You might also like

- Substantive Test of CashDocument19 pagesSubstantive Test of Cashshalom catedrilla100% (1)

- Cash & Cash Equivalents, Lecture &exercisesDocument16 pagesCash & Cash Equivalents, Lecture &exercisesDessa GarongNo ratings yet

- Receivables (Handouts)Document6 pagesReceivables (Handouts)Crystal Padilla100% (1)

- Taxation For Dummies PDFDocument13 pagesTaxation For Dummies PDFLiz VillarazaNo ratings yet

- Test of Controls Procedure PDFDocument6 pagesTest of Controls Procedure PDFNatsu DragneelNo ratings yet

- O Level Business Studies NotesDocument14 pagesO Level Business Studies NotesFarhan Arshad60% (5)

- Chapter 4 - 6 Transaction CyclesDocument8 pagesChapter 4 - 6 Transaction CyclesJessa Mae Banse Limosnero25% (4)

- Department of Accountancy: Page - 1Document47 pagesDepartment of Accountancy: Page - 1NoroNo ratings yet

- Auditing Theory-A Guide in Understanding The PSA (2018) SalosagcolDocument8 pagesAuditing Theory-A Guide in Understanding The PSA (2018) SalosagcolI am JacobNo ratings yet

- RequirementsDocument174 pagesRequirementsSourav KumarNo ratings yet

- Applied Auditing Audit of Receivables Problem 1: QuestionsDocument9 pagesApplied Auditing Audit of Receivables Problem 1: QuestionsPau SantosNo ratings yet

- Audit of Receivables WubexDocument9 pagesAudit of Receivables WubexZelalem HassenNo ratings yet

- PSBA - Audit of InventoriesDocument14 pagesPSBA - Audit of InventoriesThalia UyNo ratings yet

- Ethical IssuesDocument5 pagesEthical IssuesRamapriyaiyengarNo ratings yet

- Chapter 12 - Assurance & Other Related ServicesDocument5 pagesChapter 12 - Assurance & Other Related ServicesellieNo ratings yet

- Chapter 1 Audit of Cash and Cash EquivalentsDocument129 pagesChapter 1 Audit of Cash and Cash Equivalentsdeborah grace sagarioNo ratings yet

- Income Taxation Capital AssetDocument93 pagesIncome Taxation Capital AssetGelyn Cruz100% (1)

- Module 2 ReceivablesDocument15 pagesModule 2 ReceivablesKim JisooNo ratings yet

- Auditing Problems: Audit of ReceivablesDocument4 pagesAuditing Problems: Audit of ReceivablesLaong laanNo ratings yet

- Auditing Theory MCQs (Continuation) by Salosagcol With AnswersDocument21 pagesAuditing Theory MCQs (Continuation) by Salosagcol With AnswersYeovil Pansacala67% (3)

- 06 ReceivableDocument104 pages06 Receivablefordan Zodorovic100% (4)

- Accounting - 1st Quiz Cash and Cash Equivalent 2011Document2 pagesAccounting - 1st Quiz Cash and Cash Equivalent 2011Louie De La Torre40% (5)

- Audit of Receivables Lecture NotesDocument10 pagesAudit of Receivables Lecture NotesDebs Fanoga100% (1)

- AP 08 Substantive Audit Tests of EquityDocument2 pagesAP 08 Substantive Audit Tests of EquityJobby JaranillaNo ratings yet

- Substantive Audit Testing CompDocument36 pagesSubstantive Audit Testing CompJoshua WacanganNo ratings yet

- Audit of ReceivablesDocument48 pagesAudit of Receivablescarl fuerzasNo ratings yet

- Mas Usl ReviewerDocument10 pagesMas Usl RevieweriptrcrmlNo ratings yet

- Audit of Cash and Cash EquivalentsDocument10 pagesAudit of Cash and Cash EquivalentsVel JuneNo ratings yet

- Audit of The Expenditure Cycle: Tests of Controls and Substantive Tests of Transactions - IDocument19 pagesAudit of The Expenditure Cycle: Tests of Controls and Substantive Tests of Transactions - Itankofdoom 4100% (1)

- Audit PracticeDocument161 pagesAudit PracticeKez Max100% (1)

- Apparel Dictionary Very UsefulDocument9 pagesApparel Dictionary Very Usefulmorshed_mahamud7055No ratings yet

- Retail Invoice Infiniti Retail Limited Trading As CromaDocument4 pagesRetail Invoice Infiniti Retail Limited Trading As CromaSurya PrakashNo ratings yet

- Auditing Theory Audit of The Inventory and Warehousing CycleDocument15 pagesAuditing Theory Audit of The Inventory and Warehousing CycleMark Anthony Tibule100% (2)

- Audit of Property, Plant and Equipment (Document35 pagesAudit of Property, Plant and Equipment (Mohd Mirul86% (21)

- 1.0 Notes Cash and Cash Equivalents 1.0 Notes Cash and Cash EquivalentsDocument181 pages1.0 Notes Cash and Cash Equivalents 1.0 Notes Cash and Cash EquivalentsLawrence YusiNo ratings yet

- Audit of ReceivableDocument4 pagesAudit of ReceivableMark Lord Morales Bumagat100% (2)

- Audit of Receivables-1Document16 pagesAudit of Receivables-1jennyMBNo ratings yet

- Audit DocumentationDocument6 pagesAudit Documentationemc2_mcv100% (4)

- Auditing Problems Final Preboard Examination Batch 87 SET: Cpa Review School of The Philippines ManilaDocument12 pagesAuditing Problems Final Preboard Examination Batch 87 SET: Cpa Review School of The Philippines ManilaMarwin AceNo ratings yet

- Quiz 1 Specialized IndustriesDocument5 pagesQuiz 1 Specialized IndustriesLyca Mae CubangbangNo ratings yet

- Guide To Retail Math Key Formulas PDFDocument1 pageGuide To Retail Math Key Formulas PDFYusuf KandemirNo ratings yet

- Auditing Specialised IndustryDocument3 pagesAuditing Specialised IndustryAcheampong AnthonyNo ratings yet

- AP 5905 InventoriesDocument9 pagesAP 5905 Inventoriesxxxxxxxxx67% (3)

- AP 1403 Receivables Auditing ProblemsDocument18 pagesAP 1403 Receivables Auditing ProblemsДжен Акино ОганизаNo ratings yet

- Comprehensive Audit Problem Julie AngeloDocument8 pagesComprehensive Audit Problem Julie AngeloAnonymous LC5kFdtcNo ratings yet

- Contract To Sell - Luzon Development Bank vs. EnriquezDocument2 pagesContract To Sell - Luzon Development Bank vs. EnriquezJack Bryan Hufano50% (2)

- Auditing Problem ReviewerDocument12 pagesAuditing Problem ReviewerJan Amora Pueblo0% (4)

- Audit Prob - ReceivablesDocument27 pagesAudit Prob - ReceivablesCharis Marie Urgel100% (3)

- CPAR AT - Other Assurance EngagementsDocument9 pagesCPAR AT - Other Assurance EngagementsJohn Carlo CruzNo ratings yet

- Vat and Completion of Acc Cycle For MerchandisingDocument7 pagesVat and Completion of Acc Cycle For MerchandisingLouie De La TorreNo ratings yet

- Auditing The Revenue Receipt Cycle QuizDocument2 pagesAuditing The Revenue Receipt Cycle Quizgaler LedesmaNo ratings yet

- Joan Holtz Case SolutionsDocument5 pagesJoan Holtz Case SolutionsRahul KaulNo ratings yet

- 8 Audit of LiabilitiesDocument4 pages8 Audit of LiabilitiesCarieza CardenasNo ratings yet

- Audit of CashDocument14 pagesAudit of CashMarah ArcederaNo ratings yet

- Week 1 Operations AuditDocument4 pagesWeek 1 Operations Audityen claveNo ratings yet

- Auditing ProblemsDocument10 pagesAuditing ProblemsLouie De La TorreNo ratings yet

- Audit of ReceivablesDocument4 pagesAudit of ReceivablesClarisse AnnNo ratings yet

- Audit of ReceivablesDocument3 pagesAudit of ReceivablesJhedz CartasNo ratings yet

- 11 - Substantive Tests of Property, Plant and EquipmentDocument27 pages11 - Substantive Tests of Property, Plant and EquipmentArleneCastroNo ratings yet

- Audit of ReceivablesDocument9 pagesAudit of Receivablesmissy100% (2)

- Ap-1403 ReceivablesDocument18 pagesAp-1403 Receivableschowchow123No ratings yet

- Audit of EquityDocument5 pagesAudit of EquityKarlo Jude Acidera0% (1)

- Chapter 2 Audit Cash PDFDocument6 pagesChapter 2 Audit Cash PDFalemayehu100% (2)

- MODAUD1 UNIT 2 - Audit of Cash and Cash TransactionsDocument8 pagesMODAUD1 UNIT 2 - Audit of Cash and Cash TransactionsJake Bundok100% (1)

- Receipt & Disbursment Cycles: Audit of Cash Balance: Auditing ProblemsDocument6 pagesReceipt & Disbursment Cycles: Audit of Cash Balance: Auditing ProblemsJohn Lester DocaNo ratings yet

- Audit of Cash TheoryDocument7 pagesAudit of Cash TheoryShulamite Ignacio GarciaNo ratings yet

- AP Lesson 2Document13 pagesAP Lesson 2Joanne RomaNo ratings yet

- Auditing Problems: Audit of ReceivablesDocument4 pagesAuditing Problems: Audit of ReceivablesMa. Trixcy De VeraNo ratings yet

- 00 Quick Notes - Revenue and Receipt Cycle PDFDocument5 pages00 Quick Notes - Revenue and Receipt Cycle PDFBecky GonzagaNo ratings yet

- AttachmentDocument14 pagesAttachmentAngelo Jose BalalongNo ratings yet

- Module 2 ReceivablesDocument16 pagesModule 2 ReceivablesEarl ENo ratings yet

- ReceivablesDocument16 pagesReceivablesJanela Venice SantosNo ratings yet

- Taxation-Not CompleteDocument13 pagesTaxation-Not CompleteLouie De La TorreNo ratings yet

- Job Arrangement Letter-FSOLDocument11 pagesJob Arrangement Letter-FSOLLouie De La TorreNo ratings yet

- Student Apprenticeship Program (Sap) :: Initial Document RequirementsDocument1 pageStudent Apprenticeship Program (Sap) :: Initial Document RequirementsLouie De La TorreNo ratings yet

- Answers - V2Chapter 1 2012Document10 pagesAnswers - V2Chapter 1 2012Christopher Diaz0% (1)

- Answers - V2Chapter 6 2012Document6 pagesAnswers - V2Chapter 6 2012Rhei BarbaNo ratings yet

- Enrollment GuideDocument3 pagesEnrollment GuideLouie De La TorreNo ratings yet

- OJT Apprentice LedgerDocument1 pageOJT Apprentice LedgerLouie De La Torre50% (2)

- EdsaDocument1 pageEdsaLouie De La TorreNo ratings yet

- NSTP Community Immersion Project Completion Report: Names Section Numbers SignaturesDocument2 pagesNSTP Community Immersion Project Completion Report: Names Section Numbers SignaturesLouie De La TorreNo ratings yet

- Audtng2 Syllabus Revised May 2013Document7 pagesAudtng2 Syllabus Revised May 2013Louie De La TorreNo ratings yet

- Objectives: Dianne A. ChuaDocument2 pagesObjectives: Dianne A. ChuaLouie De La TorreNo ratings yet

- Ddddddddswa: 4 3 2 WarehouseDocument1 pageDdddddddswa: 4 3 2 WarehouseLouie De La TorreNo ratings yet

- Basic Acctg MidtermDocument8 pagesBasic Acctg MidtermLouie De La Torre100% (3)

- 180 84 1 PBDocument12 pages180 84 1 PBLouie De La TorreNo ratings yet

- 1 CVPDocument38 pages1 CVPLouie De La TorreNo ratings yet

- Suggested SolutionsDocument2 pagesSuggested SolutionsLouie De La TorreNo ratings yet

- 361 Chapter 9 MC SolutionsDocument24 pages361 Chapter 9 MC SolutionsLouie De La TorreNo ratings yet

- 6.prep of Trial BalanceDocument20 pages6.prep of Trial BalanceLouie De La TorreNo ratings yet

- Marketing Strategies of EXIM Bank Limited Bangladesh: Abdullah Al Mamun, MDDocument68 pagesMarketing Strategies of EXIM Bank Limited Bangladesh: Abdullah Al Mamun, MDshahdatzNo ratings yet

- Working - Group - Scenario - Rice NoodleDocument6 pagesWorking - Group - Scenario - Rice Noodletamvan68No ratings yet

- Luxury Retail Marketing Manager in Yardley PA Resume Dina GordinDocument2 pagesLuxury Retail Marketing Manager in Yardley PA Resume Dina GordinDinaGordinNo ratings yet

- Curing The Sales Marketing DivideDocument4 pagesCuring The Sales Marketing DivideMicheal GoodmanNo ratings yet

- Laxmi Engineering Works Vs P.S.GDocument17 pagesLaxmi Engineering Works Vs P.S.Gjeevan_v_mNo ratings yet

- 047 Country of Origin Effect On Purchasing IntentionDocument18 pages047 Country of Origin Effect On Purchasing Intentioniis rifiNo ratings yet

- PS2Document2 pagesPS2fego2008100% (1)

- 1230 Why People Believe Peter PopoffDocument3 pages1230 Why People Believe Peter PopoffbmarksNo ratings yet

- Activity Sheet 9-1 Consumer-QuizDocument2 pagesActivity Sheet 9-1 Consumer-QuizJhon Vincent Draug PosadasNo ratings yet

- AMD - Note On PV Ratio-1Document4 pagesAMD - Note On PV Ratio-1Bharath s kashyapNo ratings yet

- Sales PromotionDocument29 pagesSales PromotionAnonymous uxd1ydNo ratings yet

- Business Plan SECTION 6Document6 pagesBusiness Plan SECTION 6hazimNo ratings yet

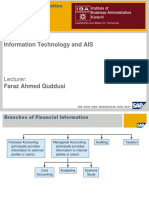

- Role of AISDocument20 pagesRole of AISFaraz Ahmed QuddusiNo ratings yet

- Re An Advocate - (1964) 1 MLJ 1Document8 pagesRe An Advocate - (1964) 1 MLJ 1Nur Fatin Mohamad FaridNo ratings yet

- Eurocash Business Strategy AnalysisDocument6 pagesEurocash Business Strategy AnalysiskshywyNo ratings yet

- Employee BehaviourDocument55 pagesEmployee BehaviourRajeswari AcharyaNo ratings yet

- Bain Worldwide Luxury Goods Report 2014Document36 pagesBain Worldwide Luxury Goods Report 2014Felipe MNP0% (2)

- Business Plan ReportDocument2 pagesBusiness Plan Reportsimranarora2007No ratings yet

- Sanitary NapkinsDocument11 pagesSanitary NapkinsHadist Buchori0% (1)