You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Calpine RGGI LawsuitDocument208 pagesCalpine RGGI LawsuitCommonwealth FoundationNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Service Manual Tosoh Aia360Document4 pagesService Manual Tosoh Aia360OmerNo ratings yet

- Start Where You Are A Journal For Self Exploration PDFDocument1 pageStart Where You Are A Journal For Self Exploration PDFNyemwerai Muterere22% (9)

- Impact of Government Policy and Regulations in BankingDocument65 pagesImpact of Government Policy and Regulations in BankingNiraj ThapaNo ratings yet

- Family Law Outline RevisedDocument11 pagesFamily Law Outline RevisedAdriana CarinanNo ratings yet

- Rheumatoid ArthritisDocument15 pagesRheumatoid ArthritisPJHG100% (2)

- XXXXXDocument38 pagesXXXXXGarrett HughesNo ratings yet

- Pennsylvania Government Flow ChartDocument1 pagePennsylvania Government Flow ChartCommonwealth FoundationNo ratings yet

- Obamacare Has Harmed Pennsylvania FamiliesDocument2 pagesObamacare Has Harmed Pennsylvania FamiliesCommonwealth FoundationNo ratings yet

- UFCW 1776 LetterDocument1 pageUFCW 1776 LetterCommonwealth FoundationNo ratings yet

- Commonwealth Foundation Testimony On RGGI 10.28.19Document3 pagesCommonwealth Foundation Testimony On RGGI 10.28.19Commonwealth FoundationNo ratings yet

- Constitutional and Legal Requirements of A Balanced Budget in PennsylvaniaDocument1 pageConstitutional and Legal Requirements of A Balanced Budget in PennsylvaniaCommonwealth FoundationNo ratings yet

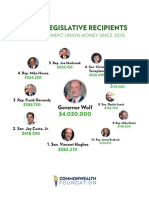

- Top 10 Legislative Recipients of Union Political MoneyDocument1 pageTop 10 Legislative Recipients of Union Political MoneyCommonwealth FoundationNo ratings yet

- Charter Testimony October 2016Document6 pagesCharter Testimony October 2016Commonwealth FoundationNo ratings yet

- Vape Tax VictimsDocument2 pagesVape Tax VictimsCommonwealth FoundationNo ratings yet

- Memo in Support of DOC and PBPP MergerDocument2 pagesMemo in Support of DOC and PBPP MergerCommonwealth FoundationNo ratings yet

- Pennsylvanians Flee From High TaxesDocument4 pagesPennsylvanians Flee From High TaxesCommonwealth FoundationNo ratings yet

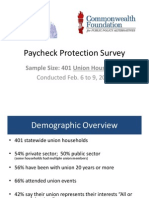

- Paycheck Protection Survey: Sample Size: 401 Union HouseholdsDocument7 pagesPaycheck Protection Survey: Sample Size: 401 Union HouseholdsCommonwealth FoundationNo ratings yet

- Mary Isenhour Letter To PERCDocument2 pagesMary Isenhour Letter To PERCCommonwealth FoundationNo ratings yet

- How Workers Are Forced To Fund Attack AdsDocument2 pagesHow Workers Are Forced To Fund Attack AdsCommonwealth FoundationNo ratings yet

- AFSCME Local 2528 PAC SolicitationDocument3 pagesAFSCME Local 2528 PAC SolicitationCommonwealth FoundationNo ratings yet

- Pennsylvania Sat 1986-2011 (Intern's Conflicted Copy 2016-06-16)Document13 pagesPennsylvania Sat 1986-2011 (Intern's Conflicted Copy 2016-06-16)Commonwealth FoundationNo ratings yet

- SAT Scores by State 2015Document2 pagesSAT Scores by State 2015Commonwealth FoundationNo ratings yet

- PA Pension ReformDocument31 pagesPA Pension ReformCommonwealth FoundationNo ratings yet

- Commonwealth Foundation RTKDocument10 pagesCommonwealth Foundation RTKCommonwealth FoundationNo ratings yet

- Patient-Centered Medicaid Reform ActDocument14 pagesPatient-Centered Medicaid Reform ActCommonwealth FoundationNo ratings yet

- What Is Paycheck Protection?Document1 pageWhat Is Paycheck Protection?Commonwealth FoundationNo ratings yet

- DPW Welfare Waste, Fraud & Abuse SavingsDocument2 pagesDPW Welfare Waste, Fraud & Abuse SavingsCommonwealth FoundationNo ratings yet

- Pennsylvania's Pension Crisis: Facts and MythsDocument2 pagesPennsylvania's Pension Crisis: Facts and MythsCommonwealth FoundationNo ratings yet

- Public Pensions: Past, Present and FutureDocument2 pagesPublic Pensions: Past, Present and FutureCommonwealth FoundationNo ratings yet

- Liquor Privatization Facts and MythsDocument2 pagesLiquor Privatization Facts and MythsCommonwealth FoundationNo ratings yet

- Social Impacts of Liquor PrivatizationDocument6 pagesSocial Impacts of Liquor PrivatizationCommonwealth FoundationNo ratings yet

- Comparison ChartDocument1 pageComparison ChartCommonwealth FoundationNo ratings yet

- FM3 Privatization PollDocument15 pagesFM3 Privatization PollCommonwealth FoundationNo ratings yet

- Letter To Corbett: Reject Medicaid ExpansionDocument4 pagesLetter To Corbett: Reject Medicaid ExpansionCommonwealth FoundationNo ratings yet

- Unsinkable: The True Story of Pennsylvania's Sinking Pension SystemDocument1 pageUnsinkable: The True Story of Pennsylvania's Sinking Pension SystemCommonwealth FoundationNo ratings yet

- Master of Arts in Education Major in Education Management: Development Administration and Education SubjectDocument12 pagesMaster of Arts in Education Major in Education Management: Development Administration and Education SubjectJeai Rivera EvangelistaNo ratings yet

- Instant Download Developing Management Skills 10th Edition Whetten Test Bank PDF Full ChapterDocument33 pagesInstant Download Developing Management Skills 10th Edition Whetten Test Bank PDF Full Chapterdonaldvioleti7o100% (9)

- Toefl Exercise 1Document9 pagesToefl Exercise 1metaNo ratings yet

- Sara Lee Philippines Inc Vs Macatlang, G.R. No. 180147, June 4, 2014Document15 pagesSara Lee Philippines Inc Vs Macatlang, G.R. No. 180147, June 4, 2014duanepoNo ratings yet

- Biotransformation of DrugsDocument36 pagesBiotransformation of DrugszeepharmacistNo ratings yet

- Laboratory 1. ANALYSIS OF PLANT PIGMENTS USING PAPER CHROMATOGRAPHYDocument8 pagesLaboratory 1. ANALYSIS OF PLANT PIGMENTS USING PAPER CHROMATOGRAPHYGualberto Tampol Jr.No ratings yet

- The BoxDocument6 pagesThe BoxDemian GaylordNo ratings yet

- Orange PeelDocument2 pagesOrange PeelCharul Shukla100% (1)

- Danamma Vs AmarDocument13 pagesDanamma Vs AmarParthiban SekarNo ratings yet

- Lesson Plan 9th Grade ScienceDocument2 pagesLesson Plan 9th Grade Scienceapi-316973807No ratings yet

- What Is Thick Film Ceramic PCBDocument13 pagesWhat Is Thick Film Ceramic PCBjackNo ratings yet

- Guidelines: VSBK Design OptionDocument60 pagesGuidelines: VSBK Design OptionChrisNo ratings yet

- Ageing Baby BoomersDocument118 pagesAgeing Baby Boomersstephloh100% (1)

- Nano Technology Oil RefiningDocument19 pagesNano Technology Oil RefiningNikunj Agrawal100% (1)

- Map of Jeju: For Muslim TouristsDocument7 pagesMap of Jeju: For Muslim TouristslukmannyeoNo ratings yet

- Legal AgreementDocument2 pagesLegal AgreementMohd NadeemNo ratings yet

- 16 Leases (Lessee) s19 FinalDocument35 pages16 Leases (Lessee) s19 FinalNosipho NyathiNo ratings yet

- Technipfmc Corporate Brochure en 2018Document7 pagesTechnipfmc Corporate Brochure en 2018Sivaji RajinikanthNo ratings yet

- India Is My CountryDocument2 pagesIndia Is My CountryAbi MuthukumarNo ratings yet

- MC DuroDesign EDocument8 pagesMC DuroDesign Epetronela.12No ratings yet

- Structural Elements For Typical BridgesDocument3 pagesStructural Elements For Typical BridgesJoe A. CagasNo ratings yet

- 01 B744 B1 ATA 23 Part2Document170 pages01 B744 B1 ATA 23 Part2NadirNo ratings yet

- Hampers 2023 - Updted Back Cover - FADocument20 pagesHampers 2023 - Updted Back Cover - FAHaris HaryadiNo ratings yet

- Earth Art Michael Heizer The CityDocument2 pagesEarth Art Michael Heizer The Cityccxx09.cxNo ratings yet