You might also like

- Gyaan Kosh Term 3 Corporate Finance SummaryDocument10 pagesGyaan Kosh Term 3 Corporate Finance SummaryAnuj AgarwalNo ratings yet

- Fair Value GIDocument45 pagesFair Value GIscamardela79No ratings yet

- Capital StructureDocument28 pagesCapital Structureluvnica6348No ratings yet

- Dwnload Full Foundations of Financial Management Canadian 9th Edition Hirt Solutions Manual PDFDocument36 pagesDwnload Full Foundations of Financial Management Canadian 9th Edition Hirt Solutions Manual PDFhenrykr7men100% (11)

- Our ProjectDocument7 pagesOur ProjectYoussef samirNo ratings yet

- Sample of Asset-Office Land, Equiptment, Cash, MachinesDocument29 pagesSample of Asset-Office Land, Equiptment, Cash, MachinesMaria Cludet NayveNo ratings yet

- Subject Code-B-103 Section A: Part One:: A. Ignored Non-Corporate EnterpriseDocument8 pagesSubject Code-B-103 Section A: Part One:: A. Ignored Non-Corporate EnterpriseRamusubu PsrkNo ratings yet

- Fabrozzi 3Document39 pagesFabrozzi 3leena JohnsonNo ratings yet

- Karen Patterson - Self AssessmentDocument2 pagesKaren Patterson - Self AssessmentpreciousNo ratings yet

- Notes On Weighted-Average Cost of Capital (WACC) : Finance 422Document5 pagesNotes On Weighted-Average Cost of Capital (WACC) : Finance 422Dan MaloneyNo ratings yet

- Understanding the True Cost of Issuing Convertible DebtDocument5 pagesUnderstanding the True Cost of Issuing Convertible Debt_lucky_No ratings yet

- Introduction of Cost of CapitalDocument6 pagesIntroduction of Cost of CapitalKamalesh MahapatraNo ratings yet

- SSRN Id424903Document51 pagesSSRN Id424903Urmi MukherjeeNo ratings yet

- The Cost of Capital: OutlineDocument10 pagesThe Cost of Capital: OutlineNikhil GandhiNo ratings yet

- Treatment of Securitized Transactions in Bankruptcy: April 2001Document6 pagesTreatment of Securitized Transactions in Bankruptcy: April 2001Harpott GhantaNo ratings yet

- Optimal Capital Structure by Adam HayesDocument2 pagesOptimal Capital Structure by Adam HayesMaham MujeebNo ratings yet

- SFM Case4 Group7Document5 pagesSFM Case4 Group7AMAAN LULANIA 22100% (1)

- 1.consolidation Loan: 2.grievance ProcedureDocument10 pages1.consolidation Loan: 2.grievance ProcedureShradha JainNo ratings yet

- 30 March Assignment 1500 WordsDocument5 pages30 March Assignment 1500 Wordsmishal chNo ratings yet

- Battle of The Exes: Understanding The Effect of The Ex Ante and Ex Post Approaches On Damage CalculationsDocument3 pagesBattle of The Exes: Understanding The Effect of The Ex Ante and Ex Post Approaches On Damage CalculationsVeris Consulting, Inc.No ratings yet

- APC 403 PFRS For SEs (Section 1-2)Document3 pagesAPC 403 PFRS For SEs (Section 1-2)AnnSareineMamadesNo ratings yet

- Managerial Finance: Leverage Determinants in Saudi ArabiaDocument29 pagesManagerial Finance: Leverage Determinants in Saudi ArabiaMahmood KhanNo ratings yet

- 13 Impairment of AssetsDocument44 pages13 Impairment of Assetsfordan Zodorovic56% (9)

- Current Liabilities - ProvisionsDocument9 pagesCurrent Liabilities - ProvisionsJerome_JadeNo ratings yet

- Financial Management 2Document75 pagesFinancial Management 2Ali ShehbazNo ratings yet

- Finance Assignment' 1Document13 pagesFinance Assignment' 1Daichi FaithNo ratings yet

- (C) There Is Certainly A Relationship Between The Weighted AverageDocument9 pages(C) There Is Certainly A Relationship Between The Weighted AverageikrooNo ratings yet

- Fainancial Management AssignmentDocument13 pagesFainancial Management AssignmentSamuel AbebawNo ratings yet

- Capital Structure Theories ExplainedDocument10 pagesCapital Structure Theories ExplainedMd. Nazmul Kabir100% (1)

- Timothy - Chap 9Document33 pagesTimothy - Chap 9Chaeyeon Jung0% (1)

- Cost of Capital and Its Implications for Valuation and Strategic DecisionsDocument6 pagesCost of Capital and Its Implications for Valuation and Strategic DecisionsBaskar SelvanNo ratings yet

- 12 Theories of FinanceDocument15 pages12 Theories of Financehira malikNo ratings yet

- Corporate Finance - Cash Insolvency AnalysisDocument9 pagesCorporate Finance - Cash Insolvency Analysisuser 02No ratings yet

- MNGT 422Document8 pagesMNGT 422Kristofer John RufoNo ratings yet

- Critique Paper On Impairment of AssetsDocument8 pagesCritique Paper On Impairment of AssetsJoshtanco17No ratings yet

- PRACTICAL ACCOUNTING 1 RECEIVABLESDocument3 pagesPRACTICAL ACCOUNTING 1 RECEIVABLESChinchin Ilagan DatayloNo ratings yet

- How Do You Value A Company?Document3 pagesHow Do You Value A Company?Sumit DaniNo ratings yet

- Bài tập chương 1+2 KTQTDocument9 pagesBài tập chương 1+2 KTQTTrần Thanh SơnNo ratings yet

- Case Study #6 WorldCom, Inc. - Capitalized Costs and Earnings Quality 50 AbstractDocument2 pagesCase Study #6 WorldCom, Inc. - Capitalized Costs and Earnings Quality 50 AbstractAnisa KodraNo ratings yet

- AlibertiDocument29 pagesAlibertibiblioteca economicaNo ratings yet

- Maurece Schiller - StubsDocument15 pagesMaurece Schiller - StubsMihir ShahNo ratings yet

- The CostDocument25 pagesThe CostRomeo Torreta JrNo ratings yet

- Damodaran - Financial Services ValuationDocument7 pagesDamodaran - Financial Services ValuationBogdan TudoseNo ratings yet

- Capital Structure: Features of Optimal Capital StructureDocument7 pagesCapital Structure: Features of Optimal Capital StructureSana MahmoodNo ratings yet

- Financial Theory and Corporate Policy - Copeland.449-493Document45 pagesFinancial Theory and Corporate Policy - Copeland.449-493Claire Marie ThomasNo ratings yet

- What Is A Financial InstrumentDocument9 pagesWhat Is A Financial InstrumentSimon ChawingaNo ratings yet

- Factoring in Finance ArrangementsDocument9 pagesFactoring in Finance Arrangementsduncanmac200777No ratings yet

- Week 7: Corporate Credit Risk Models Based On Stock PriceDocument19 pagesWeek 7: Corporate Credit Risk Models Based On Stock PriceNhat Khanh NguyenNo ratings yet

- FM - Chapter 15Document8 pagesFM - Chapter 15Rahul ShrivastavaNo ratings yet

- Cost of Capital PDFDocument11 pagesCost of Capital PDFLa Sensaciion Del DiiazNo ratings yet

- Enron and Internationally Agreed Principles: A Case Study in Ethics PDFDocument4 pagesEnron and Internationally Agreed Principles: A Case Study in Ethics PDFSuren TheannilawuNo ratings yet

- Ifrs For SMEsDocument104 pagesIfrs For SMEsApril AcboNo ratings yet

- The Cost of Capital: OutlineDocument11 pagesThe Cost of Capital: OutlineVelmuruganKNo ratings yet

- Q1) What Is Cost of Capital? How Is It Calculated For Different Sources of Capital? How Is Average Weighted Cost of Capital Measured?Document18 pagesQ1) What Is Cost of Capital? How Is It Calculated For Different Sources of Capital? How Is Average Weighted Cost of Capital Measured?udayvadapalliNo ratings yet

- The Cost of Capital: Learning ObjectivesDocument24 pagesThe Cost of Capital: Learning ObjectivesMarshallBruce123No ratings yet

- APC 403 PFRS For SMEsDocument10 pagesAPC 403 PFRS For SMEsHazel Seguerra BicadaNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- MODULE_5_-_Issues_in_Valuing_Financial_Service_FirmsDocument3 pagesMODULE_5_-_Issues_in_Valuing_Financial_Service_Firmschristian garciaNo ratings yet

- National Immunization Management System: Tracking ID: 100001468Document1 pageNational Immunization Management System: Tracking ID: 100001468aaaaaaaliNo ratings yet

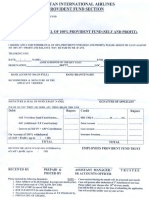

- Self Povident FundDocument1 pageSelf Povident FundMoin Max ReevesNo ratings yet

- National Immunization Management System: Tracking ID: 100001468Document1 pageNational Immunization Management System: Tracking ID: 100001468aaaaaaaliNo ratings yet

- Business Research Method: Group No. 4 Members Names and Roll NumbersDocument3 pagesBusiness Research Method: Group No. 4 Members Names and Roll NumbersMoin Max ReevesNo ratings yet

- BM Man Hour Plan 2019Document31 pagesBM Man Hour Plan 2019Moin Max ReevesNo ratings yet

- What Is NoiseDocument9 pagesWhat Is NoiseMoin Max ReevesNo ratings yet

- QuestionnaireDocument2 pagesQuestionnaireMoin Max ReevesNo ratings yet

- Activities of Pert CPM of DawlanceDocument1 pageActivities of Pert CPM of DawlanceMoin Max ReevesNo ratings yet

- University Of Karachi Entrepreneurship Group Attendance SheetDocument4 pagesUniversity Of Karachi Entrepreneurship Group Attendance SheetMoin Max ReevesNo ratings yet

- Research ReportDocument7 pagesResearch ReportMoin Max ReevesNo ratings yet

- Queuing Model For Bank Al Habib:: Bservation IscussionDocument2 pagesQueuing Model For Bank Al Habib:: Bservation IscussionMoin Max ReevesNo ratings yet

- Higher Algebra - Hall & KnightDocument593 pagesHigher Algebra - Hall & KnightRam Gollamudi100% (2)

- Basic Accounting Concepts: The Income Statement: Mcgraw-Hill/IrwinDocument38 pagesBasic Accounting Concepts: The Income Statement: Mcgraw-Hill/IrwinVanessa CarltonNo ratings yet

- Atm QueuDocument5 pagesAtm QueuMoin Max ReevesNo ratings yet

- Financial Statement AnalysisDocument27 pagesFinancial Statement AnalysisFarhad Hussain100% (1)

- Meeting ChecklistDocument11 pagesMeeting ChecklistYogesh ChhaprooNo ratings yet

- Parntership HandoutDocument12 pagesParntership HandoutMaria Angela GasparNo ratings yet

- Registration of CooperativesDocument5 pagesRegistration of CooperativesRheneir Mora100% (1)

- Walmart StrategyDocument14 pagesWalmart Strategyclassmate100% (4)

- Dwayne Bohac ContributionsDocument318 pagesDwayne Bohac ContributionsReform AustinNo ratings yet

- TDS Certificate SummaryDocument2 pagesTDS Certificate SummaryAkriti JhaNo ratings yet

- 1153 b8fbDocument3 pages1153 b8fbLakshay DhamijaNo ratings yet

- Ch3 - Small Business and Corporate Enterpreneurship PDFDocument67 pagesCh3 - Small Business and Corporate Enterpreneurship PDFdanial001100% (1)

- Developing An Effective Business ModelDocument24 pagesDeveloping An Effective Business Modeldedila nachar100% (1)

- Kredx Documentation List UpdatedDocument4 pagesKredx Documentation List UpdatedSwapnil CallaNo ratings yet

- Abdm3233 International Business PlanningDocument4 pagesAbdm3233 International Business PlanningpreetimutiarayNo ratings yet

- Lessons From The Enron ScandalDocument3 pagesLessons From The Enron ScandalCharise CayabyabNo ratings yet

- Employee Details Payment & Leave Details: Arrears Current AmountDocument1 pageEmployee Details Payment & Leave Details: Arrears Current AmountswapnilNo ratings yet

- Board Resolution For BIR SampleDocument2 pagesBoard Resolution For BIR SampleRonnieGarrido75% (4)

- Grofin BrochureDocument5 pagesGrofin Brochurerainmaker1978No ratings yet

- 1988 BAR EXAMINATION QUESTIONSDocument15 pages1988 BAR EXAMINATION QUESTIONSjerushabrainerdNo ratings yet

- Chapter 3 Inclusions in The Gross Income PDFDocument11 pagesChapter 3 Inclusions in The Gross Income PDFkimberly tenebro100% (1)

- Corporation AccountingDocument70 pagesCorporation AccountingMae Abigail Banquil100% (1)

- Sales Management Meeting - May 24-25 2016Document229 pagesSales Management Meeting - May 24-25 2016Emilian NeculaNo ratings yet

- Case: Diebold: Through Acquisitions Joint Ventures JDocument38 pagesCase: Diebold: Through Acquisitions Joint Ventures JsomnathmangarajNo ratings yet

- Cpa A1.2 - Audit Practice & Assurance Services - Study ManualDocument236 pagesCpa A1.2 - Audit Practice & Assurance Services - Study ManualJoan Marie AgnesNo ratings yet

- PNB vs. Andrada Electric & Engineering CoDocument6 pagesPNB vs. Andrada Electric & Engineering CoKennethQueRaymundoNo ratings yet

- Product Catalogue ERTG-LresDocument12 pagesProduct Catalogue ERTG-LrescocoricorNo ratings yet

- Philippines: Guide To Doing BusinessDocument30 pagesPhilippines: Guide To Doing BusinessTina Reyes-BattadNo ratings yet

- Ifric 23Document4 pagesIfric 23Leenin DominguezNo ratings yet

- Sabmiller's Case StudyDocument35 pagesSabmiller's Case Studyinspi_p9532100% (4)

- McDonald's Case Study - MBA MarketingDocument5 pagesMcDonald's Case Study - MBA MarketingRanjan Kumar Yadav100% (1)

- MFI - Cooperative BankDocument22 pagesMFI - Cooperative BankkamalgandhiNo ratings yet

- ACC 401week 8 QuizDocument17 pagesACC 401week 8 QuizEMLNo ratings yet

- Ethical Issues in Business SettingsDocument2 pagesEthical Issues in Business SettingsFeras MehmoodNo ratings yet