You might also like

- Quiz 1 InstructionsDocument6 pagesQuiz 1 Instructionssyed mujtubaNo ratings yet

- Wiring OptionsDocument81 pagesWiring Optionsmahaan khatri100% (6)

- Final Exam Sample Questions Attempt Review 5Document9 pagesFinal Exam Sample Questions Attempt Review 5leieparanoico100% (1)

- Bond Valuation: Case: Atlas InvestmentsDocument853 pagesBond Valuation: Case: Atlas Investmentsjk kumarNo ratings yet

- Valuation of Fixed Income SecuritiesDocument41 pagesValuation of Fixed Income SecuritiesVikrant Verma100% (1)

- Dividends Still Don't Lie: The Truth About Investing in Blue Chip Stocks and Winning in the Stock MarketFrom EverandDividends Still Don't Lie: The Truth About Investing in Blue Chip Stocks and Winning in the Stock MarketNo ratings yet

- Port Marine CircularsDocument649 pagesPort Marine CircularsNurlia AduNo ratings yet

- F.249 Fund Transfer Request Form1Document3 pagesF.249 Fund Transfer Request Form1OscarNo ratings yet

- Chapter 12. The Term Structure of Interest Rates Chapter 12. The Term Structure of Interest RatesDocument37 pagesChapter 12. The Term Structure of Interest Rates Chapter 12. The Term Structure of Interest RatesVikas JhabakNo ratings yet

- Chapter 12. The Term Structure of Interest RatesDocument37 pagesChapter 12. The Term Structure of Interest RatesUbaid DarNo ratings yet

- Chapter 7. Risk and Term Structure of Interest Rates Chapter 7. Risk and Term Structure of Interest RatesDocument72 pagesChapter 7. Risk and Term Structure of Interest Rates Chapter 7. Risk and Term Structure of Interest RatesGulEFarisFarisNo ratings yet

- The Structure of Interest RatesDocument72 pagesThe Structure of Interest RatesMarwa HassanNo ratings yet

- Term Structure of Interest RatesDocument21 pagesTerm Structure of Interest RatestoabhishekpalNo ratings yet

- 2 - Fixed Income SecuritiesDocument19 pages2 - Fixed Income Securitiesquynhnhudang5No ratings yet

- Intermediate Finance: Session 9Document56 pagesIntermediate Finance: Session 9rizaunNo ratings yet

- Unit 3 - Term Structure of Interest Rates Slides 2022Document53 pagesUnit 3 - Term Structure of Interest Rates Slides 2022ndonithando2207No ratings yet

- ECN 3422 - Lecture 1 - 2021.09.21Document21 pagesECN 3422 - Lecture 1 - 2021.09.21Cornelius MasikiniNo ratings yet

- Now U S A Bank Is Buying $ and Give RsDocument84 pagesNow U S A Bank Is Buying $ and Give RsNitin RajotiaNo ratings yet

- Term Structure of Interest Rates, Spot Rate & Forward RateDocument18 pagesTerm Structure of Interest Rates, Spot Rate & Forward RateShruti Savant DodaniNo ratings yet

- Term Structure of Interest RatesDocument17 pagesTerm Structure of Interest RatesTheagarajan ThanikachalamNo ratings yet

- Lecture 4Document27 pagesLecture 4superzttNo ratings yet

- Lecture 4 - Bond Portfolio ManagementDocument42 pagesLecture 4 - Bond Portfolio ManagementAnh ThoNo ratings yet

- Valuation of Fixed Income SecuritiesDocument37 pagesValuation of Fixed Income Securitiesaksh02007No ratings yet

- Term Structure of Interest RatesDocument44 pagesTerm Structure of Interest RatesmasatiNo ratings yet

- Foreign Exchange: - Purchase and Sale of National Currencies - Huge MarketDocument100 pagesForeign Exchange: - Purchase and Sale of National Currencies - Huge MarketAmber PetersonNo ratings yet

- 4 - Term Structures TheoriesDocument15 pages4 - Term Structures Theoriesmajmmallikarachchi.mallikarachchiNo ratings yet

- The Yield CurveDocument14 pagesThe Yield CurveAmirNo ratings yet

- GE1202 Managing Your Personal Finance: SavingDocument29 pagesGE1202 Managing Your Personal Finance: SavingAiden LANNo ratings yet

- Lecture 5312312Document55 pagesLecture 5312312Tam Chun LamNo ratings yet

- Finance Notes Chapter 13Document7 pagesFinance Notes Chapter 13D HoNo ratings yet

- Yield Curve Analysis: Rahul Chhabra MBA, 3 SemDocument21 pagesYield Curve Analysis: Rahul Chhabra MBA, 3 SemRushmiS100% (2)

- Reading 2Document9 pagesReading 2Syed Mujtaba Ali AhsanNo ratings yet

- AFM 204 - Class 7 Slides - Cost of EquityDocument49 pagesAFM 204 - Class 7 Slides - Cost of Equityasflkhaf2No ratings yet

- Foreign Exchange: - Purchase and Sale of National Currencies - Huge MarketDocument102 pagesForeign Exchange: - Purchase and Sale of National Currencies - Huge MarketChirag BachaniNo ratings yet

- Term Structure and Risk StructureDocument28 pagesTerm Structure and Risk StructureAdina CasianaNo ratings yet

- Lec 10Document26 pagesLec 10danphamm226No ratings yet

- Riskterm PrintDocument6 pagesRiskterm Printsmit9993No ratings yet

- DuSmtnvfEemMzQ7SOgDNxg - Module 3 Lecture SlidesDocument70 pagesDuSmtnvfEemMzQ7SOgDNxg - Module 3 Lecture SlidesCocos CosmeticsNo ratings yet

- Investment Basics I: ObjectivesDocument14 pagesInvestment Basics I: Objectivesno nameNo ratings yet

- UntitledDocument29 pagesUntitledDEEPIKA S R BUSINESS AND MANAGEMENT (BGR)No ratings yet

- Bonds Overview Pricing YieldDocument40 pagesBonds Overview Pricing YieldRajesh Chowdary Chintamaneni100% (1)

- Duration & ConvexityDocument18 pagesDuration & ConvexityHrishikesh Malu100% (3)

- BondsDocument53 pagesBondsKshitishNo ratings yet

- Expectations TheoryDocument10 pagesExpectations TheorywanNo ratings yet

- FM 8Document33 pagesFM 8Taaran ReddyNo ratings yet

- Revision Test 1Document15 pagesRevision Test 1ndonithando2207No ratings yet

- ECO 302 Intermediate Macroeconomic Theory I: The IS Curve (Jones Chapter 11)Document45 pagesECO 302 Intermediate Macroeconomic Theory I: The IS Curve (Jones Chapter 11)Md SafiNo ratings yet

- Bonds and Bond MarketsDocument124 pagesBonds and Bond Marketskarthik chamarthyNo ratings yet

- Economy SR 2Document41 pagesEconomy SR 2PriyanshNo ratings yet

- Unit2 IapmDocument43 pagesUnit2 IapmAshish SinghNo ratings yet

- Yield Curve Analysis and Fixed-Income ArbitrageDocument33 pagesYield Curve Analysis and Fixed-Income Arbitrageandrewfu1988No ratings yet

- The Level & Structure of Interest RatesDocument49 pagesThe Level & Structure of Interest RatesarmailgmNo ratings yet

- Chapter 6. Bonds, Bond Prices and Interest Rates Chapter 6. Bonds, Bond Prices and Interest RatesDocument57 pagesChapter 6. Bonds, Bond Prices and Interest Rates Chapter 6. Bonds, Bond Prices and Interest RatesGulEFarisFarisNo ratings yet

- PP Lecture On Introduction To The Term Structure of Interest RatesDocument12 pagesPP Lecture On Introduction To The Term Structure of Interest Ratesbhawika bajajNo ratings yet

- Bond Price VolatilityDocument63 pagesBond Price VolatilityJithesh JanardhananNo ratings yet

- Chapter 3 What Do Interest Rates Mean and What Is Their Role in ValuationDocument13 pagesChapter 3 What Do Interest Rates Mean and What Is Their Role in ValuationJay Ann DomeNo ratings yet

- Money: - What Is Money? - 3 Distinguishing Features of MoneyDocument46 pagesMoney: - What Is Money? - 3 Distinguishing Features of MoneyabissembayNo ratings yet

- Statistical ArbitrageDocument21 pagesStatistical ArbitragehannesreiNo ratings yet

- Option VolatilityDocument50 pagesOption VolatilityJunedi dNo ratings yet

- Efficient Market TheoryDocument25 pagesEfficient Market TheorypriyaNo ratings yet

- Gold Value and Gold Prices from 1971 - 2021: An Empirical ModelFrom EverandGold Value and Gold Prices from 1971 - 2021: An Empirical ModelNo ratings yet

- Common Sense Retirement Planning: Home, Savings and InvestmentFrom EverandCommon Sense Retirement Planning: Home, Savings and InvestmentNo ratings yet

- Article 1: Snva-Edutech PVT LTD B 44, Sector 59, Noida, Uttar Pradesh 201301, India CIN No: U80100DL2009PTC195637Document1 pageArticle 1: Snva-Edutech PVT LTD B 44, Sector 59, Noida, Uttar Pradesh 201301, India CIN No: U80100DL2009PTC195637Mridal PandeyNo ratings yet

- MGT Assignment Jack Welch's LeadershipDocument3 pagesMGT Assignment Jack Welch's LeadershipAmanie Othman100% (1)

- 购买 SATOR LNG 中介支付承诺书: Letter Of Commitment To Purchase Satorlng Intermediary PaymentDocument3 pages购买 SATOR LNG 中介支付承诺书: Letter Of Commitment To Purchase Satorlng Intermediary PaymentJIN YuanNo ratings yet

- XX SectionDocument1 pageXX SectionNagesh ChitariNo ratings yet

- DownloadDocument6 pagesDownloadFaris KhazaharNo ratings yet

- Gammon: Heavy Duty Dry Break Quick DisconnectDocument2 pagesGammon: Heavy Duty Dry Break Quick DisconnectAdolfo Eduardo García BraunNo ratings yet

- Lifting Plan Symphony StarDocument27 pagesLifting Plan Symphony StarJosé Luis Saá LoorNo ratings yet

- Six Merger Waves in The Historical MergersDocument6 pagesSix Merger Waves in The Historical MergersMei YunNo ratings yet

- Champions 50Document7 pagesChampions 50VijayaLakshmi KuchimanchiNo ratings yet

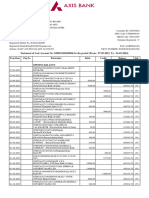

- Account STMTDocument27 pagesAccount STMTsrinivas rao kNo ratings yet

- The Question of Imperialism The Political Economy of Dominance and Dependence by Benjamin J. CohenDocument277 pagesThe Question of Imperialism The Political Economy of Dominance and Dependence by Benjamin J. CohenFernandaNo ratings yet

- Eco QuizDocument9 pagesEco QuizAhsan IjazNo ratings yet

- Barnacle Parps Chainsaw Guide PDFDocument279 pagesBarnacle Parps Chainsaw Guide PDFGabriel LinsNo ratings yet

- JK 8009VC PDFDocument48 pagesJK 8009VC PDFSewing worldNo ratings yet

- Mutasi Mar 2023Document1 pageMutasi Mar 2023Imam Fidyansyah100% (1)

- HSSK Associate: Johnson & Johnson ParkDocument6 pagesHSSK Associate: Johnson & Johnson Parkshri277No ratings yet

- ASI Mech - Certificado de IncorporaciónDocument2 pagesASI Mech - Certificado de IncorporaciónAirekoNo ratings yet

- Draft DMS User Manual - 50 Years Indonesia Korea Update 1Document17 pagesDraft DMS User Manual - 50 Years Indonesia Korea Update 1adityasamhyundaiNo ratings yet

- Operations Management 8 TH EditionDocument17 pagesOperations Management 8 TH EditionElmer John BallonNo ratings yet

- Engineering Economics (Theory of Cost)Document12 pagesEngineering Economics (Theory of Cost)Usman QasimNo ratings yet

- Ibm - Chapter 3Document21 pagesIbm - Chapter 3yared haftuNo ratings yet

- A Sovereign Wealth FundDocument1 pageA Sovereign Wealth FundArthur LeywinNo ratings yet

- Company Stats EuropeDocument375 pagesCompany Stats Europesourabh6chakrabort-1No ratings yet

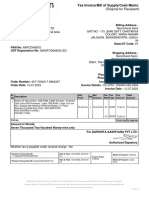

- InvoiceDocument1 pageInvoiceNemichand SainiNo ratings yet

- Lucky Carrot : Show Transcribed Image TextDocument2 pagesLucky Carrot : Show Transcribed Image TextAchmad RizalNo ratings yet

- Bba Alternative Assignment-1Document2 pagesBba Alternative Assignment-1princrNo ratings yet