You might also like

- Pak Enings HTDocument15 pagesPak Enings HTVincent SampianoNo ratings yet

- Problem 5: QuestionsDocument6 pagesProblem 5: QuestionsTk KimNo ratings yet

- Cash and Cash EquivDocument8 pagesCash and Cash EquivMonina Cabalag0% (1)

- Chapter-5 Homework InventoriesDocument4 pagesChapter-5 Homework InventoriesKenneth Christian Wilbur0% (1)

- Audit Problem Inventories AnswerDocument6 pagesAudit Problem Inventories AnswerJames PaulNo ratings yet

- 2 1Document1 page2 1riza147No ratings yet

- Audit of Invest. in Equity and Debt SecuritiesDocument23 pagesAudit of Invest. in Equity and Debt SecuritiesJoseph SalidoNo ratings yet

- Audit of Inventories - STDocument7 pagesAudit of Inventories - STFrancine Holler0% (2)

- Problems Audit of InvestmentsDocument15 pagesProblems Audit of InvestmentsKm de Leon75% (4)

- Audit For ReceivablesDocument1 pageAudit For ReceivablesXandae MempinNo ratings yet

- Business Com Chapter 23Document5 pagesBusiness Com Chapter 23Nino Joycelee TuboNo ratings yet

- Audit Prob Cash AnsDocument7 pagesAudit Prob Cash AnsNoreen BinagNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument5 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErwin Labayog MedinaNo ratings yet

- Far 03 - InventoryDocument7 pagesFar 03 - InventoryMark Domingo MendozaNo ratings yet

- 3 1Document1 page3 1riza147No ratings yet

- AudcisDocument6 pagesAudcisJessa May MendozaNo ratings yet

- Finals Answer KeyDocument6 pagesFinals Answer Keymarx marolinaNo ratings yet

- DocxDocument25 pagesDocxPhilip Castro67% (3)

- Documento - MX Ap Receivables Quizzer QDocument10 pagesDocumento - MX Ap Receivables Quizzer QMiel Viason CañeteNo ratings yet

- TRAPO, Inc. Estimates Its Bad Debt Losses by Aging Its Accounts Receivable. The Aging Schedule ofDocument2 pagesTRAPO, Inc. Estimates Its Bad Debt Losses by Aging Its Accounts Receivable. The Aging Schedule ofAlvinDumanggasNo ratings yet

- A Owns Majority of The Outstanding Ordinary SharesDocument2 pagesA Owns Majority of The Outstanding Ordinary Sharesasdfghjkl zxcvbnm100% (1)

- Advac SemifinalDocument8 pagesAdvac SemifinalDIVINE VILLENANo ratings yet

- Solutions Exercises CashDocument4 pagesSolutions Exercises CashPrince CalicaNo ratings yet

- Practical Accounting 1: 2011 National Cpa Mock Board ExaminationDocument7 pagesPractical Accounting 1: 2011 National Cpa Mock Board Examinationcacho cielo graceNo ratings yet

- INVESTMENTS inDocument7 pagesINVESTMENTS inJessa May MendozaNo ratings yet

- Audit of Allowance For Doubtful AccountsDocument4 pagesAudit of Allowance For Doubtful AccountsCJ alandyNo ratings yet

- Prelim Exam ManuscriptDocument10 pagesPrelim Exam ManuscriptJulie Mae Caling MalitNo ratings yet

- QuizDocument15 pagesQuizMark Domingo Mendoza100% (1)

- Chapter 14 Multiple Choices: PROB. 14 - 1 (IAS)Document12 pagesChapter 14 Multiple Choices: PROB. 14 - 1 (IAS)jek vinNo ratings yet

- Aud Activity 1Document10 pagesAud Activity 1sethdrea officialNo ratings yet

- Lesson 2 (Week 2) - Investment in Equity SecuritiesDocument10 pagesLesson 2 (Week 2) - Investment in Equity SecuritiesMonica MonicaNo ratings yet

- Group 8Document31 pagesGroup 8Jessa E. FabilaneNo ratings yet

- Emilio Aguinaldo College - Cavite Campus School of Business AdministrationDocument8 pagesEmilio Aguinaldo College - Cavite Campus School of Business AdministrationKarlayaanNo ratings yet

- Home Office BranchDocument5 pagesHome Office BranchRodNo ratings yet

- This Study Resource Was: QuestionsDocument5 pagesThis Study Resource Was: QuestionsXNo ratings yet

- Assignment No. 3 Audit of InventoriesDocument6 pagesAssignment No. 3 Audit of InventoriesMa Tiffany Gura Roble100% (1)

- NKNKDocument18 pagesNKNKSophia PerezNo ratings yet

- CHAPTER 10 - Pre-Board Examinations-1Document35 pagesCHAPTER 10 - Pre-Board Examinations-1Mr.AccntngNo ratings yet

- Tutorial BienDocument2 pagesTutorial BienCarlo Baculo100% (1)

- Iacc 1 - Quizzer Cash and Cash EquivalentDocument3 pagesIacc 1 - Quizzer Cash and Cash EquivalentJerry Toledo0% (1)

- S SdfafdafdafdafDocument8 pagesS SdfafdafdafdafMark Domingo MendozaNo ratings yet

- MQ 1 Receivables and InventoryDocument4 pagesMQ 1 Receivables and Inventorymarygraceomac100% (2)

- Audit of Inventories and Cost of Goods SDocument10 pagesAudit of Inventories and Cost of Goods SJessaNo ratings yet

- Cash and Cash Equivalent: Problem 1Document4 pagesCash and Cash Equivalent: Problem 1Ab CNo ratings yet

- Q06A Audit of Non Cash AssetsDocument7 pagesQ06A Audit of Non Cash AssetsChristine Jane ParroNo ratings yet

- Problem 2Document4 pagesProblem 2redassdawn100% (1)

- Audit of Inventories Roque 2018Document61 pagesAudit of Inventories Roque 2018Anna TaylorNo ratings yet

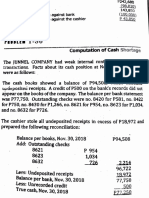

- Cash Shortage Computation: SolutionDocument4 pagesCash Shortage Computation: SolutionCJ alandyNo ratings yet

- Auditing Problems: Audit of Cash and Cash Equivalents Problem No. 1Document21 pagesAuditing Problems: Audit of Cash and Cash Equivalents Problem No. 1ATLASNo ratings yet

- Ap-1403 ReceivablesDocument18 pagesAp-1403 ReceivablesElaine YapNo ratings yet

- AFST Practice Set 02 Partnership (Part 2)Document3 pagesAFST Practice Set 02 Partnership (Part 2)Alain CopperNo ratings yet

- Exercise Bank ReconDocument9 pagesExercise Bank ReconDeviline MichelleNo ratings yet

- 09.30.2017 Audit of CashDocument7 pages09.30.2017 Audit of CashPatOcampoNo ratings yet

- Final Exam 12 PDF FreeDocument17 pagesFinal Exam 12 PDF FreeEmey CalbayNo ratings yet

- Auditing Report CASE11Document18 pagesAuditing Report CASE11Coke Aidenry Saludo0% (1)

- Aud. Prob.Document16 pagesAud. Prob.Ria Alanis CastilloNo ratings yet

- CCE Quiz Batasan Set - SolutionDocument4 pagesCCE Quiz Batasan Set - SolutionJoovs JoovhoNo ratings yet

- aud-C&CE-online ReviewerDocument26 pagesaud-C&CE-online Reviewerdave excelleNo ratings yet

- NoteDocument16 pagesNoteJay-an AntipoloNo ratings yet

- Cash and Cash EquivalentsDocument8 pagesCash and Cash EquivalentsmissyNo ratings yet

- ERC AP 1901 InventoriesDocument8 pagesERC AP 1901 Inventoriesjikee11No ratings yet

- DocxDocument35 pagesDocxjikee11No ratings yet

- Dimacali, Johnpaul C.: Character ReferencesDocument2 pagesDimacali, Johnpaul C.: Character Referencesjikee11No ratings yet

- Handouts PDFDocument374 pagesHandouts PDFVicky Danila Albano60% (5)

- The Impact of Accounting Information SystemsDocument22 pagesThe Impact of Accounting Information Systemsjikee11No ratings yet

- Computer Accounting With QuickBooks 2011 13th Edition Donna KayChap0021Document12 pagesComputer Accounting With QuickBooks 2011 13th Edition Donna KayChap0021jikee11No ratings yet

- Dow University of Health Sciences: Vacancies of Non-Teaching StaffDocument2 pagesDow University of Health Sciences: Vacancies of Non-Teaching Staffjikee11No ratings yet

- GKK Monthly Summary - ShortDocument5 pagesGKK Monthly Summary - Shortjikee11No ratings yet

- DocxDocument17 pagesDocxjikee11No ratings yet

- Contribution: Chapel ProjectDocument3 pagesContribution: Chapel Projectjikee11No ratings yet

- QuizletDocument3 pagesQuizletjikee11No ratings yet

- GKK San Miguel Parish Prex Seminar Batch 92 Liquidation Report (Jan 5-8, 2018)Document2 pagesGKK San Miguel Parish Prex Seminar Batch 92 Liquidation Report (Jan 5-8, 2018)jikee11No ratings yet

- Handouts PDFDocument374 pagesHandouts PDFVicky Danila Albano60% (5)

- DocDocument31 pagesDocjikee11No ratings yet

- DocxDocument48 pagesDocxjikee1150% (2)

- Prob 3Document2 pagesProb 3jikee11No ratings yet

- Sample Ch09Document54 pagesSample Ch09jikee11No ratings yet

- Prob 3Document3 pagesProb 3jikee11No ratings yet

- Cpa Review School - Prac 1Document12 pagesCpa Review School - Prac 1jikee1150% (2)

- Corp LiquiDocument15 pagesCorp Liquijikee11No ratings yet

- Detail Notice Inviting TenderDocument17 pagesDetail Notice Inviting Tenderjikee11No ratings yet

- High School Graduation SpeechDocument11 pagesHigh School Graduation SpeechEmma MulletNo ratings yet

- Analysis of Sales Process and Operations of Retail Branch Banking System in HDFC BankDocument136 pagesAnalysis of Sales Process and Operations of Retail Branch Banking System in HDFC BankShahnawaz AliNo ratings yet

- Obligations Are ExtinguishedDocument24 pagesObligations Are ExtinguishedikayNo ratings yet

- (#3) Basic Concepts of Risk and Return, and The Time Value of MoneyDocument22 pages(#3) Basic Concepts of Risk and Return, and The Time Value of MoneyBianca Jane GaayonNo ratings yet

- Colinares & Veloso vs. CA (Edited)Document3 pagesColinares & Veloso vs. CA (Edited)Ton RiveraNo ratings yet

- DicgcDocument11 pagesDicgcPranav ShahNo ratings yet

- Paytm Payment Solutions Feb15 PDFDocument30 pagesPaytm Payment Solutions Feb15 PDFRomeo MalikNo ratings yet

- Account Statement From 1 Nov 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 1 Nov 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceMukesh SharmaNo ratings yet

- Sukhchain Aggarwal: Financial Statement Analysis of ICICI BankDocument1 pageSukhchain Aggarwal: Financial Statement Analysis of ICICI Banksandy_jadhaoNo ratings yet

- PAHAL - NGO From Uttarakhand MicrofinanceDocument6 pagesPAHAL - NGO From Uttarakhand MicrofinanceMayank Tandon100% (2)

- Financial Accounting 1 by HaroldDocument392 pagesFinancial Accounting 1 by HaroldRobertKimtaiNo ratings yet

- SEIC 2019 Handbook PDFDocument24 pagesSEIC 2019 Handbook PDFYing ShengNo ratings yet

- Branch List Offering Doorstep Banking12012020Document36 pagesBranch List Offering Doorstep Banking12012020Avijit ParidaNo ratings yet

- KYC Know Your CustomerDocument29 pagesKYC Know Your CustomerAsad AliNo ratings yet

- Alfacurrate AAA PMS Jul16Document39 pagesAlfacurrate AAA PMS Jul16flytorahulNo ratings yet

- Kotak Prime: About Kotak Mahindra GroupDocument11 pagesKotak Prime: About Kotak Mahindra GrouptrishlaNo ratings yet

- BPI Employees Union Vs Bank of The Philippine IslandDocument6 pagesBPI Employees Union Vs Bank of The Philippine IslandAllen OlayvarNo ratings yet

- RAF List Sep 1939Document552 pagesRAF List Sep 1939Robert MacDonaldNo ratings yet

- EBS Payment Gateway ProposalDocument8 pagesEBS Payment Gateway ProposalBarun SahaNo ratings yet

- Chief Executive Officer CEO Turnaround in San Diego CA Resume Robert CampbellDocument2 pagesChief Executive Officer CEO Turnaround in San Diego CA Resume Robert CampbellRobertCampbell1No ratings yet

- Centrum Wealth Ratnamani Metals - Initiating CoverageDocument11 pagesCentrum Wealth Ratnamani Metals - Initiating Coveragenarayanan_rNo ratings yet

- Accounting 1B HomeworkDocument3 pagesAccounting 1B HomeworketernitystarNo ratings yet

- UPI PG RBI - Final PDFDocument83 pagesUPI PG RBI - Final PDFpratik zankeNo ratings yet

- Bank Secrecy LawDocument33 pagesBank Secrecy LawTen Laplana100% (4)

- Maxim Bay Al SalamDocument17 pagesMaxim Bay Al SalamNaim ARNo ratings yet

- Universidad Iberoamericana - Unibe-: Disbursement RecordDocument2 pagesUniversidad Iberoamericana - Unibe-: Disbursement Recordodontologia unibeNo ratings yet

- Atty. Leon L. Asa, Et Al. vs. Atty. Pablito M. Castillo, Et AlDocument16 pagesAtty. Leon L. Asa, Et Al. vs. Atty. Pablito M. Castillo, Et AljafernandNo ratings yet

- F.Y.B.Com SyllabusDocument50 pagesF.Y.B.Com Syllabusrakesh_crcNo ratings yet

- FintechFinance1 Online v3Document128 pagesFintechFinance1 Online v3Santosh KadamNo ratings yet

- Master POA Sample Book PDFDocument20 pagesMaster POA Sample Book PDFwjpodjoaspodjadNo ratings yet