You might also like

- Honda Civic Insurance (20-21) PDFDocument10 pagesHonda Civic Insurance (20-21) PDFGuru CharanNo ratings yet

- To, Mrs Padmapriya R No 2/7 Akshya Plot G1 Bharathidasan Street Nillamaggai Nagar Adambakkam 600088 Kanchipuram TAMILNADU 600088 Mobile:9840584756Document4 pagesTo, Mrs Padmapriya R No 2/7 Akshya Plot G1 Bharathidasan Street Nillamaggai Nagar Adambakkam 600088 Kanchipuram TAMILNADU 600088 Mobile:9840584756shidoNo ratings yet

- The Oriental Insurance Company LimitedDocument3 pagesThe Oriental Insurance Company LimitedDibya DillipNo ratings yet

- Bajaj Allianz Private Car Policy SummaryDocument10 pagesBajaj Allianz Private Car Policy SummaryAairyNo ratings yet

- Best Contact Center Insurance PolicyDocument3 pagesBest Contact Center Insurance PolicyKrishnaNo ratings yet

- Com - Hdfcergo CRIPC 2311205143629000000Document3 pagesCom - Hdfcergo CRIPC 2311205143629000000Parul SinghNo ratings yet

- HDFCGA0312202100003212Document8 pagesHDFCGA0312202100003212Dhanush Shiva Dollaiah0% (1)

- Go Digit Two-Wheeler Liability Only Policy ScheduleDocument2 pagesGo Digit Two-Wheeler Liability Only Policy Scheduleharshil gandhiNo ratings yet

- Beat Car InsuranceDocument2 pagesBeat Car InsuranceSNo ratings yet

- Policy Schedule Certificate MotorDocument2 pagesPolicy Schedule Certificate MotorsssNo ratings yet

- Personal Loan Key Facts StatementDocument8 pagesPersonal Loan Key Facts StatementINAM JUNG GUJJARNo ratings yet

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsDocument3 pagesSub: Risk Assumption Letter: Insured & Vehicle DetailsViseshSatyannNo ratings yet

- Car CretaDocument7 pagesCar CretaSreekanth ChinthaNo ratings yet

- HDFC ERGO General Insurance Company Limited: Policy No. 2320 1005 1515 2200 000Document3 pagesHDFC ERGO General Insurance Company Limited: Policy No. 2320 1005 1515 2200 000SiddhantPatelNo ratings yet

- Welcome To Aditya Birla Insurance Brokers Limited, A Subsidiary of Aditya Birla Capital Limited!Document3 pagesWelcome To Aditya Birla Insurance Brokers Limited, A Subsidiary of Aditya Birla Capital Limited!Vaibhav SinghalNo ratings yet

- Acko Group Travel TC AbhibusDocument25 pagesAcko Group Travel TC AbhibusSreekanthNo ratings yet

- Digit Two-Wheeler Package Policy: Go Digit General Insurance LTDDocument2 pagesDigit Two-Wheeler Package Policy: Go Digit General Insurance LTDManoj KukrejaNo ratings yet

- AckoPolicy-DBTR00434107494 00Document2 pagesAckoPolicy-DBTR00434107494 00Syed's Way PoolNo ratings yet

- Policy PDFDocument4 pagesPolicy PDFshubhamNo ratings yet

- HDFC ERGO Health Insurance Policy SummaryDocument5 pagesHDFC ERGO Health Insurance Policy Summarynilesh sawantNo ratings yet

- Tata AIA Life Diamond Savings PlanDocument4 pagesTata AIA Life Diamond Savings Plansree db2No ratings yet

- Insurance PDFDocument2 pagesInsurance PDFJohn AjishNo ratings yet

- United India Insurance Company LimitedDocument11 pagesUnited India Insurance Company LimitedSrinu DebbatiNo ratings yet

- Hero InsuranceDocument1 pageHero InsuranceSwati AgarwalNo ratings yet

- Digit Two-Wheeler Package Policy: Go Digit General Insurance LTDDocument2 pagesDigit Two-Wheeler Package Policy: Go Digit General Insurance LTDDURAI RAJNo ratings yet

- Premium certificate for tax deduction under section 80DDocument2 pagesPremium certificate for tax deduction under section 80Dtamil2oooNo ratings yet

- Policy BreakdownDocument4 pagesPolicy BreakdownSparsh Panwar 067 F2No ratings yet

- TVS Credit Services Sanction Letter for OPPO Mobile LoanDocument2 pagesTVS Credit Services Sanction Letter for OPPO Mobile LoanVikas KumarNo ratings yet

- TW Niapolicyschedulecirtificatetw 89931793Document3 pagesTW Niapolicyschedulecirtificatetw 89931793Sachin SoniNo ratings yet

- Group Activ Secure - Certificate of InsuranceDocument4 pagesGroup Activ Secure - Certificate of InsuranceBanu MathyNo ratings yet

- The New India Assurance Co. Ltd. (Government of India Undertaking)Document3 pagesThe New India Assurance Co. Ltd. (Government of India Undertaking)sarath potnuriNo ratings yet

- AD 003 021 Your Car Insurance GuideDocument37 pagesAD 003 021 Your Car Insurance GuideDhar RakulNo ratings yet

- HR10J6570 - Acko Insurance Policy PDFDocument5 pagesHR10J6570 - Acko Insurance Policy PDFRitesh KumarNo ratings yet

- Acko Bike Policy - DBTR00126261926 - 00Document1 pageAcko Bike Policy - DBTR00126261926 - 00harshith sbNo ratings yet

- Policy Schedule: Digit Compulsory Personal Accident Policy Cover (Owner Driver)Document3 pagesPolicy Schedule: Digit Compulsory Personal Accident Policy Cover (Owner Driver)Mahender SinghNo ratings yet

- HDFC - Address Change FormDocument1 pageHDFC - Address Change FormChaitu RishanNo ratings yet

- 17-11-2022 Policy DocDocument1 page17-11-2022 Policy DocOfficial Sumit SafeshopNo ratings yet

- Policy Document BajajAllianz General InsuranceDocument6 pagesPolicy Document BajajAllianz General InsuranceVishnu PNo ratings yet

- PRULink Assurance Account Plus Sales Illustration SummaryDocument8 pagesPRULink Assurance Account Plus Sales Illustration SummaryErrol Rabe SolidariosNo ratings yet

- Future Generali India: Insurance Company LimitedDocument2 pagesFuture Generali India: Insurance Company Limitedstar pandiNo ratings yet

- Comprehensive Policy with ConsumablesDocument6 pagesComprehensive Policy with ConsumablesJeet TrivediNo ratings yet

- My InsuranceDocument2 pagesMy InsuranceAditya Abhay SinghNo ratings yet

- AckoPolicy-DBCR00557668657 00Document2 pagesAckoPolicy-DBCR00557668657 00pizza nmorevikNo ratings yet

- Group Personal Accident Policy CertificateDocument5 pagesGroup Personal Accident Policy CertificateChetan Ganesh RautNo ratings yet

- Confirmation of Your Two Wheeler Policy atDocument2 pagesConfirmation of Your Two Wheeler Policy atShiwam KumarNo ratings yet

- Iffco Tokio PolicyDocument1 pageIffco Tokio PolicyAdesh KumarNo ratings yet

- United India Insurance Company LimitedDocument9 pagesUnited India Insurance Company LimitedMumtaj KhudbuddinNo ratings yet

- The Oriental Insurance Company LimitedDocument3 pagesThe Oriental Insurance Company LimitedVishu SharmaNo ratings yet

- Keshan Amar ChauhanDocument3 pagesKeshan Amar ChauhanTusharNo ratings yet

- Cfi PDFDocument1 pageCfi PDFAmit KambojNo ratings yet

- Agent Name Khivraj Motors Agent Code MIS1000132 Agent Contact No 9108694880Document2 pagesAgent Name Khivraj Motors Agent Code MIS1000132 Agent Contact No 9108694880SanthoshNo ratings yet

- AckoPolicy-DCCR00184233989 00Document5 pagesAckoPolicy-DCCR00184233989 00Prakash ThimmaiahNo ratings yet

- PS/Consolidated Premium Statement /ver 2.1/jan 2021: A Reliance Capital CompanyDocument1 pagePS/Consolidated Premium Statement /ver 2.1/jan 2021: A Reliance Capital CompanyJhansi RokatiNo ratings yet

- Renewal of Your Easy Health Floater Standard Insurance PolicyDocument5 pagesRenewal of Your Easy Health Floater Standard Insurance PolicyMayur KrishnaNo ratings yet

- Activa NBike InsuranceDocument2 pagesActiva NBike InsuranceVeni PriyaNo ratings yet

- Anurag SinghDocument2 pagesAnurag SinghSureshJaiswalNo ratings yet

- Policy No Name Address:: ModeDocument2 pagesPolicy No Name Address:: ModerajNo ratings yet

- HDFC ErgoDocument1 pageHDFC ErgoPuneetNo ratings yet

- KNRC 3QFY17 Results Review Shows Strong Performance But Slowing Order GrowthDocument8 pagesKNRC 3QFY17 Results Review Shows Strong Performance But Slowing Order Growtharun_algoNo ratings yet

- Residential Recovery Awaited: Highlights of The QuarterDocument16 pagesResidential Recovery Awaited: Highlights of The QuartergbNo ratings yet

- En Bloc,: No.l 34IRGIDHC/2021Document2 pagesEn Bloc,: No.l 34IRGIDHC/2021arun_algoNo ratings yet

- ChangePro software reviewDocument6 pagesChangePro software reviewarun_algoNo ratings yet

- 08add - Edit - Search With Highlighting Pattern Dialog - ReSharperDocument9 pages08add - Edit - Search With Highlighting Pattern Dialog - ReSharperarun_algoNo ratings yet

- 14fast Native Structure Reading in C# Using Dynamic Assemblies - CodeProjectDocument6 pages14fast Native Structure Reading in C# Using Dynamic Assemblies - CodeProjectarun_algoNo ratings yet

- 0.1 New in ZUP From Version 151 Onwards. Im... Onix-TradeDocument18 pages0.1 New in ZUP From Version 151 Onwards. Im... Onix-Tradearun_algoNo ratings yet

- 08add - Edit - Search With Highlighting Pattern Dialog - ReSharperDocument9 pages08add - Edit - Search With Highlighting Pattern Dialog - ReSharperarun_algoNo ratings yet

- 14fast Native Structure Reading in C# Using Dynamic Assemblies - CodeProjectDocument6 pages14fast Native Structure Reading in C# Using Dynamic Assemblies - CodeProjectarun_algoNo ratings yet

- Hands-On Lab: Linq Project: Unified Language Features For Object and Relational QueriesDocument24 pagesHands-On Lab: Linq Project: Unified Language Features For Object and Relational Queriesarun_algoNo ratings yet

- HSL PCG "Currency Daily": 11 January, 2017Document6 pagesHSL PCG "Currency Daily": 11 January, 2017arun_algoNo ratings yet

- OIDocument13 pagesOIarun_algoNo ratings yet

- Indian Rupee Currency Market Technical Analysis and Hedging StrategiesDocument6 pagesIndian Rupee Currency Market Technical Analysis and Hedging Strategiesarun_algoNo ratings yet

- HSL PCG “CURRENCY DAILYDocument6 pagesHSL PCG “CURRENCY DAILYarun_algoNo ratings yet

- 08add - Edit - Search With Highlighting Pattern Dialog - ReSharperDocument9 pages08add - Edit - Search With Highlighting Pattern Dialog - ReSharperarun_algoNo ratings yet

- ChangePro software reviewDocument6 pagesChangePro software reviewarun_algoNo ratings yet

- HSL Techno Edge: Retail ResearchDocument3 pagesHSL Techno Edge: Retail Researcharun_algoNo ratings yet

- HSL PCG "Currency Daily": 05 January, 2017Document6 pagesHSL PCG "Currency Daily": 05 January, 2017arun_algoNo ratings yet

- Reset A MySQL Root Password PDFDocument3 pagesReset A MySQL Root Password PDFarun_algoNo ratings yet

- HSL PCG "Currency Insight"-Weekly: 07 January, 2017Document16 pagesHSL PCG "Currency Insight"-Weekly: 07 January, 2017arun_algoNo ratings yet

- Indian Rupee Currency Market Moves and Hedging StrategiesDocument6 pagesIndian Rupee Currency Market Moves and Hedging Strategiesarun_algoNo ratings yet

- HSL PCG "Currency Daily": 06 January, 2017Document6 pagesHSL PCG "Currency Daily": 06 January, 2017arun_algoNo ratings yet

- HSL Techno Edge: Retail ResearchDocument3 pagesHSL Techno Edge: Retail Researcharun_algoNo ratings yet

- HSL PCG "Currency Daily": 19 January, 2017Document6 pagesHSL PCG "Currency Daily": 19 January, 2017arun_algoNo ratings yet

- HSL PCG "Currency Daily": 18 January, 2017Document6 pagesHSL PCG "Currency Daily": 18 January, 2017arun_algoNo ratings yet

- HSL PCG "Currency Daily": 17 January, 2017Document6 pagesHSL PCG "Currency Daily": 17 January, 2017arun_algoNo ratings yet

- ReportDocument6 pagesReportarun_algoNo ratings yet

- HSL PCG "Currency Daily": 18 January, 2017Document6 pagesHSL PCG "Currency Daily": 18 January, 2017arun_algoNo ratings yet

- ReportDocument6 pagesReportarun_algoNo ratings yet

- HSL PCG "Currency Daily": 31 January, 2017Document6 pagesHSL PCG "Currency Daily": 31 January, 2017arun_algoNo ratings yet

- HSL PCG Currency Daily OutlookDocument6 pagesHSL PCG Currency Daily Outlookarun_algoNo ratings yet

- HSL PCG "Currency Daily": 25 January, 2017Document6 pagesHSL PCG "Currency Daily": 25 January, 2017arun_algoNo ratings yet

- Source of Income Inequality PDFDocument16 pagesSource of Income Inequality PDFBeni GunawanNo ratings yet

- Sox PDFDocument8 pagesSox PDFRoland ValNo ratings yet

- Real Downstream Internet-Based Supply Chain Management: Hcorrea@Document23 pagesReal Downstream Internet-Based Supply Chain Management: Hcorrea@JeanCassioNo ratings yet

- Warren Buffett 1997 BRK Annual Report To ShareholdersDocument20 pagesWarren Buffett 1997 BRK Annual Report To ShareholdersBrian McMorrisNo ratings yet

- QuizletDocument4 pagesQuizletKizzea Bianca GadotNo ratings yet

- Philguarantee Vs VPECI and 3plexDocument1 pagePhilguarantee Vs VPECI and 3plexChaNo ratings yet

- Corporate GuaranteeDocument14 pagesCorporate GuaranteeAkio ChingNo ratings yet

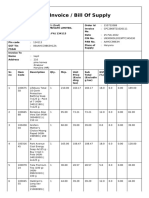

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKapil SinglaNo ratings yet

- Errata 2020Document3 pagesErrata 2020SamNo ratings yet

- "The Philippines" in Political Parties and Democracy: Western Europe, East and Southeast Asia 1990-2010Document19 pages"The Philippines" in Political Parties and Democracy: Western Europe, East and Southeast Asia 1990-2010Julio TeehankeeNo ratings yet

- Level Up Lesson Plans Banking 101 DDocument15 pagesLevel Up Lesson Plans Banking 101 DPriyanka artsNo ratings yet

- Pricing: Weygandt - Kieso - KimmelDocument66 pagesPricing: Weygandt - Kieso - KimmelSMBNo ratings yet

- GayanDocument23 pagesGayanijayathungaNo ratings yet

- Education Loans For Higher StudiesDocument7 pagesEducation Loans For Higher StudiesSREYANo ratings yet

- Cash and Cash EquivalentsDocument20 pagesCash and Cash EquivalentsPetrina100% (1)

- CA Final SFM Very Short Formula Book Nov 2020Document36 pagesCA Final SFM Very Short Formula Book Nov 2020Romaric DjokoNo ratings yet

- Risk and Rates of ReturnDocument16 pagesRisk and Rates of ReturnSally Goodwill100% (1)

- Teach A Man How To FishDocument9 pagesTeach A Man How To FishRonak SinghNo ratings yet

- SJFM Coop ByLawsDocument10 pagesSJFM Coop ByLawsruth sab-itNo ratings yet

- Can India Afford To Boycott Chinese ProductsDocument2 pagesCan India Afford To Boycott Chinese ProductsSowmya MinnuNo ratings yet

- Government Accounting & Financial RulesDocument9 pagesGovernment Accounting & Financial RulesSouvik DattaNo ratings yet

- Chinese Bond Buying ProgramDocument2 pagesChinese Bond Buying Programshahil_4u100% (1)

- LLQP Financial Math2015sampleDocument10 pagesLLQP Financial Math2015sampleYat ChiuNo ratings yet

- Income Statement Quarterly DataDocument2 pagesIncome Statement Quarterly DataelninothekidNo ratings yet

- Capital MarketDocument16 pagesCapital Marketdeepika90236100% (1)

- SGB40 Issue PriceDocument1 pageSGB40 Issue PriceAkashTripathiNo ratings yet

- 556 l6 Breach of TrustDocument18 pages556 l6 Breach of TrustAttyynHazwaniNo ratings yet

- Sample Resolution Transfer-SignatoriesDocument2 pagesSample Resolution Transfer-SignatoriesJaymart C. EstradaNo ratings yet

- Swan Energy LTDDocument29 pagesSwan Energy LTDvsrsNo ratings yet