You might also like

- Quarterly Business Review PowerPoint Presentation SlidesDocument57 pagesQuarterly Business Review PowerPoint Presentation SlidesSlideTeam60% (5)

- On The Shoulders of Giants - Mental Models For The New MilleniumDocument17 pagesOn The Shoulders of Giants - Mental Models For The New Milleniumpjs15No ratings yet

- Parag Q2 FY19 EdelDocument9 pagesParag Q2 FY19 EdelRohan AdlakhaNo ratings yet

- IndiGo IBDocument5 pagesIndiGo IBMadhav sharmaNo ratings yet

- 3Q17 Earning Eng FinalDocument18 pages3Q17 Earning Eng FinalarakeelNo ratings yet

- Note For Investment Operation CommitteeDocument4 pagesNote For Investment Operation CommitteeAyushi somaniNo ratings yet

- Investor Presentation February 2019 PDFDocument31 pagesInvestor Presentation February 2019 PDFkartik jangidNo ratings yet

- Analysts Meet - 2010Document17 pagesAnalysts Meet - 2010shabbir batterywalaNo ratings yet

- Mahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Document14 pagesMahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Yash DoshiNo ratings yet

- Manappuram Finance Investor PresentationDocument43 pagesManappuram Finance Investor PresentationabmahendruNo ratings yet

- CJ - Credit SuiseDocument24 pagesCJ - Credit Suisebackup tringuyenNo ratings yet

- Earnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - NsDocument34 pagesEarnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - Nssunil.dasarath jadhavNo ratings yet

- Capa CiteDocument29 pagesCapa CiteParas ChhedaNo ratings yet

- Mahindra & Mahindra: 3 August 2009Document8 pagesMahindra & Mahindra: 3 August 2009Chandni OzaNo ratings yet

- Investor Presentation 30.09.2023Document30 pagesInvestor Presentation 30.09.2023amitsbhatiNo ratings yet

- 2018 Aug M&M ReportDocument12 pages2018 Aug M&M ReportVivek shindeNo ratings yet

- Budget Call Circular FY2017 39 - 080716Document13 pagesBudget Call Circular FY2017 39 - 080716sorenttoNo ratings yet

- Ambuja Cements: NeutralDocument8 pagesAmbuja Cements: Neutral张迪No ratings yet

- Parag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyDocument10 pagesParag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyNiravAcharyaNo ratings yet

- In V Pre 18022020Document33 pagesIn V Pre 18022020Anshul JainNo ratings yet

- IcsiDocument12 pagesIcsiUday NegiNo ratings yet

- Bronch AdDocument23 pagesBronch AdAbdelrahman NazmiNo ratings yet

- MD & Ceo CFO CRO CIO: Note For Investment Operation CommitteeDocument4 pagesMD & Ceo CFO CRO CIO: Note For Investment Operation CommitteeAyushi somaniNo ratings yet

- Top 17 Stocks BuyDocument13 pagesTop 17 Stocks BuySushilNo ratings yet

- Earning PresentationDocument15 pagesEarning PresentationNilesh SonarNo ratings yet

- BLS International 2QFY19 (CMP Rs 128, Mcap Rs 13bn, Fair Value Rs 277)Document1 pageBLS International 2QFY19 (CMP Rs 128, Mcap Rs 13bn, Fair Value Rs 277)Ashutosh GuptaNo ratings yet

- ST BK of IndiaDocument42 pagesST BK of IndiaSuyaesh SinghaniyaNo ratings yet

- Target FinancialsDocument15 pagesTarget Financialsso_levictorNo ratings yet

- Maintain NEUTRAL: Acem in CMP Rs 219 Target Rs 191 ( 13%)Document7 pagesMaintain NEUTRAL: Acem in CMP Rs 219 Target Rs 191 ( 13%)9987303726No ratings yet

- Q3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleDocument12 pagesQ3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleSAGAR VAZIRANINo ratings yet

- Ashok Leyland Kotak 050218Document4 pagesAshok Leyland Kotak 050218suprabhattNo ratings yet

- Analysts Meet May068Document34 pagesAnalysts Meet May068Sabarish_1991No ratings yet

- NOCILDocument44 pagesNOCILsingh66222No ratings yet

- Investors - Presentation - 11-02-2021 Low MarginDocument32 pagesInvestors - Presentation - 11-02-2021 Low Marginravi.youNo ratings yet

- Investors / Analyst's Presentation For December 31, 2016 (Company Update)Document16 pagesInvestors / Analyst's Presentation For December 31, 2016 (Company Update)Shyam SunderNo ratings yet

- Sintex Industries (SININD) : Growth To Moderate FurtherDocument7 pagesSintex Industries (SININD) : Growth To Moderate Furtherred cornerNo ratings yet

- Nisha PPT 1Document13 pagesNisha PPT 1Anonymous Fr37v90cqNo ratings yet

- Investor Presentation - February 2017 (Company Update)Document37 pagesInvestor Presentation - February 2017 (Company Update)Shyam SunderNo ratings yet

- Tata MotorsDocument5 pagesTata Motorsinsurana73No ratings yet

- Key Performance Indicators Y/E MarchDocument1 pageKey Performance Indicators Y/E Marchretrov androsNo ratings yet

- Axiata Data Financials 4Q21bDocument11 pagesAxiata Data Financials 4Q21bhimu_050918No ratings yet

- Sapm AssignmentDocument4 pagesSapm Assignment401-030 B. Harika bcom regNo ratings yet

- Momo Operating Report 2022 Q4Document5 pagesMomo Operating Report 2022 Q4Harris ChengNo ratings yet

- Result Presentation (Result)Document14 pagesResult Presentation (Result)Shyam SunderNo ratings yet

- Equity Valuation: REDS-Research Equity Database System Page 1 of 2Document2 pagesEquity Valuation: REDS-Research Equity Database System Page 1 of 2Ariansyah NobelNo ratings yet

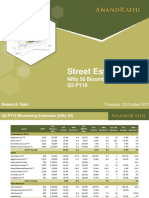

- Nifty50 Q2 FY18 Quarterly EstimatesDocument8 pagesNifty50 Q2 FY18 Quarterly Estimatessrinivas NNo ratings yet

- Extraordinary When One Looks at The Performance of The Broader Universe" As Well As WhenDocument9 pagesExtraordinary When One Looks at The Performance of The Broader Universe" As Well As Whenravi_405No ratings yet

- Stock Price & Pattern of ShareholdingDocument15 pagesStock Price & Pattern of ShareholdingdanyalNo ratings yet

- Top Glove 140618Document5 pagesTop Glove 140618Joseph CampbellNo ratings yet

- Avanti Feeds Limited: Q4 & FY20 Result Presentation JULY 2020Document25 pagesAvanti Feeds Limited: Q4 & FY20 Result Presentation JULY 2020Avinash PatraNo ratings yet

- Sun Pharma: CMP: INR909 TP: INR1,000 BuyDocument8 pagesSun Pharma: CMP: INR909 TP: INR1,000 BuyKannan JainNo ratings yet

- Nazara Technologies LimitedDocument35 pagesNazara Technologies LimitedMadhan RajNo ratings yet

- Equity Valuation: REDS-Research Equity Database System Page 1 of 2Document2 pagesEquity Valuation: REDS-Research Equity Database System Page 1 of 2Ariansyah NobelNo ratings yet

- GR I Crew XV 2018 TcsDocument79 pagesGR I Crew XV 2018 TcsMUKESH KUMARNo ratings yet

- TS - MSCI Indonesia Nov-21 Rebalancing PreviewDocument6 pagesTS - MSCI Indonesia Nov-21 Rebalancing PreviewAdri KhosasihNo ratings yet

- Dividend Stocks ListDocument4 pagesDividend Stocks ListAnjaiah PittalaNo ratings yet

- 2023 07 27 PH e PgoldDocument6 pages2023 07 27 PH e PgoldexcA1996No ratings yet

- Cipla: Performance HighlightsDocument8 pagesCipla: Performance HighlightsKapil AthwaniNo ratings yet

- Semen Indonesia Persero TBK PT: at A GlanceDocument3 pagesSemen Indonesia Persero TBK PT: at A GlanceRendy SentosaNo ratings yet

- Harga Wajar DBIDocument40 pagesHarga Wajar DBISeptiawanNo ratings yet

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioFrom EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- 3M List PDFDocument2 pages3M List PDFsaveclipNo ratings yet

- Revision of Landline Plan With Added Freebies': BSNL Chennai TelephonesDocument1 pageRevision of Landline Plan With Added Freebies': BSNL Chennai TelephonessaveclipNo ratings yet

- ACC AHA ACE 2003 Guideline Update For The Clinical PDFDocument99 pagesACC AHA ACE 2003 Guideline Update For The Clinical PDFsaveclipNo ratings yet

- 8th National TEE-Application 2014Document1 page8th National TEE-Application 2014saveclipNo ratings yet

- Corporate Banking Seminar: Trade FinanceDocument26 pagesCorporate Banking Seminar: Trade FinancePierreNo ratings yet

- Sangmi Nazir 2010 Assset QualityDocument17 pagesSangmi Nazir 2010 Assset QualitycarltondurrantNo ratings yet

- Corporate Governance in PakistanDocument11 pagesCorporate Governance in PakistanSehrish Nadeem KitchlewNo ratings yet

- Startup Funding: The Startup Founder'S Guide ToDocument28 pagesStartup Funding: The Startup Founder'S Guide ToNguyen ThieuNo ratings yet

- International Credit Rating AgencyDocument4 pagesInternational Credit Rating AgencyDibesh PadiaNo ratings yet

- Chapter 4: Option Pricing Models: The Binomial ModelDocument9 pagesChapter 4: Option Pricing Models: The Binomial ModelDUY LE NHAT TRUONGNo ratings yet

- Self Storage 7Document13 pagesSelf Storage 7RobNo ratings yet

- Whitepaper DF Transition ManagementDocument5 pagesWhitepaper DF Transition ManagementCaixing LinNo ratings yet

- Ccri Pcram Final 1pDocument48 pagesCcri Pcram Final 1paquaboi924No ratings yet

- Corporate Law Firm Headquartered in Lahore PakistanDocument6 pagesCorporate Law Firm Headquartered in Lahore PakistanRana EhsanNo ratings yet

- Gitanjali Amit MandalDocument2 pagesGitanjali Amit MandalAmit KumarNo ratings yet

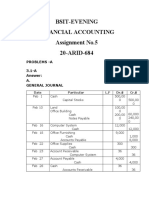

- Assignment No.5 AccountingDocument6 pagesAssignment No.5 Accountingibrar ghaniNo ratings yet

- SGX-Listed Hatten Land Diversifies Beyond Melaka Through Proposed Acquisition of Unicity in Seremban, MalaysiaDocument3 pagesSGX-Listed Hatten Land Diversifies Beyond Melaka Through Proposed Acquisition of Unicity in Seremban, MalaysiaWeR1 Consultants Pte LtdNo ratings yet

- Module Wise Important Questions and AnswersDocument31 pagesModule Wise Important Questions and AnswersViraja GuruNo ratings yet

- Order Exposure and Parasitic TradersDocument22 pagesOrder Exposure and Parasitic TradersNo NameNo ratings yet

- How To Pay Off A 30-Year Mortgage in 15 Years - Tips & TricksDocument6 pagesHow To Pay Off A 30-Year Mortgage in 15 Years - Tips & TricksdhanahbalNo ratings yet

- Eb Ceg in The Line of MoneyDocument33 pagesEb Ceg in The Line of MoneyPayal MehtaNo ratings yet

- Prompt Corrective ActionsDocument1 pagePrompt Corrective Actionsnir_lord100% (1)

- Somya Amritanshu - Arcpa1206b - Q3 - Ay202223Document2 pagesSomya Amritanshu - Arcpa1206b - Q3 - Ay202223Sourabh PunshiNo ratings yet

- Finance & Accounts SectionDocument4 pagesFinance & Accounts SectionSheraz gondalNo ratings yet

- Petroleum Economic Decision ToolsDocument40 pagesPetroleum Economic Decision ToolscjNo ratings yet

- Apc Recruitment FatemaDocument44 pagesApc Recruitment FatemaMehboobe FatemaNo ratings yet

- 06 - Corp Summary Oh 2011 - PDFDocument8 pages06 - Corp Summary Oh 2011 - PDFhqi777No ratings yet

- PDFs Wiseman 2011-03 SynopsisDocument10 pagesPDFs Wiseman 2011-03 Synopsisnavinvijay2No ratings yet

- Financial Statement AnalysisDocument26 pagesFinancial Statement Analysissagar7No ratings yet

- Part 6 Assessment of RiskDocument2 pagesPart 6 Assessment of RiskEn MonsalveNo ratings yet

- Bba + Ba Iv Sem - BFM - Nitin BansalDocument6 pagesBba + Ba Iv Sem - BFM - Nitin BansalAria MazeNo ratings yet