload Full Database Systems Design Implementation and Management 11th Edition Coronel Solutions Manual PDFDocument25 pagesDwnload Full Database Systems Design Implementation and Management 11th Edition Coronel Solutions Manual PDFtabetha363100% (19)

- An Integrated EA FrameworkDocument9 pagesAn Integrated EA Frameworkpedro_luna_43No ratings yet

- Thoughts On Functional DecompositionDocument5 pagesThoughts On Functional DecompositionXemox XenimaxNo ratings yet

- Zachman FrameworkDocument7 pagesZachman FrameworkHeriyanto LimNo ratings yet

- Use Case DiagramsDocument4 pagesUse Case Diagramssydh614No ratings yet

- Book Item 11315Document28 pagesBook Item 11315mitu lead01No ratings yet

- Chapter 1Document31 pagesChapter 1Brenda MuseNo ratings yet

- A Comparison of The Top Four Enterprise-Architecture MethodologiesDocument36 pagesA Comparison of The Top Four Enterprise-Architecture MethodologiesvikkasjindalNo ratings yet

- ASIA Module 2Document26 pagesASIA Module 2marsh mallowNo ratings yet

- 05 BPTrends 2007 Rummler & Ramias ITDisasters-A Root CauseDocument7 pages05 BPTrends 2007 Rummler & Ramias ITDisasters-A Root CauseKidwvyneBeatsNo ratings yet

- 10 Key Skills Architects Must Have To Deliver ValueDocument29 pages10 Key Skills Architects Must Have To Deliver ValuePeter HofmannNo ratings yet

- Agility: The Key To Survival of The Fittest in The Software MarketDocument16 pagesAgility: The Key To Survival of The Fittest in The Software MarketEmerand RandiNo ratings yet

- Unit-Ii Principles of Service-OrientationDocument10 pagesUnit-Ii Principles of Service-OrientationprasanthikasamsettyNo ratings yet

- Manajemen Pemeliharaan Fasilitas Bangunan Gedung Pada Proyek Swasta: Studi KasusDocument7 pagesManajemen Pemeliharaan Fasilitas Bangunan Gedung Pada Proyek Swasta: Studi KasusNoor HasnawatiNo ratings yet

- Goals of Financial Management-Valuation ApproachDocument9 pagesGoals of Financial Management-Valuation Approachnatalie clyde matesNo ratings yet

- Wiley Economic History SocietyDocument27 pagesWiley Economic History SocietyJames HeartfieldNo ratings yet

- Test Bank For Retail Management A Strategic Approach 13th by BermanDocument21 pagesTest Bank For Retail Management A Strategic Approach 13th by Bermandelphianimpugnerolk3gNo ratings yet

- SB Bonifacio G. GalayDocument3 pagesSB Bonifacio G. GalayJeorel QuiapoNo ratings yet

- Ordinance No.01 S 2023 BPLODocument3 pagesOrdinance No.01 S 2023 BPLOBarangay LibasNo ratings yet

- Develop An Extended Model For The Data Management System For Inter-Hospitals On Client Medical ServicesDocument7 pagesDevelop An Extended Model For The Data Management System For Inter-Hospitals On Client Medical ServicesInternational Journal of Innovative Science and Research TechnologyNo ratings yet

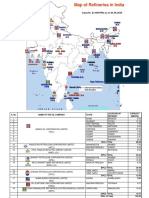

- RefineriesMap PDFDocument2 pagesRefineriesMap PDFMayur MandrekarNo ratings yet

- Bangko Sentral NG Pilipinas Citizen's CharterDocument5 pagesBangko Sentral NG Pilipinas Citizen's CharterAlex ReyesNo ratings yet

- Hot Sheet: Yamalube ProductsDocument2 pagesHot Sheet: Yamalube Productsrolex21No ratings yet

- D.O MAA WARISAN ENT Rasyein Final 02tanker Sadao TripDocument2 pagesD.O MAA WARISAN ENT Rasyein Final 02tanker Sadao TripJuliana HarunNo ratings yet

- MBAAR AssignmentDocument43 pagesMBAAR Assignmentkidszalor1412100% (3)

- Revised FAQ CGGPRA Rules 2017 - Updated On 16 December 2020Document49 pagesRevised FAQ CGGPRA Rules 2017 - Updated On 16 December 2020Rakesh Ambasana HNo ratings yet

- Case StudyDocument3 pagesCase Studynazia malikNo ratings yet

- Welding & SR Requirements - Pressure Parts - BoilerDocument7 pagesWelding & SR Requirements - Pressure Parts - BoilerNavneet SinghNo ratings yet

- Full Download Culture Counts A Concise Introduction To Cultural Anthropology 2nd Edition Nanda Test BankDocument11 pagesFull Download Culture Counts A Concise Introduction To Cultural Anthropology 2nd Edition Nanda Test Bankmasonpierce2z8s100% (39)

- Bus 5112 Marketing Management Written Assignment Unit 2Document5 pagesBus 5112 Marketing Management Written Assignment Unit 2rueNo ratings yet

- Advanced Financial Reporting: RevisionDocument44 pagesAdvanced Financial Reporting: Revisionmy VinayNo ratings yet

- Packaging and Labeling DecisionsDocument10 pagesPackaging and Labeling DecisionsKomal Shujaat100% (5)

- Human Resources Workforce Plan Milestone TwoDocument7 pagesHuman Resources Workforce Plan Milestone TwoKennedy WashikaNo ratings yet

- Case Study: What Went Wrong at Foxmeyer?: Página de 1 de 4Document4 pagesCase Study: What Went Wrong at Foxmeyer?: Página de 1 de 4ADRIAN WALDIR MIRANDA CORILLOCLLANo ratings yet

- SG Airlines ESG Report 2021 - 22Document253 pagesSG Airlines ESG Report 2021 - 22sherwynNo ratings yet

- Towards Enhancing Building Information Modeling Implementation in The Egyptian AEC IndustryDocument15 pagesTowards Enhancing Building Information Modeling Implementation in The Egyptian AEC IndustryIEREKPRESSNo ratings yet

- 5G Evolution Across Three Major ReleasesDocument1 page5G Evolution Across Three Major ReleasesCamilo CelisNo ratings yet

- Unit 9Document13 pagesUnit 9yafot56346No ratings yet

- Sbi Po Prelims 2020: English LanguageDocument15 pagesSbi Po Prelims 2020: English LanguageShivNo ratings yet