You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Case Forest City Tennis ClubDocument9 pagesCase Forest City Tennis ClubAhmedNiaz100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- IFFSSAFinal Report 2 May 22Document133 pagesIFFSSAFinal Report 2 May 22Tom CochranNo ratings yet

- Agreement Ngo Consultancy 1Document3 pagesAgreement Ngo Consultancy 1Devraj100% (4)

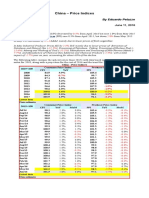

- China - Price IndicesDocument1 pageChina - Price IndicesEduardo PetazzeNo ratings yet

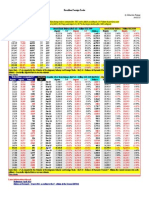

- WTI Spot PriceDocument4 pagesWTI Spot PriceEduardo Petazze100% (1)

- México, PBI 2015Document1 pageMéxico, PBI 2015Eduardo PetazzeNo ratings yet

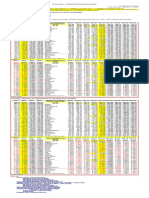

- Brazilian Foreign TradeDocument1 pageBrazilian Foreign TradeEduardo PetazzeNo ratings yet

- Retail Sales in The UKDocument1 pageRetail Sales in The UKEduardo PetazzeNo ratings yet

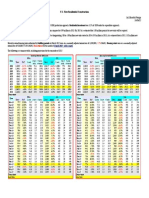

- U.S. New Residential ConstructionDocument1 pageU.S. New Residential ConstructionEduardo PetazzeNo ratings yet

- Euro Area - Industrial Production IndexDocument1 pageEuro Area - Industrial Production IndexEduardo PetazzeNo ratings yet

- Mas Review All ProblemsDocument12 pagesMas Review All ProblemsmeriiNo ratings yet

- gfps-datasheet-HDPE PIPE - Potable Water IndustryDIPS, DR11Black Pipe, Blue Stripe, 40' Long-360030007Document1 pagegfps-datasheet-HDPE PIPE - Potable Water IndustryDIPS, DR11Black Pipe, Blue Stripe, 40' Long-360030007Nam PhanNo ratings yet

- Special Issue On Economy & Sustainable Development in UzbekistanDocument112 pagesSpecial Issue On Economy & Sustainable Development in UzbekistanMalcolm ChristopherNo ratings yet

- Chapter-Viii 8.1. Housing & Urban Development Corporation (HUDCO) Limited Urban DevelopmentDocument13 pagesChapter-Viii 8.1. Housing & Urban Development Corporation (HUDCO) Limited Urban DevelopmentJayjeet BhattacharjeeNo ratings yet

- Catalogue of Fifth 00 GlenDocument66 pagesCatalogue of Fifth 00 GlenShubho BoseNo ratings yet

- EPA Standards IEMS ISO 14000 PDFDocument7 pagesEPA Standards IEMS ISO 14000 PDFateliervitaliNo ratings yet

- SIMULUS 8 Offline RegistrationDocument8 pagesSIMULUS 8 Offline RegistrationNeutral Body NursingNo ratings yet

- (English-French) Degrowth, Explained (DownSub - Com)Document11 pages(English-French) Degrowth, Explained (DownSub - Com)MOHAMED EL BARAKANo ratings yet

- LettersDocument126 pagesLettersnadeemtyagiNo ratings yet

- E Book RoyaltiesDocument6 pagesE Book Royaltiesclwaei5525No ratings yet

- Success: Equipment: Container - 40' HC # 1Document2 pagesSuccess: Equipment: Container - 40' HC # 1Fitri FitrianahNo ratings yet

- Chapter 7 - Teacher's Manual - Ifa Part 1aDocument7 pagesChapter 7 - Teacher's Manual - Ifa Part 1aCharmae Agan CaroroNo ratings yet

- Overview of The District KachhiDocument4 pagesOverview of The District Kachhisyed waqas RehmanNo ratings yet

- Bimstec: Download FromDocument4 pagesBimstec: Download FromTarun Kumar MahorNo ratings yet

- Magnakabel NusantaraDocument13 pagesMagnakabel Nusantaratees220510No ratings yet

- Maltusian Theory of PopulationDocument2 pagesMaltusian Theory of PopulationBirkheyNo ratings yet

- Advocate Set Out 2015Document51 pagesAdvocate Set Out 2015duomareNo ratings yet

- MedicalDocument2 pagesMedicalDVET IndiaNo ratings yet

- SUMI YASHSHREE HOTELS RESORTS PRIVATE LIMITED Purchase 79Document2 pagesSUMI YASHSHREE HOTELS RESORTS PRIVATE LIMITED Purchase 79biswa chakrabortyNo ratings yet

- Prof Ram Meghe College OF Engineering & Management, BadneraDocument4 pagesProf Ram Meghe College OF Engineering & Management, BadneraVaibhav MandhareNo ratings yet

- MM 1 - Students Book Unit 8 AnswersDocument3 pagesMM 1 - Students Book Unit 8 AnswerssantiagoalejandrotrujilloortiNo ratings yet

- Assignment Mat097Document25 pagesAssignment Mat097Nur AdeelaNo ratings yet

- Siemens AR 2006 1427558 2Document147 pagesSiemens AR 2006 1427558 2shashi_k07No ratings yet

- Air Canada Vs CirDocument59 pagesAir Canada Vs CirKrizia FabicoNo ratings yet

- 4 RatioDocument50 pages4 RatioSandeep SharmaNo ratings yet

- POLICY BRIEF CPEC Dividends For Balochistan A Critical AnalysisDocument7 pagesPOLICY BRIEF CPEC Dividends For Balochistan A Critical AnalysisAyesha BukhariNo ratings yet

- 470 Capsim NotesDocument2 pages470 Capsim NoteschomkaNo ratings yet