You might also like

- Introduction to Project Finance in Renewable Energy Infrastructure: Including Public-Private Investments and Non-Mature MarketsFrom EverandIntroduction to Project Finance in Renewable Energy Infrastructure: Including Public-Private Investments and Non-Mature MarketsNo ratings yet

- Risk Management in Construction Industry: Mr. Satish K. Kamane, Mr. Sandip A. MahadikDocument7 pagesRisk Management in Construction Industry: Mr. Satish K. Kamane, Mr. Sandip A. MahadikAnusha AshokNo ratings yet

- What is Project FinanceDocument29 pagesWhat is Project FinanceGeorgeNo ratings yet

- Unlocking Capital: The Power of Bonds in Project FinanceFrom EverandUnlocking Capital: The Power of Bonds in Project FinanceNo ratings yet

- PGP IDM-31 - Project Risk Mgmt.Document33 pagesPGP IDM-31 - Project Risk Mgmt.suhas vermaNo ratings yet

- Qualitative Risk Assessment and Mitigation Measures For Real Estate Projects in MaharashtraDocument9 pagesQualitative Risk Assessment and Mitigation Measures For Real Estate Projects in MaharashtraInternational Jpurnal Of Technical Research And ApplicationsNo ratings yet

- Society of Construction Law (UAE)Document11 pagesSociety of Construction Law (UAE)Ahmed AbdulShafiNo ratings yet

- Risk Assessment in Construction ProjectsDocument5 pagesRisk Assessment in Construction ProjectsIJRASETPublicationsNo ratings yet

- Providing Mitigation Startegies Arising in Infrastructure ProjectsDocument20 pagesProviding Mitigation Startegies Arising in Infrastructure ProjectsAritra KeshNo ratings yet

- Transferring Construction RisksDocument18 pagesTransferring Construction RiskswhyoNo ratings yet

- International Project Finance: Chiemezie EjinimmaDocument15 pagesInternational Project Finance: Chiemezie EjinimmaAlihayderNo ratings yet

- Journal of Structured Finance AcuLeadDocument24 pagesJournal of Structured Finance AcuLeadAtanu MukherjeeNo ratings yet

- Risk ManagementDocument18 pagesRisk ManagementAnusha KishoreNo ratings yet

- Ijtra1505236 PDFDocument9 pagesIjtra1505236 PDFRushi NaikNo ratings yet

- Risk AssignmentDocument53 pagesRisk AssignmentNafiz ImtiazNo ratings yet

- Risk Analysis & Assessment in Nigerian Banks IIDocument16 pagesRisk Analysis & Assessment in Nigerian Banks IIShowman4100% (1)

- A Firm Foundation For Project FinanceDocument6 pagesA Firm Foundation For Project FinanceMarc BernardNo ratings yet

- Chapter 04Document13 pagesChapter 04sanjaymits2No ratings yet

- Contract DocumentDocument78 pagesContract DocumentEngineeri TadiyosNo ratings yet

- Group 1 RMFD SynopsisDocument7 pagesGroup 1 RMFD SynopsisguptadivyeNo ratings yet

- PRM Chapter 1Document9 pagesPRM Chapter 1Kan Fock-KuiNo ratings yet

- SEBI Project Finance GuidelinesDocument21 pagesSEBI Project Finance GuidelinesSachin ShintreNo ratings yet

- Project Finance Assignment: Student Name Institutional Affiliation Course Number and Name Professor's Name DateDocument12 pagesProject Finance Assignment: Student Name Institutional Affiliation Course Number and Name Professor's Name DateFREDRICKNo ratings yet

- 41 - KTS-CM-13Document8 pages41 - KTS-CM-13IrenataNo ratings yet

- The Nature of Credit Risk in Project FinanceDocument4 pagesThe Nature of Credit Risk in Project FinanceSayon DasNo ratings yet

- Risk Analysis Project FinanceDocument181 pagesRisk Analysis Project Financeshah_harshit25100% (1)

- Infrastructure Risk ManagementDocument16 pagesInfrastructure Risk ManagementNihar NanyamNo ratings yet

- Tianjin PlasticsDocument9 pagesTianjin PlasticsmalikatjuhNo ratings yet

- Lecture 2 - Risk ManagementDocument41 pagesLecture 2 - Risk ManagementchristopherNo ratings yet

- Energy Industry - Evolving Risk - MarshDocument28 pagesEnergy Industry - Evolving Risk - MarshbxbeautyNo ratings yet

- Adekoya, Adebanji - Managing Non-Technical Risk in E and P ProjectsDocument6 pagesAdekoya, Adebanji - Managing Non-Technical Risk in E and P ProjectsU4rayNo ratings yet

- Rating Methodology For Project Finance TransactionsDocument6 pagesRating Methodology For Project Finance TransactionsAlka KakkarNo ratings yet

- Risks Associated With International Project Financing: Submitted By: Sajal Nahar G-44 Akshay Arora G-48Document13 pagesRisks Associated With International Project Financing: Submitted By: Sajal Nahar G-44 Akshay Arora G-48sajalNo ratings yet

- BSCE4-E Manibog Mart-Lliam Activity 5 Research-ManuscriptDocument20 pagesBSCE4-E Manibog Mart-Lliam Activity 5 Research-ManuscriptMiNT MatiasNo ratings yet

- Examining Risk Tolerance in Project-Driven OrganizationDocument5 pagesExamining Risk Tolerance in Project-Driven Organizationapi-3707091No ratings yet

- Risks in Project and Risk Mitigation Measures - An OverviewDocument42 pagesRisks in Project and Risk Mitigation Measures - An OverviewashishNo ratings yet

- A Review of Risk Management Techniques For Construction ProjectsDocument6 pagesA Review of Risk Management Techniques For Construction ProjectsIJRASETPublicationsNo ratings yet

- 1 s2.0 S2405844022030146 MainDocument11 pages1 s2.0 S2405844022030146 MainglifemeashoNo ratings yet

- Giao trinh riskDocument3 pagesGiao trinh riskNguyễn Ngọc QuỳnhNo ratings yet

- Analysis of The Dulles GreenwayDocument21 pagesAnalysis of The Dulles GreenwayRakesh JainNo ratings yet

- Ar2006-0553-0561 Laryea and HughesDocument9 pagesAr2006-0553-0561 Laryea and HughessweetyNo ratings yet

- Chapter Three: Looing at ProjectDocument7 pagesChapter Three: Looing at ProjectMikias EphremNo ratings yet

- Contractorsrisk Paras 0003 File PDFDocument57 pagesContractorsrisk Paras 0003 File PDFRiyasNo ratings yet

- Preliminary Risk Assessment in Project FinanceDocument18 pagesPreliminary Risk Assessment in Project FinanceflichuchaNo ratings yet

- Financial Risks in Construction ProjectsDocument5 pagesFinancial Risks in Construction Projectsalaa jalladNo ratings yet

- Risk ManagementDocument22 pagesRisk Managementاحمد مفرجNo ratings yet

- Managing Healthcare PF Investments.j.jim.20130201.12Document13 pagesManaging Healthcare PF Investments.j.jim.20130201.12Sky walkingNo ratings yet

- Risk Analysis and Management in ConstructionDocument16 pagesRisk Analysis and Management in ConstructionwahyuNo ratings yet

- Day 4 - Operations - Risk ManagementDocument37 pagesDay 4 - Operations - Risk ManagementPhilip CabuhatNo ratings yet

- Jurnal EnglishDocument8 pagesJurnal EnglishAnnurramadhani OciNo ratings yet

- 153 155ncice 078Document4 pages153 155ncice 078Dewa Gede Soja PrabawaNo ratings yet

- Azerbaijan State University of EconomicsDocument15 pagesAzerbaijan State University of EconomicsAnar hummatovNo ratings yet

- FP BaydounDocument16 pagesFP Baydounanon_902477153No ratings yet

- Project Apprisal and FinanceDocument56 pagesProject Apprisal and Financeroypronoy354No ratings yet

- Construction ManagementDocument11 pagesConstruction ManagementSumit PriyamNo ratings yet

- Risk ManagementDocument6 pagesRisk ManagementLaprick MwangiNo ratings yet

- Contractorsrisk Paras 0003 File PDFDocument57 pagesContractorsrisk Paras 0003 File PDFMauro MLRNo ratings yet

- Lecture 5 - Project Finance and Risk ManagementDocument55 pagesLecture 5 - Project Finance and Risk ManagementLewisNo ratings yet

- PRM Chapter 3Document20 pagesPRM Chapter 3Kan Fock-KuiNo ratings yet

- CookiesDocument1 pageCookiesTpomaNo ratings yet

- A Fast Algorithm For The Minimum Covariance Determinant Estimator PDFDocument31 pagesA Fast Algorithm For The Minimum Covariance Determinant Estimator PDFAlvaro MamaniNo ratings yet

- DISCRIMINANT DIAGRAMS For IRON OXIDE Fingerprinting of Mineral Deposit TypesDocument17 pagesDISCRIMINANT DIAGRAMS For IRON OXIDE Fingerprinting of Mineral Deposit Typesjunior.geologiaNo ratings yet

- 10 1002@gj 3693Document18 pages10 1002@gj 3693TpomaNo ratings yet

- Asus 1Document1 pageAsus 1TpomaNo ratings yet

- IoGAS Quick Start Tutorial1Document42 pagesIoGAS Quick Start Tutorial1Pia Lois100% (2)

- Lithos 2001 15Document1 pageLithos 2001 15TpomaNo ratings yet

- AsusDocument1 pageAsusTpomaNo ratings yet

- One (1) Year (U.S. and Latin America) Standard Limited Warranty ("Limited Warranty") For Toshiba Branded Accessories and ElectronicsDocument6 pagesOne (1) Year (U.S. and Latin America) Standard Limited Warranty ("Limited Warranty") For Toshiba Branded Accessories and ElectronicsJosé SayraNo ratings yet

- CHAP4 - Magmatic Sulfide DepositsDocument11 pagesCHAP4 - Magmatic Sulfide DepositsJaime CuyaNo ratings yet

- IoGAS Quick Start Tutorial1Document42 pagesIoGAS Quick Start Tutorial1Pia Lois100% (2)

- 2306 8286 1 PBDocument16 pages2306 8286 1 PBTpomaNo ratings yet

- Jansen 2017Document30 pagesJansen 2017TpomaNo ratings yet

- Rosasetal 2018 SGPCongresoDocument5 pagesRosasetal 2018 SGPCongresoTpomaNo ratings yet

- Arndt 2013Document18 pagesArndt 2013TpomaNo ratings yet

- The Abundance of Seafl Oor Massive Sulfi de DepositsDocument4 pagesThe Abundance of Seafl Oor Massive Sulfi de DepositsTpomaNo ratings yet

- Arndt 2013Document18 pagesArndt 2013TpomaNo ratings yet

- New Software For Faster and Better 3d Geological ModellingDocument9 pagesNew Software For Faster and Better 3d Geological Modellingbeku_ggs_bekuNo ratings yet

- Permian-Early Mesozoic Rifts in Peru and Bolivia, and Their Bearing On Andean-Age TectonicsDocument6 pagesPermian-Early Mesozoic Rifts in Peru and Bolivia, and Their Bearing On Andean-Age TectonicsTpomaNo ratings yet

- 10 1016@j Chemgeo 2016 10 032Document67 pages10 1016@j Chemgeo 2016 10 032TpomaNo ratings yet

- Hollister 1978Document10 pagesHollister 1978TpomaNo ratings yet

- Chapter 4 Perello Et AlDocument26 pagesChapter 4 Perello Et AlTpoma100% (1)

- BMG6a-G4W KrigeDocument24 pagesBMG6a-G4W KrigeTpomaNo ratings yet

- Chapter 4 Perello Et AlDocument26 pagesChapter 4 Perello Et AlTpoma100% (1)

- Rel Notes Update 2007Document35 pagesRel Notes Update 2007Julio SantosNo ratings yet

- Implicit Book - Digital.fv1Document57 pagesImplicit Book - Digital.fv1TpomaNo ratings yet

- Tinka Presentation 23 March 2017Document30 pagesTinka Presentation 23 March 2017TpomaNo ratings yet

- SCZn2 - G3-B4 Alter ENGL Short Lima2012rDocument20 pagesSCZn2 - G3-B4 Alter ENGL Short Lima2012rTpomaNo ratings yet

- SCZn2 - G3-B4 Alter ENGL Short Lima2012rDocument20 pagesSCZn2 - G3-B4 Alter ENGL Short Lima2012rTpomaNo ratings yet

- Skarn Short Course 1 IntroDocument12 pagesSkarn Short Course 1 IntroTpomaNo ratings yet

- Jurnal PajakDocument43 pagesJurnal PajakIndahNo ratings yet

- Financial Statement Analysis: Presenter's Name Presenter's Title DD Month YyyyDocument79 pagesFinancial Statement Analysis: Presenter's Name Presenter's Title DD Month Yyyyjohny BraveNo ratings yet

- Improving Social Cohesion in Ethiopia's Babile DistrictDocument9 pagesImproving Social Cohesion in Ethiopia's Babile DistrictsimbiroNo ratings yet

- BS Wira SartikaDocument1 pageBS Wira SartikaJGL MOTORNo ratings yet

- IPSFDocument7 pagesIPSFmanikandan BalasubramaniyanNo ratings yet

- National Shelter ProgramDocument43 pagesNational Shelter ProgramLara CayagoNo ratings yet

- SEC-MC No. 24 (s.2019)Document42 pagesSEC-MC No. 24 (s.2019)Zihr EllerycNo ratings yet

- Natco Medicine CompanyDocument12 pagesNatco Medicine CompanyPawan SoniNo ratings yet

- Recognizing and Measuring Government GrantsDocument12 pagesRecognizing and Measuring Government GrantsGraciasNo ratings yet

- Forex Indicators GuideDocument3 pagesForex Indicators Guideenghoss77No ratings yet

- ADM 3351-Final With SolutionsDocument14 pagesADM 3351-Final With SolutionsGraeme RalphNo ratings yet

- Contract of Lease With Option To PurchaseDocument3 pagesContract of Lease With Option To PurchaseNeilJuan JuanNo ratings yet

- Management of Banks and Financial Institutions Ass - 2Document5 pagesManagement of Banks and Financial Institutions Ass - 2Agnet TomyNo ratings yet

- NOCIL Investor PresentationDocument28 pagesNOCIL Investor PresentationSaurabh JainNo ratings yet

- MPC 2002 Financial ReportDocument25 pagesMPC 2002 Financial ReportMelbourne Press ClubNo ratings yet

- Inclusive Growth With Disruptive Innovations: Gearing Up For Digital DisruptionDocument48 pagesInclusive Growth With Disruptive Innovations: Gearing Up For Digital DisruptionShashank YadavNo ratings yet

- Eugene Fama ThesisDocument7 pagesEugene Fama Thesiskriscundiffevansville100% (1)

- Corporate Finace 1 PDFDocument4 pagesCorporate Finace 1 PDFwafflesNo ratings yet

- Loan Application FormDocument17 pagesLoan Application FormBodhiratan BartheNo ratings yet

- Comprehensive Accounting Case StudyDocument11 pagesComprehensive Accounting Case StudyMike StevenNo ratings yet

- Soal LatihanDocument1 pageSoal Latihanflypop13No ratings yet

- Unit 1 Portfolio Activity Review of Key Financial StatementsDocument4 pagesUnit 1 Portfolio Activity Review of Key Financial StatementsSimran PannuNo ratings yet

- 2024 Financial Report SanFranciscoDocument1 page2024 Financial Report SanFranciscoWiljohn ComendadorNo ratings yet

- LEI Bulk - 1000 ItemsDocument542 pagesLEI Bulk - 1000 ItemsVyacheslavNo ratings yet

- Dusty R BouthilletteDocument16 pagesDusty R Bouthillettedanw5646No ratings yet

- Iasb Employee BenDocument3 pagesIasb Employee BenRommel CruzNo ratings yet

- A Study On The Impact of Project Management Strategy On Real EstateDocument72 pagesA Study On The Impact of Project Management Strategy On Real EstateTasmay Enterprises100% (1)

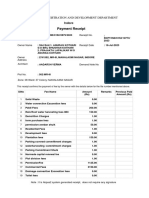

- Payment Receipt: Urban Administration and Development DepartmentDocument2 pagesPayment Receipt: Urban Administration and Development Departmentaadarsh vermaNo ratings yet

- Instructor's Manual Chapter 4 Time Value of MoneyDocument21 pagesInstructor's Manual Chapter 4 Time Value of MoneyReginoSaynoValenzuelaNo ratings yet

- CFP - SuggestedSolutions - RPEBDocument6 pagesCFP - SuggestedSolutions - RPEBSODDEYNo ratings yet

- Packing for Mars: The Curious Science of Life in the VoidFrom EverandPacking for Mars: The Curious Science of Life in the VoidRating: 4 out of 5 stars4/5 (1395)

- Sully: The Untold Story Behind the Miracle on the HudsonFrom EverandSully: The Untold Story Behind the Miracle on the HudsonRating: 4 out of 5 stars4/5 (103)

- Hero Found: The Greatest POW Escape of the Vietnam WarFrom EverandHero Found: The Greatest POW Escape of the Vietnam WarRating: 4 out of 5 stars4/5 (19)

- The Fabric of Civilization: How Textiles Made the WorldFrom EverandThe Fabric of Civilization: How Textiles Made the WorldRating: 4.5 out of 5 stars4.5/5 (57)

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4 out of 5 stars4/5 (1)

- The Beekeeper's Lament: How One Man and Half a Billion Honey Bees Help Feed AmericaFrom EverandThe Beekeeper's Lament: How One Man and Half a Billion Honey Bees Help Feed AmericaNo ratings yet

- The Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyFrom EverandThe Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyNo ratings yet

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationFrom EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationRating: 4.5 out of 5 stars4.5/5 (46)

- Faster: How a Jewish Driver, an American Heiress, and a Legendary Car Beat Hitler's BestFrom EverandFaster: How a Jewish Driver, an American Heiress, and a Legendary Car Beat Hitler's BestRating: 4 out of 5 stars4/5 (28)

- The Weather Machine: A Journey Inside the ForecastFrom EverandThe Weather Machine: A Journey Inside the ForecastRating: 3.5 out of 5 stars3.5/5 (31)

- Einstein's Fridge: How the Difference Between Hot and Cold Explains the UniverseFrom EverandEinstein's Fridge: How the Difference Between Hot and Cold Explains the UniverseRating: 4.5 out of 5 stars4.5/5 (50)

- The Quiet Zone: Unraveling the Mystery of a Town Suspended in SilenceFrom EverandThe Quiet Zone: Unraveling the Mystery of a Town Suspended in SilenceRating: 3.5 out of 5 stars3.5/5 (23)

- The End of Craving: Recovering the Lost Wisdom of Eating WellFrom EverandThe End of Craving: Recovering the Lost Wisdom of Eating WellRating: 4.5 out of 5 stars4.5/5 (80)

- 35 Miles From Shore: The Ditching and Rescue of ALM Flight 980From Everand35 Miles From Shore: The Ditching and Rescue of ALM Flight 980Rating: 4 out of 5 stars4/5 (21)

- Recording Unhinged: Creative and Unconventional Music Recording TechniquesFrom EverandRecording Unhinged: Creative and Unconventional Music Recording TechniquesNo ratings yet

- Pale Blue Dot: A Vision of the Human Future in SpaceFrom EverandPale Blue Dot: A Vision of the Human Future in SpaceRating: 4.5 out of 5 stars4.5/5 (586)

- The Path Between the Seas: The Creation of the Panama Canal, 1870-1914From EverandThe Path Between the Seas: The Creation of the Panama Canal, 1870-1914Rating: 4.5 out of 5 stars4.5/5 (124)

- A Place of My Own: The Architecture of DaydreamsFrom EverandA Place of My Own: The Architecture of DaydreamsRating: 4 out of 5 stars4/5 (241)

- Reality+: Virtual Worlds and the Problems of PhilosophyFrom EverandReality+: Virtual Worlds and the Problems of PhilosophyRating: 4 out of 5 stars4/5 (24)

- Data-ism: The Revolution Transforming Decision Making, Consumer Behavior, and Almost Everything ElseFrom EverandData-ism: The Revolution Transforming Decision Making, Consumer Behavior, and Almost Everything ElseRating: 3.5 out of 5 stars3.5/5 (12)

- The Future of Geography: How the Competition in Space Will Change Our WorldFrom EverandThe Future of Geography: How the Competition in Space Will Change Our WorldRating: 4.5 out of 5 stars4.5/5 (4)

- Permaculture for the Rest of Us: Abundant Living on Less than an AcreFrom EverandPermaculture for the Rest of Us: Abundant Living on Less than an AcreRating: 4.5 out of 5 stars4.5/5 (33)

- Dirt to Soil: One Family’s Journey into Regenerative AgricultureFrom EverandDirt to Soil: One Family’s Journey into Regenerative AgricultureRating: 5 out of 5 stars5/5 (125)