You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- HW2 - DH Frames and FKDocument4 pagesHW2 - DH Frames and FKrhett.d.miller9555No ratings yet

- In-N-Out Burger Allergen Information: Our Food Does Not Contain Peanuts, Tree Nuts, Sesame, Shellfish, or FishDocument1 pageIn-N-Out Burger Allergen Information: Our Food Does Not Contain Peanuts, Tree Nuts, Sesame, Shellfish, or Fishrhett.d.miller9555No ratings yet

- Position Purpose: Senior Project ManagerDocument2 pagesPosition Purpose: Senior Project Managerrhett.d.miller9555No ratings yet

- Four Year Program PHIL BSDocument1 pageFour Year Program PHIL BSrhett.d.miller9555No ratings yet

- KF FeSCNDocument15 pagesKF FeSCNrhett.d.miller9555No ratings yet

- NIKE Inc Ten Year Financial History FY19Document1 pageNIKE Inc Ten Year Financial History FY19Moisés Ríos RamosNo ratings yet

- DSIJ3209Document84 pagesDSIJ3209Navin ChandarNo ratings yet

- Chapter:-1: Vision of The CompanyDocument64 pagesChapter:-1: Vision of The CompanyRavi ShettyNo ratings yet

- Soup To Nuts Seminar SeriesDocument33 pagesSoup To Nuts Seminar SeriesEmmanuel Benedict Bosque IcaranomNo ratings yet

- Chapter 12 PDFDocument94 pagesChapter 12 PDFSrikanth GudipatiNo ratings yet

- (Download pdf) Corporate Finance 13Th Edition Bradford D Jordan Stephen A Ross full chapter pdf docxDocument69 pages(Download pdf) Corporate Finance 13Th Edition Bradford D Jordan Stephen A Ross full chapter pdf docxkiyawaotomo100% (5)

- Sebi GuidelinesDocument44 pagesSebi Guidelinesdivya57trueNo ratings yet

- Full Download Test Bank For Essentials of Investments 10th Edition Zvi Bodie Alex Kane Alan Marcus PDF Full ChapterDocument36 pagesFull Download Test Bank For Essentials of Investments 10th Edition Zvi Bodie Alex Kane Alan Marcus PDF Full Chapterpated.tylarus.q4knl100% (17)

- TYBFM A 36 Vignesh Khandelwal Black BookDocument74 pagesTYBFM A 36 Vignesh Khandelwal Black Bookpreet doshiNo ratings yet

- CF Berk DeMarzo Harford Chapter 13 Problem AnswerDocument9 pagesCF Berk DeMarzo Harford Chapter 13 Problem AnswerRachel Cheng0% (1)

- Glossary On Mutual FundsDocument17 pagesGlossary On Mutual FundsBabasab Patil (Karrisatte)No ratings yet

- Activity 10Document2 pagesActivity 10Randelle James FiestaNo ratings yet

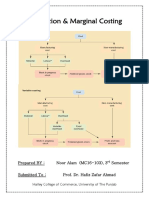

- Absorption & Marginal Costing - Noor Alam (MC16-103)Document24 pagesAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- Balance Sheet of GTL: Unsecured LoansDocument7 pagesBalance Sheet of GTL: Unsecured LoansMeryl FernsNo ratings yet

- Indian Amusement Parks IndustryDocument23 pagesIndian Amusement Parks Industrykiranmai2567% (3)

- Law Compilation of ActquizDocument15 pagesLaw Compilation of ActquizMychie Lynne MayugaNo ratings yet

- Ark Etf Trust: Semi-Annual ReportDocument45 pagesArk Etf Trust: Semi-Annual ReportTam JackNo ratings yet

- Castillo vs. BalinghasayDocument2 pagesCastillo vs. BalinghasayClark Edward Runes UyticoNo ratings yet

- TT-2 MCQDocument7 pagesTT-2 MCQKapilBudhiraja100% (1)

- India Glycols 2018-19 PDFDocument162 pagesIndia Glycols 2018-19 PDFPuneet367No ratings yet

- Chapter 3 - The Economic Models and The Flow of ProductionDocument16 pagesChapter 3 - The Economic Models and The Flow of Productionancaye1962No ratings yet

- Industrial Management - Slide PDFDocument107 pagesIndustrial Management - Slide PDFShahed MahmudNo ratings yet

- SAP Materials Management OverViewDocument243 pagesSAP Materials Management OverViewMihai Toma75% (4)

- Bba 205Document458 pagesBba 205divya kalyaniNo ratings yet

- Fundamental Analysis Technical Analysis Chartists: Why Does It Happen?Document3 pagesFundamental Analysis Technical Analysis Chartists: Why Does It Happen?noniiiiNo ratings yet

- FCEBDocument3 pagesFCEBRedefining Success KashishNo ratings yet

- PDF Investment Analysis and Portfolio Management 11Th Edition Frank K Reilly Ebook Full ChapterDocument53 pagesPDF Investment Analysis and Portfolio Management 11Th Edition Frank K Reilly Ebook Full Chaptermargaret.redd792100% (1)

- Meiditya Larasati - 01017190019 - PR Pertemuan 03Document9 pagesMeiditya Larasati - 01017190019 - PR Pertemuan 03Haikal RafifNo ratings yet

- Financial MarketsDocument3 pagesFinancial Marketspatrick bolo100% (1)

- Methanex OverviewDocument57 pagesMethanex OverviewHelixNo ratings yet