You might also like

- United States Census Figures Back to 1630From EverandUnited States Census Figures Back to 1630No ratings yet

- Examen 1 InfoDocument8 pagesExamen 1 InfoOrlando JohhNo ratings yet

- Midterm1 DataDocument4 pagesMidterm1 DataiceNo ratings yet

- Chapter 17Document23 pagesChapter 17Bhavya SarawgiNo ratings yet

- BP Energy Outlook 2020 Chart Data PackDocument200 pagesBP Energy Outlook 2020 Chart Data PackrubenpeNo ratings yet

- Irrational ExuberanceDocument52 pagesIrrational ExuberancetrendscatcherNo ratings yet

- Lessons From Capital Market History: Return & RiskDocument46 pagesLessons From Capital Market History: Return & RiskBlue DemonNo ratings yet

- Pbi Peru 1970-2014Document5 pagesPbi Peru 1970-2014Dennis Vasquez MarinNo ratings yet

- Moneda SDocument6 pagesMoneda Ssantiago guaymasNo ratings yet

- NPV Graph and SpreadsheetsDocument3 pagesNPV Graph and SpreadsheetsSrinivas Meduri100% (1)

- Top Federal Tax Rates Since 1916Document1 pageTop Federal Tax Rates Since 1916Ephraim DavisNo ratings yet

- Personal Finance Webinar Presentation 11/12/2012 Streettalk AdvsiorsDocument19 pagesPersonal Finance Webinar Presentation 11/12/2012 Streettalk Advsiorsstreettalk700No ratings yet

- Altura Exposicion: Tabla 16-G Coeficiente CeDocument9 pagesAltura Exposicion: Tabla 16-G Coeficiente CeKatty LapoNo ratings yet

- Global Economics Assignment: Submitted By:-Mansi Mittal (82) Submitted To: - Prof. Moon Moon HaqueDocument14 pagesGlobal Economics Assignment: Submitted By:-Mansi Mittal (82) Submitted To: - Prof. Moon Moon HaqueMansi MittalNo ratings yet

- North South University: Economic Conditions of Bangladesh During 1972-2019Document16 pagesNorth South University: Economic Conditions of Bangladesh During 1972-2019Shoaib AhmedNo ratings yet

- Annual Subscription 1894 - 2008Document6 pagesAnnual Subscription 1894 - 2008ipatersoNo ratings yet

- Fed Top Tax Rate HistoryDocument1 pageFed Top Tax Rate HistoryJohn StantonNo ratings yet

- Libro 1Document18 pagesLibro 1julian_Hm9830No ratings yet

- Ibm: PBV and RoeDocument3 pagesIbm: PBV and Roeminhthuc203No ratings yet

- Aus Single Family ResidencesDocument1 pageAus Single Family ResidencesMichael KozlowskiNo ratings yet

- Indicator2 2006 1Document3 pagesIndicator2 2006 1aisha00052693No ratings yet

- Educa Contador (1) (1) - 1-4Document4 pagesEduca Contador (1) (1) - 1-4Fonezinho TopNo ratings yet

- El SalvadorDocument3 pagesEl SalvadorJOSIAS NAHUM MADUEÑO CANCHARINo ratings yet

- El SalvadorDocument3 pagesEl SalvadorJOSIAS NAHUM MADUEÑO CANCHARINo ratings yet

- ChileDocument3 pagesChileJOSIAS NAHUM MADUEÑO CANCHARINo ratings yet

- ChileDocument3 pagesChileJOSIAS NAHUM MADUEÑO CANCHARINo ratings yet

- Trend LineDocument6 pagesTrend Linejahir golandajNo ratings yet

- Poblacion FuturaDocument2 pagesPoblacion FuturaLisbeth YagualNo ratings yet

- Vaymuanha 3.3ty Vay70% 7.2% 5namDocument2 pagesVaymuanha 3.3ty Vay70% 7.2% 5namTào Thanh TìnhNo ratings yet

- Palet: Color 1 Color 2 Color 3 Color 4 Color 5Document4 pagesPalet: Color 1 Color 2 Color 3 Color 4 Color 5marlis amadorNo ratings yet

- Ie DataDocument111 pagesIe Datapraneet singhNo ratings yet

- 09 - Homework3 Punto 1Document45 pages09 - Homework3 Punto 1Deisy Paola Suarez LopezNo ratings yet

- Break Even Analysis: Units Price Total Revenue Fixed Cost Variable Cost Total Cost Net Profit/ (Loss)Document6 pagesBreak Even Analysis: Units Price Total Revenue Fixed Cost Variable Cost Total Cost Net Profit/ (Loss)Waqas MohiuddinNo ratings yet

- PASIG REVENUE CODE of 1992 As Amended (LBT of Dealers, Contractors and Services)Document4 pagesPASIG REVENUE CODE of 1992 As Amended (LBT of Dealers, Contractors and Services)Bobby Olavides Sebastian33% (3)

- 2012 LAPC Facebook Fan TournamentDocument2 pages2012 LAPC Facebook Fan TournamentCommerce CasinoNo ratings yet

- Report Retrieve ControllerDocument13 pagesReport Retrieve ControllerPetra FaheyNo ratings yet

- AMF Bowling Ball - SSCDocument3 pagesAMF Bowling Ball - SSCAbubakar ShafiNo ratings yet

- Concrete Column PMM EnvelopeDocument12 pagesConcrete Column PMM EnvelopeAngel CMNo ratings yet

- To MiDocument5 pagesTo MiBustomi TomiNo ratings yet

- REPORT #GOLDHUNTDocument80 pagesREPORT #GOLDHUNTMuzlim Skuzu IcHigoNo ratings yet

- Salario Minimo Ministerio de Proteccion SocialDocument1 pageSalario Minimo Ministerio de Proteccion SocialJairo Roman ZapataNo ratings yet

- Clothing Retailers Financial Statements AnalysisDocument15 pagesClothing Retailers Financial Statements Analysisapi-277769092No ratings yet

- Master Coin CodesDocument19 pagesMaster Coin CodesPavlo PietrovichNo ratings yet

- Event Log 7-8-2022 11-24Document147 pagesEvent Log 7-8-2022 11-24Russel Vela BezaresNo ratings yet

- MacroDocument10 pagesMacrothareendaNo ratings yet

- US Oil Consumption and ProductionDocument2 pagesUS Oil Consumption and ProductionOmkar ChogaleNo ratings yet

- Color 1 Color 2 Color 3 Color 4 Color 5Document8 pagesColor 1 Color 2 Color 3 Color 4 Color 5Igreja De Deus No Brasil Lago VerdeNo ratings yet

- Ie DataDocument73 pagesIe Datamkkaran90No ratings yet

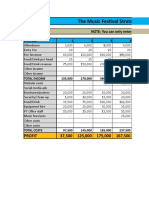

- The Music Festival Strategy Formulation Exercise: Profit 37,500 125,000 175,000 167,500Document5 pagesThe Music Festival Strategy Formulation Exercise: Profit 37,500 125,000 175,000 167,500Sarbartha RayNo ratings yet

- TELEFONOS: 02856340332 / 0424 9075655 Abogados Especialistas en Derecho LaboralDocument9 pagesTELEFONOS: 02856340332 / 0424 9075655 Abogados Especialistas en Derecho LaboralVirginia MejiaNo ratings yet

- Mariterm Cjenik Ozujak 2011Document48 pagesMariterm Cjenik Ozujak 2011dino_pNo ratings yet

- Taxation Trends in The European Union - 2011 - Booklet 34Document1 pageTaxation Trends in The European Union - 2011 - Booklet 34Dimitris ArgyriouNo ratings yet

- 3B. Lampiran PP No 82 THN 2001Document188 pages3B. Lampiran PP No 82 THN 2001Hilih KintilNo ratings yet

- Dharam Shewa Lottery 3 Option 55Document2 pagesDharam Shewa Lottery 3 Option 55Cric FreakNo ratings yet

- Uriol Vásquez MaricieloDocument6 pagesUriol Vásquez MaricieloBalto VelasquezNo ratings yet

- Exhibit 1 Profitability and Financial PositionDocument14 pagesExhibit 1 Profitability and Financial PositionMadhavi gNo ratings yet

- TMo2Go Bonus Minutes SpreadsheetDocument40 pagesTMo2Go Bonus Minutes SpreadsheetMattJhsnNo ratings yet

- Feb PWT Export 2202024Document30 pagesFeb PWT Export 2202024El rincón de las 5 EL RINCÓN DE LAS 5No ratings yet

- Debt Policy at UST Inc.Document47 pagesDebt Policy at UST Inc.karthikk1990100% (2)

- Fp-11 To 15 1st Podium LevelDocument5 pagesFp-11 To 15 1st Podium LevelKristina OrmacidoNo ratings yet

- Group Vocabulary ListDocument26 pagesGroup Vocabulary Listmussawer788No ratings yet

- Principles of Management MCQS With Answers of Stephen PDocument21 pagesPrinciples of Management MCQS With Answers of Stephen Psridharpalleda73% (73)

- Fin623 Solved MCQs For EamsDocument24 pagesFin623 Solved MCQs For EamsSohail Merchant79% (14)

- KPKPSC Experience FORMDocument1 pageKPKPSC Experience FORMShahkhan SuraniNo ratings yet

- Unit 5 Module - 8: Budgets & Budgetary Control Multiple Choice QuestionsDocument7 pagesUnit 5 Module - 8: Budgets & Budgetary Control Multiple Choice QuestionsShahkhan SuraniNo ratings yet

- Age RelaxationDocument2 pagesAge RelaxationAkhtar Hussain100% (1)

- Principles of Management MCQS With Answers of Stephen PDocument21 pagesPrinciples of Management MCQS With Answers of Stephen Psridharpalleda73% (73)

- Age RelaxationDocument2 pagesAge RelaxationAkhtar Hussain100% (1)

- Office of The Hospital Director Medical Teaching Institution BannuDocument1 pageOffice of The Hospital Director Medical Teaching Institution BannuShahkhan SuraniNo ratings yet

- Fin623 Solved MCQs For EamsDocument24 pagesFin623 Solved MCQs For EamsSohail Merchant79% (14)

- F.4 14 2019 R 01 07 2019 DRDocument1 pageF.4 14 2019 R 01 07 2019 DRIrfan Khan DanishNo ratings yet

- 100 Accounting Questions With AnswersDocument21 pages100 Accounting Questions With Answersanon_675918451No ratings yet

- Advertisement No 05 2018Document15 pagesAdvertisement No 05 2018ibrahim khanNo ratings yet

- Economics Mcqs Test From Past Public Service Commission ExamsDocument43 pagesEconomics Mcqs Test From Past Public Service Commission Examslog man89% (9)

- Ms Word MCQ Bank PDFDocument19 pagesMs Word MCQ Bank PDFMuhammad AkramNo ratings yet

- Used Under Licence by Documatica Legal Forms IncDocument1 pageUsed Under Licence by Documatica Legal Forms IncShahkhan SuraniNo ratings yet

- Age RelaxationDocument6 pagesAge RelaxationShahkhan SuraniNo ratings yet

- Principles of Management MCQS With Answers of Stephen PDocument21 pagesPrinciples of Management MCQS With Answers of Stephen Psridharpalleda73% (73)

- Interview Program SEPTEMBER 2019Document2 pagesInterview Program SEPTEMBER 2019Khalil RehmanNo ratings yet

- Critical Audit Matters: JULY 2018Document12 pagesCritical Audit Matters: JULY 2018Ahme MweweNo ratings yet

- General Accounting TermsDocument7 pagesGeneral Accounting TermsShahkhan SuraniNo ratings yet

- Sr. No. Core Areas PercentageDocument7 pagesSr. No. Core Areas PercentageRaja AhsanNo ratings yet

- Administrative Clerk JD - PDDocument6 pagesAdministrative Clerk JD - PDThinagaran GunasegaranNo ratings yet

- Anti Narcotics Force Act 1997Document7 pagesAnti Narcotics Force Act 1997Shahkhan SuraniNo ratings yet

- Power and Organizational PoliticsDocument16 pagesPower and Organizational Politicsashish21847960No ratings yet

- Shakirullah ApplictionDocument1 pageShakirullah ApplictionShahkhan SuraniNo ratings yet

- TOENEC Manpower Report (JTI) 2020Document8 pagesTOENEC Manpower Report (JTI) 2020mark lester caluzaNo ratings yet

- Lecture Notes - ECON 22358G - Chapter 13-No AnswersDocument43 pagesLecture Notes - ECON 22358G - Chapter 13-No AnswersManal AliNo ratings yet

- Functions of Central BankDocument12 pagesFunctions of Central BankSAMOIERNo ratings yet

- Bertocco and Kalajzić (2019) - On The Monetary Nature of The Interest Rate in A Keynes-Schumpeter PerspectiveDocument28 pagesBertocco and Kalajzić (2019) - On The Monetary Nature of The Interest Rate in A Keynes-Schumpeter PerspectivePepeNo ratings yet

- FIN201 Essay Test FA 2022 Nguyễn Đức Minh HS173138Document3 pagesFIN201 Essay Test FA 2022 Nguyễn Đức Minh HS173138Nguyễn Đức MinhNo ratings yet

- Abstract Temporality & Marx's Critique of Political EconomyDocument52 pagesAbstract Temporality & Marx's Critique of Political EconomyTom Allen100% (1)

- Capitalism, Socialism, and DemocracyDocument36 pagesCapitalism, Socialism, and DemocracyKavita SharmaNo ratings yet

- Mishkin Han27NewDocument21 pagesMishkin Han27NewSubhajyoti DasNo ratings yet

- Ao CodeDocument116 pagesAo Codex2ezzyorNo ratings yet

- InflationDocument40 pagesInflationRosebell MelgarNo ratings yet

- 533Document30 pages533fadoNo ratings yet

- THE CIRCULAR FLOW OF ECONOMIC ACTIVITY - Study MaterialDocument2 pagesTHE CIRCULAR FLOW OF ECONOMIC ACTIVITY - Study MaterialEllen RoaNo ratings yet

- Receipt Process Comparison (Baan Vs Oracle)Document7 pagesReceipt Process Comparison (Baan Vs Oracle)mapati66No ratings yet

- Course Outline-SpringDocument4 pagesCourse Outline-SpringAllauddinaghaNo ratings yet

- PAS 29 - Financial Reporting in Hyperinflationary EconomiesDocument7 pagesPAS 29 - Financial Reporting in Hyperinflationary EconomiesKrizzia DizonNo ratings yet

- Principal and InterestDocument23 pagesPrincipal and InterestSpam KingNo ratings yet

- The Globalization of World Economics-1Document25 pagesThe Globalization of World Economics-1JASPER ALCANTARANo ratings yet

- TRW QuessdgDocument2 pagesTRW QuessdgShreyansh TripathiNo ratings yet

- Mathematics-of-Investment-midterm LessonsDocument50 pagesMathematics-of-Investment-midterm LessonsJohn Luis Masangkay BantolinoNo ratings yet

- Comaker Policy PDFDocument10 pagesComaker Policy PDFAko C IanNo ratings yet

- Central Bank Ratings A New Methodology For Global Excellence 2Nd Edition Indranarain Ramlall Full ChapterDocument67 pagesCentral Bank Ratings A New Methodology For Global Excellence 2Nd Edition Indranarain Ramlall Full Chapterjuanita.byers160100% (4)

- Macroeconomics 6th Edition Blanchard Test BankDocument10 pagesMacroeconomics 6th Edition Blanchard Test Bankroryhungzad6100% (29)

- Chapter 10 Lecture PresentationDocument51 pagesChapter 10 Lecture PresentationDina SamirNo ratings yet

- Monetary Policy and Inflation in Zambia: JEL Classification: C50, E52 Cointegrated Vector Autoregressive Model, VECXDocument37 pagesMonetary Policy and Inflation in Zambia: JEL Classification: C50, E52 Cointegrated Vector Autoregressive Model, VECXWilliam FedoungNo ratings yet

- PDFDocument1 pagePDFPradeep SinglaNo ratings yet

- Karl Marx's Wage Labor and Capital' - by The Dangerous Maybe - MediumDocument10 pagesKarl Marx's Wage Labor and Capital' - by The Dangerous Maybe - MediumGabriel DavidsonNo ratings yet

- AS - Lecture 17, 18Document25 pagesAS - Lecture 17, 18shubham solankiNo ratings yet

- Foreign Exchange RateDocument20 pagesForeign Exchange RatePrabhneet100% (1)

- Essay On The Statement by The Special Rapporteur On The Right To Adequate HousingDocument2 pagesEssay On The Statement by The Special Rapporteur On The Right To Adequate HousingTharosAbelNo ratings yet

- 2 - Tutorial 6 - SolutionDocument3 pages2 - Tutorial 6 - SolutionLuanNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionFrom EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionRating: 5 out of 5 stars5/5 (27)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo ratings yet

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet

- Beat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012From EverandBeat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012No ratings yet

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- Bookkeeping for Small Business: The Most Complete and Updated Guide with Tips and Tricks to Track Income & Expenses and Prepare for TaxesFrom EverandBookkeeping for Small Business: The Most Complete and Updated Guide with Tips and Tricks to Track Income & Expenses and Prepare for TaxesNo ratings yet

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Taxes Have Consequences: An Income Tax History of the United StatesFrom EverandTaxes Have Consequences: An Income Tax History of the United StatesNo ratings yet

- Make Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionFrom EverandMake Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionNo ratings yet

- Decrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationFrom EverandDecrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationNo ratings yet

- U.S. Taxes for Worldly Americans: The Traveling Expat's Guide to Living, Working, and Staying Tax Compliant AbroadFrom EverandU.S. Taxes for Worldly Americans: The Traveling Expat's Guide to Living, Working, and Staying Tax Compliant AbroadNo ratings yet

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsFrom EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsRating: 3.5 out of 5 stars3.5/5 (9)