You might also like

- Business Cycles and Aggregate DemandDocument40 pagesBusiness Cycles and Aggregate DemandSnehal Joshi100% (1)

- Globalization and Its DiscontentsDocument6 pagesGlobalization and Its DiscontentsNazish SohailNo ratings yet

- Macro5 Lecppt ch11Document88 pagesMacro5 Lecppt ch11이가빈[학생](국제대학 국제학과)No ratings yet

- Week 9 - SII2013 PDFDocument67 pagesWeek 9 - SII2013 PDFGorge SorosNo ratings yet

- EinfMakro 2023 - Vorlesung 4Document27 pagesEinfMakro 2023 - Vorlesung 4Miloje RamadaniNo ratings yet

- Introductory Macroeconomics ECON10003: Lecture 6: The Keynesian Model of The Economy IDocument24 pagesIntroductory Macroeconomics ECON10003: Lecture 6: The Keynesian Model of The Economy IImaweeb 77No ratings yet

- Aggregate Demand - MacroDocument21 pagesAggregate Demand - MacroHaardik GandhiNo ratings yet

- Consumption FunctionDocument39 pagesConsumption FunctionAnku SharmaNo ratings yet

- Session 10 11Document16 pagesSession 10 11Alfa RydesterNo ratings yet

- Chapter 6 (Macro)Document10 pagesChapter 6 (Macro)mashibani01No ratings yet

- Week9 Thursday SlidesDocument36 pagesWeek9 Thursday SlidesSiham BuuleNo ratings yet

- Macro5 Lecppt ch05Document102 pagesMacro5 Lecppt ch05meuang68No ratings yet

- Session 6Document13 pagesSession 623pgp011No ratings yet

- Macroeconomics - Keynesian ModelsDocument22 pagesMacroeconomics - Keynesian ModelsAlfa RydesterNo ratings yet

- Aggregate Demand and Aggregate SupplyDocument24 pagesAggregate Demand and Aggregate SupplyAri HaranNo ratings yet

- Macroeconomics III: Consumption and Investment: Gavin Cameron Lady Margaret HallDocument21 pagesMacroeconomics III: Consumption and Investment: Gavin Cameron Lady Margaret HallIrina StefanaNo ratings yet

- Week3 Thursday SlidesDocument36 pagesWeek3 Thursday SlidesSiham BuuleNo ratings yet

- Macro - Module - 16 3Document23 pagesMacro - Module - 16 3AlexNo ratings yet

- Aggregate Supply and Aggregate Demand: R. Santos, "Economics: Principles & Application." Prepared by Rick HelserDocument18 pagesAggregate Supply and Aggregate Demand: R. Santos, "Economics: Principles & Application." Prepared by Rick HelserIndivineNo ratings yet

- Consumption Savings Investment. ParadoxDocument46 pagesConsumption Savings Investment. ParadoxChristine Joy LanabanNo ratings yet

- Investment TheoryDocument23 pagesInvestment TheoryAnkita MalikNo ratings yet

- 11 - Growth Capital and IdeasDocument41 pages11 - Growth Capital and IdeasSHEUM PEE KHEE / UPMNo ratings yet

- CH 10 Lo - Economic - InstabilityDocument26 pagesCH 10 Lo - Economic - Instabilitytariku1234No ratings yet

- Shifts of The Curve: Price Level Money Supply ExogenousDocument28 pagesShifts of The Curve: Price Level Money Supply ExogenousKoyakuNo ratings yet

- Aggregate Demand & Keynesian Multiplier PDFDocument6 pagesAggregate Demand & Keynesian Multiplier PDFArunabh ChoudhuryNo ratings yet

- Lecture 3 (Chapter 19)Document28 pagesLecture 3 (Chapter 19)raymondNo ratings yet

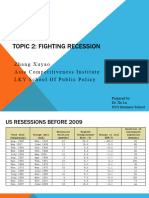

- Week 2 Fighting RecessionDocument42 pagesWeek 2 Fighting Recessiondaisyruyu2001No ratings yet

- My Aggregate Demand & Aggregate Supply (Edited For Class)Document113 pagesMy Aggregate Demand & Aggregate Supply (Edited For Class)ShivamNo ratings yet

- Session 5Document21 pagesSession 523pgp011No ratings yet

- Production & Cost: S. M. Zahid IqbalDocument19 pagesProduction & Cost: S. M. Zahid IqbalMd. Rifat Ul Alom Roni 2012809630No ratings yet

- Example Example: (5.5) : Continuation of (5.4)Document22 pagesExample Example: (5.5) : Continuation of (5.4)KoyakuNo ratings yet

- CH 21 Production CostsDocument31 pagesCH 21 Production CostsEshrat Tarabi Shimla 2211281030No ratings yet

- Aggregate Supply & Aggregate DemandDocument51 pagesAggregate Supply & Aggregate DemandRahul ShakyaNo ratings yet

- DSGE Lecture 4 - FES - 00002Document17 pagesDSGE Lecture 4 - FES - 00002imkroslayNo ratings yet

- CH 21 Production CostsDocument31 pagesCH 21 Production CostsLutfun Nesa Aysha 1831892630No ratings yet

- Determination of The Optimal Capital InvestmentDocument34 pagesDetermination of The Optimal Capital InvestmentKoyakuNo ratings yet

- Chapter 8 SlidesDocument35 pagesChapter 8 SlidesAshish ShuklaNo ratings yet

- Macro Economics Unit UpdatedDocument62 pagesMacro Economics Unit UpdatedAnshumaan PatroNo ratings yet

- ECN 3422 - Lecture 1 - 2021.09.21Document21 pagesECN 3422 - Lecture 1 - 2021.09.21Cornelius MasikiniNo ratings yet

- Chapter 3 - 2Document34 pagesChapter 3 - 2Rasheed ZedanNo ratings yet

- Wage Determination: Collective BargainingDocument46 pagesWage Determination: Collective BargainingKoyakuNo ratings yet

- Lecture 5 (Chapters 21 and 22)Document22 pagesLecture 5 (Chapters 21 and 22)raymondNo ratings yet

- Aggregate Expenditure and Equilibrium OutputDocument69 pagesAggregate Expenditure and Equilibrium OutputhongphakdeyNo ratings yet

- Goods and Financial Market EquilibriumDocument25 pagesGoods and Financial Market EquilibriumPrathamesh RamNo ratings yet

- Econ101B NotesDocument97 pagesEcon101B NotesYilena HsueNo ratings yet

- Macro !! Cha 3 $ 4Document54 pagesMacro !! Cha 3 $ 4dehinnetagimasNo ratings yet

- Unemployment and The Foundations of Aggregate SupplyDocument39 pagesUnemployment and The Foundations of Aggregate SupplyannsaralondeNo ratings yet

- Econ 203 Lecture 32Document20 pagesEcon 203 Lecture 32yourguy223No ratings yet

- Chapter 4 Production and CostDocument25 pagesChapter 4 Production and Costaudreychoga5No ratings yet

- EC 102 Revisions Lectures - Macro 2013Document56 pagesEC 102 Revisions Lectures - Macro 2013TylerTangTengYangNo ratings yet

- Increase in Demand and SupplyDocument9 pagesIncrease in Demand and SupplyJon LeinsNo ratings yet

- Consumption Function and MultiplierDocument24 pagesConsumption Function and MultiplierVikku AgarwalNo ratings yet

- Theories of Multiplier, Accelerator and Business CyclesDocument30 pagesTheories of Multiplier, Accelerator and Business CyclesProfessor Tarun DasNo ratings yet

- Business Cycles: The TheoryDocument39 pagesBusiness Cycles: The TheorySagar IndranNo ratings yet

- 3.5 Inflation and Financial Appraisal - ADJT LECTUREDocument58 pages3.5 Inflation and Financial Appraisal - ADJT LECTUREDina AyundariNo ratings yet

- T NG H P GraphsDocument8 pagesT NG H P GraphsAnnie DuolingoNo ratings yet

- Determination of Income and EmploymentDocument30 pagesDetermination of Income and EmploymentShrey GoelNo ratings yet

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Proclamation of Independence, 17 April 1971: East West University GEN 226 / Lecture 17Document11 pagesProclamation of Independence, 17 April 1971: East West University GEN 226 / Lecture 17Md SafiNo ratings yet

- EWU. GEN 226. Lecture 19. StudentsDocument5 pagesEWU. GEN 226. Lecture 19. StudentsMd SafiNo ratings yet

- 3A. EWU. GEN 226. Lecture 19. Addll. Peoples WarDocument5 pages3A. EWU. GEN 226. Lecture 19. Addll. Peoples WarMd SafiNo ratings yet

- 5A. EWU. GEN 226. Lecture 21. Addll. Super Powers in Liberation WarDocument5 pages5A. EWU. GEN 226. Lecture 21. Addll. Super Powers in Liberation WarMd SafiNo ratings yet

- EWU. GEN 226. Lecture 21. StudentsDocument4 pagesEWU. GEN 226. Lecture 21. StudentsMd SafiNo ratings yet

- Formation of Joint Indo-Bangladesh Forces and The Final VictoryDocument9 pagesFormation of Joint Indo-Bangladesh Forces and The Final VictoryMd SafiNo ratings yet

- Note On Chain-Weighted Real GDPDocument2 pagesNote On Chain-Weighted Real GDPMd SafiNo ratings yet

- Not To Be Shared With AnyoneDocument2 pagesNot To Be Shared With AnyoneMd SafiNo ratings yet

- Peace Committee: East West University GEN 226 / Lecture 22Document10 pagesPeace Committee: East West University GEN 226 / Lecture 22Md SafiNo ratings yet

- Company and Marketing Strategy: Partnering To Build Customer RelationshipsDocument24 pagesCompany and Marketing Strategy: Partnering To Build Customer RelationshipsMd SafiNo ratings yet

- Solution of Sample Question PDFDocument5 pagesSolution of Sample Question PDFMd SafiNo ratings yet

- EWU. GEN 226. Lecture 18. StudentsDocument12 pagesEWU. GEN 226. Lecture 18. StudentsMd SafiNo ratings yet

- Proclamation of Independence, 17 April 1971: East West University GEN 226 / Lecture 17Document11 pagesProclamation of Independence, 17 April 1971: East West University GEN 226 / Lecture 17Md SafiNo ratings yet

- Supplementary 2Document7 pagesSupplementary 2Md SafiNo ratings yet

- Entropy: Gibbs' Paradox and The Definition of EntropyDocument4 pagesEntropy: Gibbs' Paradox and The Definition of Entropysantiago bermudezNo ratings yet

- Patrick Minford, David Peel - Advanced Macroeconomics - A Primer (2019, Edward Elgar) - Libgen - LiDocument517 pagesPatrick Minford, David Peel - Advanced Macroeconomics - A Primer (2019, Edward Elgar) - Libgen - LiJuan Salvador Domandl100% (1)

- Jurnal 1 PDFDocument11 pagesJurnal 1 PDFDoraemon BAHASA INDONESIANo ratings yet

- IS-LM ModelDocument6 pagesIS-LM ModelAnand Kant JhaNo ratings yet

- Macroeconomics Course Outline MSC 1stDocument3 pagesMacroeconomics Course Outline MSC 1stishtiaqlodhranNo ratings yet

- MACRO 1 NotesDocument33 pagesMACRO 1 NotesPride ChinonzuraNo ratings yet

- Econ 2002 Course Outline 2018Document3 pagesEcon 2002 Course Outline 2018Simone BrownNo ratings yet

- 11 Boyles Law LABSu2020 Online VersionDocument4 pages11 Boyles Law LABSu2020 Online VersionAcademic NerdsNo ratings yet

- Deficit Financing Theory and Practice in BangladeshDocument12 pagesDeficit Financing Theory and Practice in BangladeshshuvrodeyNo ratings yet

- Monetary PolicyDocument34 pagesMonetary PolicyYogesh Kende89% (9)

- Solved Wayne Angell A Former Fed Governor Stated in An EditorialDocument1 pageSolved Wayne Angell A Former Fed Governor Stated in An EditorialM Bilal SaleemNo ratings yet

- PHY412A First Course HandoutDocument1 pagePHY412A First Course Handoutsomya diwakarNo ratings yet

- Input Output AnalysisDocument5 pagesInput Output AnalysisafguzmanNo ratings yet

- AP Macroeconomics Page 1 of 5 Assignment: Apply The Keynesian Model To AD/ASDocument6 pagesAP Macroeconomics Page 1 of 5 Assignment: Apply The Keynesian Model To AD/ASMadiNo ratings yet

- Application of Macroeconomics Theory As Basis For UnderstandingDocument24 pagesApplication of Macroeconomics Theory As Basis For UnderstandingTHERESA SUBRADONo ratings yet

- GDP Ranked by Country 2020Document22 pagesGDP Ranked by Country 2020Jun VarNo ratings yet

- TUT Macro Unit 4 (Answer)Document6 pagesTUT Macro Unit 4 (Answer)张宝琪No ratings yet

- Business Cycle 1Document7 pagesBusiness Cycle 1SaudNo ratings yet

- Shahrear NasrinDocument17 pagesShahrear NasrinShimu ShahrearNo ratings yet

- ECO 423 MACROECONOMICS III SyllabusDocument2 pagesECO 423 MACROECONOMICS III Syllabusashraf khanNo ratings yet

- MacroeconomicsDocument14 pagesMacroeconomicsAshish ParidaNo ratings yet

- Mc-Sse 8 Macroeconomics Group V : Fiscal PolicyDocument35 pagesMc-Sse 8 Macroeconomics Group V : Fiscal PolicyMaria Cristina ImportanteNo ratings yet

- Real Vs Nominal Values (Blank)Document4 pagesReal Vs Nominal Values (Blank)Prineet AnandNo ratings yet

- Chapter 8-9 International Monetary SystemDocument34 pagesChapter 8-9 International Monetary SystemGaurav GuptaNo ratings yet

- Micro Midterm May 2015ADocument7 pagesMicro Midterm May 2015ATriet TruongNo ratings yet

- Data Mentah18 Desember 2020Document23 pagesData Mentah18 Desember 2020fathur abrarNo ratings yet

- Troy University in VietnamDocument8 pagesTroy University in VietnamQuỳnh Trang NguyễnNo ratings yet

- Guided Notes Unit 5 - Macroeconomics - Economic Challenges, GDP and Growth, and LaborDocument4 pagesGuided Notes Unit 5 - Macroeconomics - Economic Challenges, GDP and Growth, and LaborNicols FleurismaNo ratings yet